Japanese equities: the story so far

Japanese equities reached another significant milestone in March 2024, when the combined market capitalisation of Tokyo-listed stocks hit quadrillion territory—1,000 trillion yen—for the first time. Throughout Japan’s extended period of stock market growth, large caps have outperformed small caps, as the market's flow-driven nature has seen larger companies attract the lion’s share of capital inflows. Yet despite the overall market surge, a substantial number of Japanese value stocks remain underpriced, particularly within the small and mid-cap sections of the market and are still trading below their book value. This presents, in our view, some exciting investment opportunities, particularly for active managers.

Chart 1: Many value stocks still trading at a discount (December 2022 vs May 2024)

Source: Russel / Nomura Japan Indexes, Nomura Fiduciary Research & Consulting (December-end 2022 versus May-end 2024)

Compared to other equity markets, active fund managers fare better in Japan

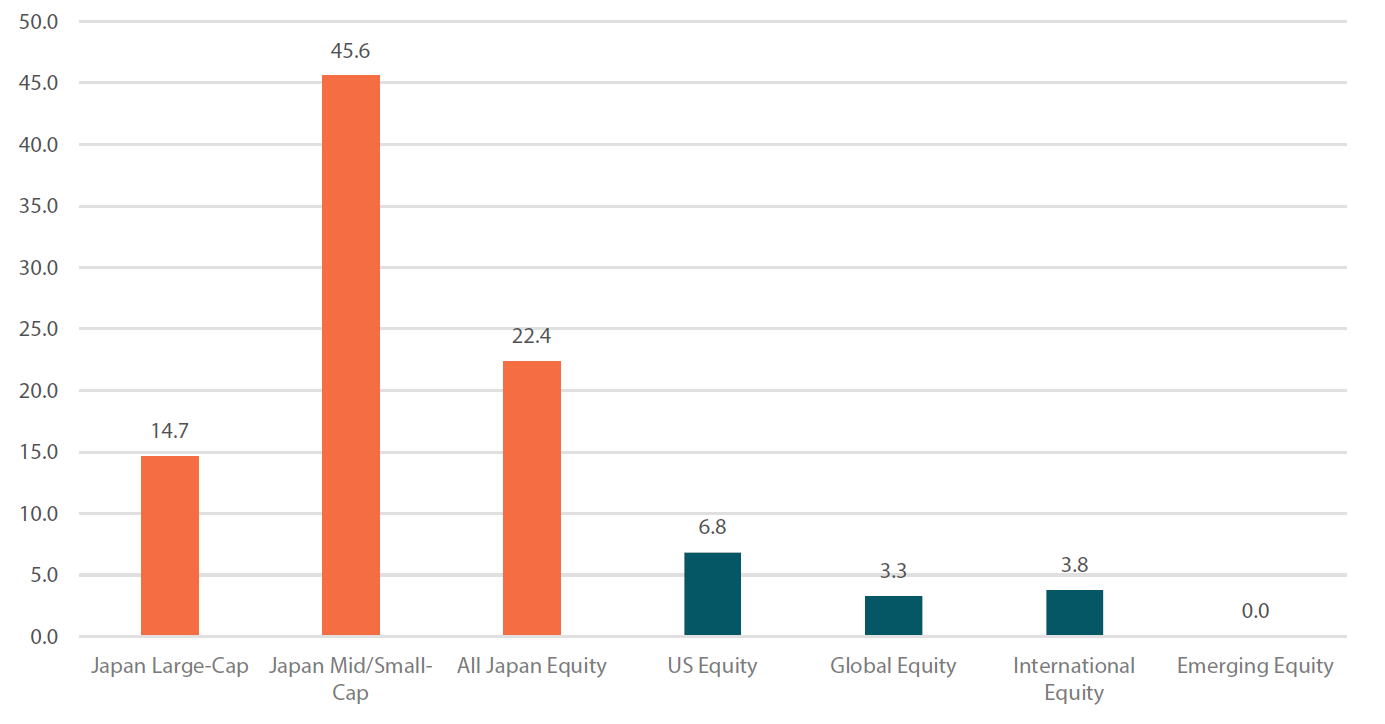

When it comes to generating alpha, Japanese equities are an ideal hunting ground for active fund managers seeking alpha. This is true for the All Japan Equity category, and particularly evident in the small and mid-cap segments. The percentage of active funds outperforming their benchmarks over a 10 year period is meaningfully higher than other asset classes.

Chart 2: Percentage of funds outperforming their benchmark over 10 years

Source: Nikko AM based on S&P Dow Jones Indices SPIVA Japan Scorecard Year-End 2023

Past Performance is not a reliable indicator of future results.

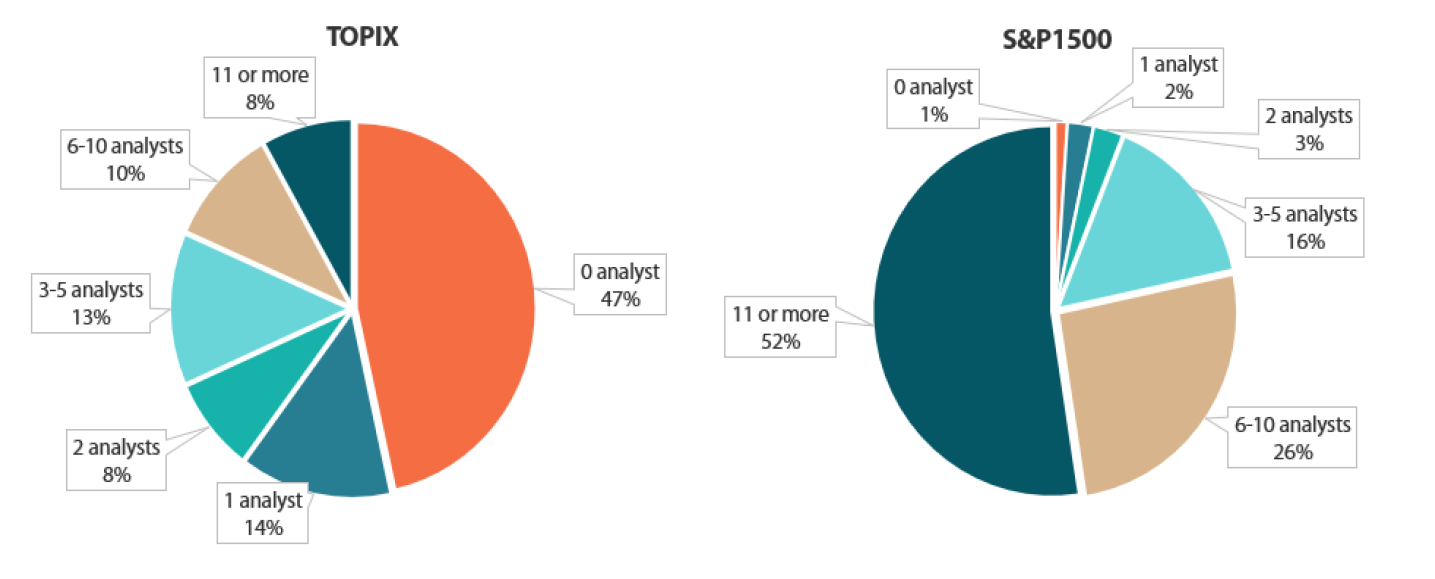

The outperformance of active managers is, in part, due to the fewer sell-side analyst coverage, limited investor access to company management (although it has improved significantly over the years) and a slower dissemination of information which gives experienced active managers the opportunity to apply their research capabilities, local knowledge and analytical skills. For example, 47% of the TOPIX Index receives zero coverage by sell-side analysts versus 1% for the S&P 1500. As a result, active managers can gain insights not reflected in market prices, helping them to identify mispriced securities before the broader market catches up.

Chart 3: Analyst Coverage by Market – Japan versus US

Source: Bloomberg as of end-December 2023

Understanding Japanese culture

Active management within Japan also benefits from a deep understanding of Japan’s unique cultural and business environment. Japan’s corporate culture is characterised by long-term relationships, consensus building and attention to detail. These cultural qualities significantly influence corporate behaviour and decision-making processes, which in turn, impacts the performance and valuation of Japanese companies.

Therefore, understanding Japan’s cultural nuances by having “feet on the ground”, including direct engagement with companies at all levels, can often prove invaluable in identifying investment opportunities. Building relationships with local industry experts, suppliers, customers and other stakeholders across supply chains can offer valuable perspectives on market trends and company performance. This is particularly critical within the overlooked small and medium-sized segments, where developing specific company insights can give active fund managers a significant competitive advantage.

Are value stocks now in the ascendency?

Value stocks, by definition, trading at lower price-to-earnings ratios and/or offering higher dividend yields, have benefitted from the market's emphasis and preference for more conservative and income-focused investment strategies. This trend is reinforced by Japan’s ongoing economic recovery, which has boosted the earnings prospects of traditionally undervalued sectors such as industrials, financials, and consumer goods.

Therefore, the persistence of value stocks trading at a discount to book value is particularly notable, suggesting investors have yet to fully recognise the intrinsic worth of these companies. While true for some large-cap value stocks, this is especially true for small and mid-cap value stocks, which tend to be overlooked compared to their larger-cap counterparts. As the Japanese equity market rally broadens and extends beyond the major indices, there is considerable potential for these smaller and mid-sized firms to experience meaningful upward price corrections.

Higher dividends signal confidence in earnings and improvement in corporate governance

The current climate of higher dividend growth from Japanese equities signals a strong vote of confidence from companies about their earnings prospects and a commitment to improving corporate governance. Investors are welcoming this trend, and high dividend-paying stocks offer a high and consistent income stream, low interest rate sensitivity, and a strong element of downside protection. With dividend growth likely to continue, driven by earnings and higher payout ratios, Japanese dividend-paying stocks look attractive for long-term, income-focused investors.

Summary: Japan’s equity market growth likely to broaden

Japan’s economic success has been underpinned by several longer-term factors, including solid macroeconomic fundamentals, favourable government policies and strategic corporate reforms. However, despite the runaway success of Japanese equities, an active management approach suggests there are some bargains still to be found. Japan’s small and mid-cap companies, particularly those overlooked and undervalued by the market, appear to have much more room to move higher as the rally broadens out.

Nikko AM team in Europe

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.