With the whole world watching every move made by the Trump administration on tariffs, in Japan there are other things happening behind the headlines, independent of the outcome of trade negotiations. This year marks the tenth anniversary since the introduction of Japan's Corporate Governance Code, as part of a broader effort to overhaul corporate performance by improving capital efficiency, adding accountability and oversight, and increasing transparency and shareholder engagement. Ten years on, those reform initiatives that were designed to modernise Japan's corporate culture, are clearly bearing fruit.

According to the Nikkei, the number of Japanese companies that have received shareholder proposals from activist investors has reached a record high of 50 so far this year (up from 46 last year) rising for the second straight year. Japan's once-stable shareholder base has come down, as a result of the unwinding of cross-shareholdings over the past decade. With Japanese companies now less insulated from shareholder pressure, and having a more diverse shareholder base, this is creating more opportunities for activist investors to push for change.

Unsolicited offers as “necessary evil”

In the meantime, since METI released its merger and acquisition (M&A) best practice guidelines in August 2023, there has been an increasing number of unsolicited offers made in the Japanese market. What would once have been considered as a “hostile takeover” has now been renamed as the more palatable “acquisition without consent”.

In the past, investment banks and corporate lawyers had largely avoided advising potential suitors on hostile takeovers due to fear of being criticised for siding with what were considered aggressive actors. This was especially the case when a large banking group could run the risk of losing its loans business as the price for conducting M&A business. Today, these banks are now free from reputation risk. This means companies can use their expertise in unlocking and creating value through M&As, irrespective of the nature of the deals.

The last sentence in an op-ed in the Nikkei newspaper published in Japan on May 10 was very powerful and carries significant weight: “we should not go back to the days when 'hostile takeovers' were a taboo”. This is a remarkable statement coming from the most established and respected financial news source in Japan and would have been unthinkable in the pre-Global Financial Crisis or even pre-pandemic days and demonstrates how the corporate climate in Japan has changed.

What is the success rate?

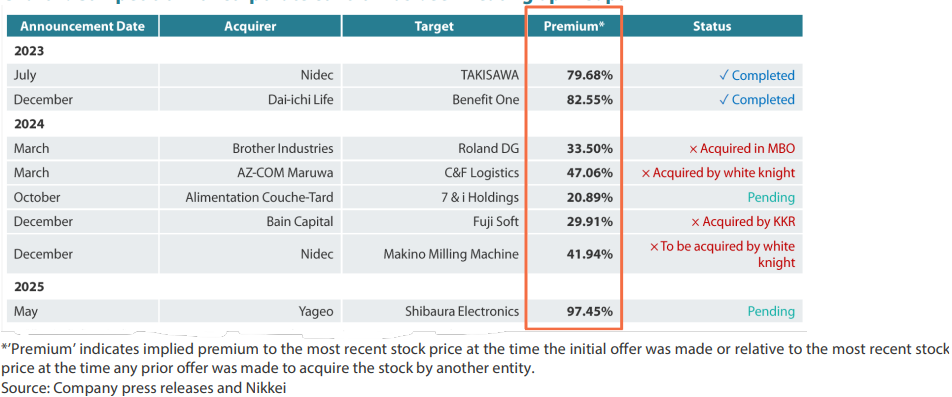

Given the increasing trend in shareholder activity, the next question to ask is how successful are these acquisition attempts? Clearly, not all offers have been successful. In fact, many of them can be considered as “not successful” given the targeted companies were not eventually acquired by the hostile suitor. However, they were all “successful” in putting companies' management teams on the spot, and in attempting to fend off suitors by focusing on enhancing shareholder value. For example, following the unsolicited takeover offer from Canadian retail giant Alimentation Couche-Tard, Seven & i Holdings is now taking steps to improve its corporate strategy and operations to lift its share price above the suitor's bid price.

White knights to the rescue?

Even unsuccessful attempts can result in greater shareholder value being realised. In late 2024, Nidec's unsolicited offer which targeted Makino Milling Machine, Japan's second-largest machine tool maker, was said to be not only “without consent” but also without any prior behind the scenes negotiations. It was rare in a sense that the move was not triggered by prior negotiations breaking down, as is often the case.

Nidec eventually gave up on the pursuit of Makino, after the targeted company threatened to mount a "poison pill" takeover defence. It was effectively forced to find a “white knight” – MBK Partners—that is now expected to acquire and take control of the company at a higher price. MBK Partners ended up offering a higher price (6.8% higher than Nidec's original tender offer, which placed a hefty 41.94% premium on the stock) to buy out Makino. In this case, even greater value is expected to be unlocked for Makino's existing shareholders when the tender offer goes through.

Bidding wars are good for shareholders

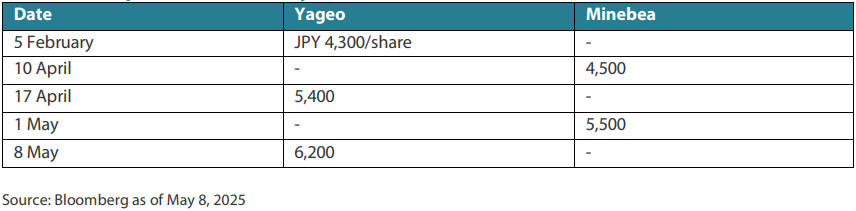

Other cases have triggered bidding wars between hostile suitors and white knights. A recent case involved the Taiwanese electronic component maker and a well-known Apple supplier Yageo offering to buy Shibaura Electronics, known for its competitive sensors, measuring devices and control equipment. Yageo believed it could help the domestic-focused Shibaura to expand its sales distribution channels globally.

Shibaura's stock price as of the close of 4 February was JPY 3,140. The initial bid price put out by Yageo was JPY 4,300 per share, which implied a premium of 36.94%. After Shibaura was reported to have sought a white knight, the Japanese electronic component maker Minebea Mitsumi announced plans to offer a higher price (JPY 4,500 per share) in a friendly deal. The two companies are aligned and have indicated that they are better positioned to realise synergies from the merger. The bidding war has continued to play out over the past few months, as shown in the table below.

Chart 1: Offer prices announced by the bidders

At the time of writing (12 June,) the highest bid price is JPY 6,200 per share, implying a 97.45% premium over the stock price on 4 February. Who could have expected the stock doubling in price in just three months without a competitive environment for corporate control?

Chart 2: Competition for corporate control has been heating up in Japan

Summary

Businesses should be owned and operated by whichever companies can maximise their value and is prepared to pay the highest bid price. Corporate governance reform over the last decade has laid the foundation for this to happen. We have discussed in the past how corporate culture is something that cannot be changed overnight. Today, it has become inarguable that in the ten years since the Corporate Governance code was introduced, and just two years since METI's M&A guidelines delivered a framework for unsolicited offers, Japan's corporate culture has undergone a dramatic shift.

While we expect the number of M&A cases to increase going forward, what is equally important is that companies are taking proactive measures to avoid being targeted by strategic buyers. This should help to unlock further value in the Japanese market in the years to come.

To learn more about unlocking hidden value in Japan, download the Nikko AM investment guide here.

About the author

Junichi Takayama, Japan Equity Investment Director

Junichi Takayama acts as a direct conduit for the Tokyo-based Japan Equity team's investment process, research, and insights to global clients. Junichi joined Nikko Asset Management in Tokyo as Investment Director in December 2013. He was assigned to continue these efforts from the firm's London office in April 2023.

With over two decades of investment management industry experience in Japan and the United States, he has a distinct East to West and West to East view of capital markets. Junichi started his career at Daiwa Securities SMBC (now Daiwa Securities Group) in Tokyo. After spending three years as an investment banking analyst involved in equity capital raising, he moved to California to join Taiyo Pacific Partners, which manages a Japan-focused activist fund in partnership with CalPERS and WL Ross & Co. After four years there conducting bottom-up fundamental equity research and engaging with Japanese corporate managers, he moved back to Tokyo to join the US asset manager Principal Global Investors as a Japan Equity Analyst and later a Japan Equity Portfolio Manager.

Junichi earned his Bachelor of Arts in Economics from the University of Michigan, Ann Arbor and Master of Business Administration with Honors from the University of Chicago Booth School of Business. He is a Chartered Financial Analyst (CFA), Chartered Alternative Investment Analyst (CAIA) and Certified Member Analyst of the Securities Analysts Association of Japan (CMA).