Nikko AM Insights

Harvesting Growth, Harnessing Change - Monthly Insights: Asian Equity-March 2023

In a world starved of workers and growth, we believe that Asia’s ability to supply both puts the region on a very firm footing over the longer term. Once we get through this current US-led rate tightening cycle and the flush out of weaker financial institutions in the West, we see a bright future for Asia, which is now trading at extremely attractive valuations.

Navigating Japan Equities: Monthly Insights from Tokyo (April 2023)

This month we discuss how potential market volatility still bears watching even if the global banking turmoil may not directly shake Japan; we also assess how a steady domestic demand recovery may be in sight even if the public is slow to remove their masks after the recent easing of restrictions.

Consumption in Asia from a new perspective

Asia’s consumption trends were once thought to be heavily influenced by those in the West, but that is no longer the case. Asian consumers have diverse tastes and influences and they are starting to dictate global trends instead of merely absorbing them. We believe that Asian brands are well placed to respond to this new paradigm.

Resilience and attractiveness of Asian local bonds

Asian local currency bonds are expected to thrive as the region’s central banks end their rate hike cycle on the back of easing inflation. We believe that strong fundamentals, high-quality yields and limited foreign ownership are other factors that are supportive of this fixed income asset class.

Balancing Act-Monthly insights: Multi-Asset Team-March 2023

Investors have been dealing with elevated volatility in asset prices since the pandemic began. A contributing factor that continues to muddy the waters has been the volatility in economic data due to COVID-led distortions. In more recent months, particularly in the US, unseasonal weather patterns have made reading the economic tea leaves even more difficult.

Global banking turmoil from an Asian perspective

It could be some time before the market stabilises in the wake of the global banking turmoil, and investor appetite toward financial subordinated debt will likely be weak in the near term. That said, considering the current valuations of fundamentally stronger Asian banks, we believe that a large part of such concerns are already reflected in their spreads/price following the re-pricing which took place earlier in March.

Global Investment Committee’s Outlook

We expect fairly rough sailing for the global economy, financial system and markets in the next two quarters, but we do not expect disasters and there should be major relief for stocks later in 2023 as central banks begin to ease policy.

Asian financials: beyond the drama

Asian banks will be more insulated from the current global banking turmoil, in our view, thanks to smaller-scale rate hikes in Asia, prudent supervision by regional financial regulators, outsized capital adequacy ratios and sensible security exposure relative to total assets. We believe this will bode well for the sector in the longer term and enhance its attractiveness.

New Zealand Equity Monthly – February 2023

Bonds have been attracting more attention from investors recently in view of their higher yields and the possibility of capital gains. In addition, as equities have lost their shine for now amid higher interest rates, bonds are expected to continue to benefit from an asset allocation perspective.

New Zealand Fixed Income Monthly – February 2023

Bonds have been attracting more attention from investors recently in view of their higher yields and the possibility of capital gains. In addition, as equities have lost their shine for now amid higher interest rates, bonds are expected to continue to benefit from an asset allocation perspective.

On the Ground in Asia-Monthly Insights: Asian Fixed Income-February 2023

Countries in the region took divergent monetary paths during the month. India and the Philippines raised their respective policy rates, while Indonesia and South Korea maintained their interest rates.

Net zero made in Asia

We believe that there are substantial rewards for those who are capable of driving the push for global decarbonisation. So, the question is: who is building the kit for the world’s net zero ambitions? We believe that the answer, both now and well into the future, is Asia.

Navigating Japan Equities: Monthly Insights from Tokyo (March 2023)

This month we discuss what the market may initially seek the most from the next Bank of Japan governor; we also look at Japan’s expanding outlays, with tax revenue and inflation in focus.

Thoughts on the 2023 China National People’s Congress

The official GDP growth target of “around 5%” unveiled at China’s annual National People’s Congress was lower than many external forecasts, and fiscal policy looks less accommodative relative to both market expectations and that of 2022. In our view, these conservative targets leave room for outperformance and likely reflect cautiousness over unexpected events and reluctance in overstimulating the economy.

The MSCI AC Asia ex Japan Index slumped 6.8% in US dollar terms, giving up its January gains. China’s reopening and peak interest rates euphoria in January were short-lived as hotter-than-expected economic indicator releases in the US raised the spectre of higher-for-longer interest rates.

Today’s surgical robot, tomorrow’s robot surgeon

Considered to be one of the greatest modern-day medical breakthroughs, robotic surgery is revolutionising surgical practices around the world. The breakthrough is particularly prominent in China, which could be the next growth frontier for surgical robotic companies.

The just-released 4Q CY22 data on aggregate corporate profits in Japan was somewhat mixed, as the overall corporate recurring pre-tax profit margin fell from its record high on a four quarter average. The non-financial service sector ticked up, but the manufacturing sector fell from its record high.

Global Equity Quarterly (Q4 2022)

Current equity market conditions dictate that you choose your investment attire particularly carefully. In our view, buying profitless technology companies is like going up a Scottish mountain wearing flip-flops. You might get away with it, but the odds are not in your favour. Instead, we prefer the protection afforded by profits (and cash) generated today—not at some unspecified point in the future.

Thoughts on the BOJ you might not have heard, but should consider

Currently, there is a wide variety of predictions for the BOJ’s actions, with some expecting imminent hawkish decisions based upon some of Governor-nominee Kazuo Ueda’s “anti-distortion” comments, but changes are more likely to be gradual and tentative assuming the global economy continues improving.

On the Ground in Asia-Monthly Insights: Asian Fixed Income-January 2023

We maintain the view that global inflationary pressures may moderate further. We prefer Singapore, South Korea and Indonesia bonds. As for currencies, we favour the renminbi, the Singapore dollar and the Thai baht.

Balancing Act-Monthly insights: Multi-Asset Team-February 2023

Growth prospects look to be improving—a sharp shift from late 2022 when the markets had strong conviction that a first half slowdown was to be followed by a better second half.

Harvesting Growth, Harnessing Change - Monthly Insights: Asian Equity-January 2023

Asian equities made a strong start to 2023, with the MSCI AC Asia ex Japan Index returning 8.2% in US dollar (USD) terms in January, supported by a rebound in investor sentiment towards China.

Japan Value Insights: CDMOs and health-related social needs

Contract development and manufacturing organisations (CDMOs) could play an important role in addressing health-related needs as society seeks rapid solutions to issues such as an increase in refractory diseases.

Navigating Japan Equities: Monthly Insights from Tokyo (February 2023)

This month we assess the trends in wages and salaries with significant change potentially in progress; we also discuss how changes at the BOJ may affect the market.

Nikko AM Japan Value Fund Rated by RSMR

Nikko AM Japan Value Fund Rated by RSMR

Following a rigorous due diligence process, the Nikko AM Japan Value Fund has received an RSMR Rating. The Fund is now one of only 300 RSMR Rated funds, selected from an Investment Association universe of 4,500. You can read the full RSMR Fund Profile HERE. Under RSMR’s binary system, a fund is either rated or it is not and they take a qualitative approach to fund rating. While past performance and risk measures play a role in fund rating, their research team rely on face-to-face meetings with fund managers and management teams across the globe to establish how they will continue to develop performance. RSMR also undertake thoughtful and detailed analysis of social, governmental and market factors to build a picture of the fund over the coming years.

Learn more about the Nikko AM Japan Value Fund HERE.

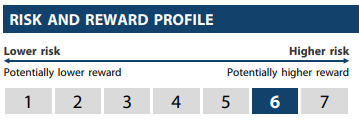

Risk Information

UN SDG Risk: In the event the degree of positive impact towards the UN SDGs of a company and/or its technology changes resulting in the Investment Manager having to sell the security, neither the Sub-Fund, the Investment Manager, Management Company nor the Investment Adviser accepts liability in relation to such change.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Sub-Fund.

Derivative risk - the Sub-Fund may use derivatives as described in the Objectives and Investment Policy. Use of derivatives results in higher chances of loss due to the use of leverage, or borrowing. Derivatives allow investors to earn large returns from small movements in the underlying asset's price. However, investors could lose large amounts if the price of the underlying assets moves against them significantly.

Counterparty risk - the possibility that the counterparty, such as brokers, clearing houses and other agents be unable to perform its obligations due to insolvency, bankruptcy or other causes.

Sustainability Risk - the risk arising from any environmental, social or governance events or conditions that, were they to occur, could cause material negative impact on the value of the investment. Specific sustainability risk can vary for each product and asset class, and include but are not limited to: Transition Risk, Physical Risk, Social Risk and Governance Risk.Important Information

Nikko AM Global Umbrella Fund is an open-ended investment company established in Luxembourg (the "Fund"). This information has been issued by Nikko Asset Management Europe Ltd and is not aimed at or intended to be read by investors in any country in which the Fund is not authorised. The Fund is registered in France, Germany, Italy, Luxembourg, Netherlands, Singapore (restricted registration), Spain, Switzerland and the UK. Some sub-funds and/or share classes may not be available in all jurisdictions. This material is for information only and is not a recommendation to sell or purchase any investment. Any investment in the Fund may only be made on the basis of the current Prospectus and the Key Investor Information Document (KIID), as well as the latest annual or interim reports. Please refer to the "Risk Factors" for all risks applicable in investing in this Fund. These documents are available from our website emea.nikkoam.com or can be obtained free of charge from the Funds registered office in Luxembourg: Private Business Center 32 – 36, boulevard d’Avranches, L-1160 Luxembourg, Luxembourg. Swiss representative, Swiss paying agent and place of jurisdiction in Switzerland: BNP Paribas, Paris, Zurich Branch, Selnaustrasse 16, 8002 Zurich. Telephone: +41 582 126374. Past performance is not a guide to future performance. Market and currency movements may cause the capital value of shares and income from them to fall as well as rise and you may get back less than you invested.