In March 2024, after the Nikkei Index reached an all-time high, Japan Equity Investment Director Junichi Takayama offered five structural reasons why Japan’s economic resurgence was more than just a flash in the pan (read the full article here). Almost a year later, those five reasons remain just as relevant for investors considering an allocation to Japan, as Junichi explains.

One: wage hikes in 2025 set to unleash domestic consumption

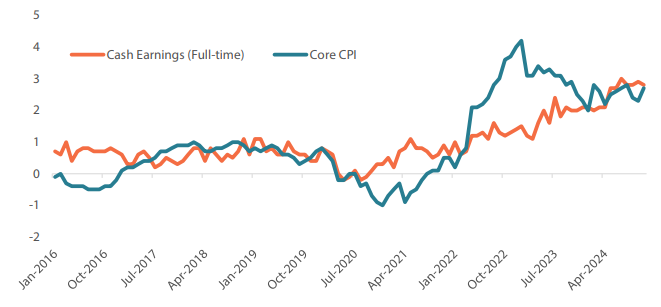

In last year's update, we highlighted the expected recovery in Japanese consumption, noting that the “Shunto” spring wage negotiations were likely to lead to higher consumer spending. While consumption remained modest throughout 2024, we are seeing an increasing number of positive signs. With inflation easing and wage growth accelerating, real wages have finally turned positive, a shift that could pave the way for our anticipated rebound in consumer spending. Chart 1 below plots cash earnings verses core consumer price index (CPI) inflation, and highlights how wage growth, in tandem with lower inflation, is leading to widespread real income growth.

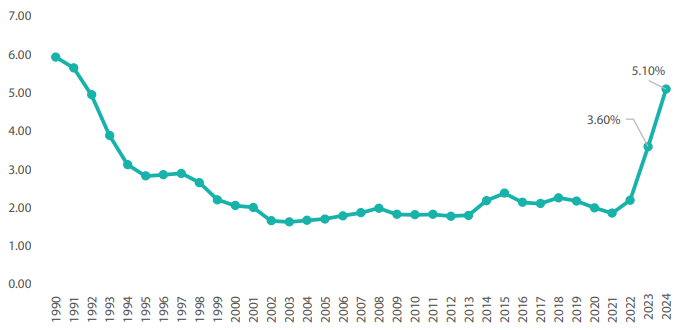

This year's round of Shunto Spring wage negotiations, where labour unions negotiate salary increases with employers ahead of the new fiscal year, are signalling record pay increases. As chart 2 below shows, two years ago, the outcome of these talks saw wages rise by 3.6%, followed by a 5.1% increase last year. This year, unions representing major industries have already called for substantial hikes: electronics sector unions have demanded a 5% rise in base salaries, airline workers are pushing for 4%, and telecom giant NTT's union is seeking a 3% increase. These figures do not include Japan's traditional seniority-based pay increases, which typically add around 2% annually.

As a reminder, Japan's employment system has long been known for its stability, with many employees spending their entire careers at a single company and following a structured pay scale. This has historically led to predictable, gradual wage growth. However, the recent momentum behind pay negotiations marks a significant shift. Labour unions are pushing hard for more aggressive base salary increases, reflecting both rising living costs and labour market dynamics (i.e., increase in job hopping), even before taking into account seniority wage growth. Encouragingly, corporate managers have signalled a willingness to meet these demands, with some indicating that another year of strong wage growth is likely.

Chart 1: Wage growth gaining momentum outpacing inflation (Cash Earnings* vs. Core CPI)

Source: Bloomberg as of January 9, 2025

* Cash Earnings is based on monthly labour survey (same sample basis) conducted by the Ministry of Health, Labour and Welfare

Chart 2: Percentage wage increase in spring wage offensive

Source: Ministry of Health, Labour and Welfare of Japan and Rengo (for 2024) as at 3 July 2024

We would therefore argue that Japan's domestic consumption story remains in the early innings. With workers finally seeing their real incomes improve, consumer confidence is expected to strengthen, potentially unlocking pent-up demand that has been building over recent years.

Two: after a record-breaking 2024, Japan's inbound tourism has impetus

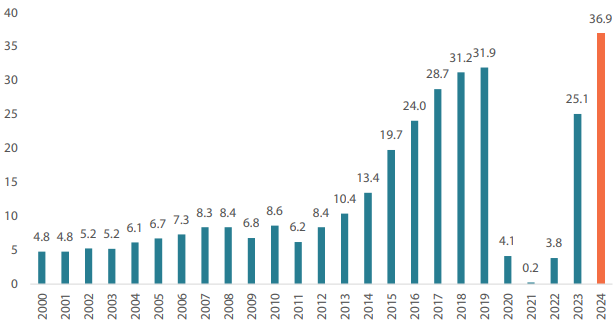

As expected, thanks to the removal of COVID-19 border control restrictions in 2023, last year saw a return to pre-pandemic levels for Japan's tourism industry. Official figures show Japan welcomed 36.9 million tourists in 2024, far exceeding the previous peak in 2019. And the momentum is expected to continue. JTB, Japan's leading travel agency, recently forecast an 8.9% increase in inbound visitors this year, with total arrivals expected to reach 40 million for the first time.

Chart 3: Number of inbound tourists (millions)

Source: Japan National Tourism Organization (JNTO) as at 15 January 2025

However, the recovery in overseas visitors to Japan has been uneven across different markets. Tourists from South Korea, Taiwan, Hong Kong and the US have returned in greater numbers than before the pandemic, but Chinese visitors—the largest group of pre-COVID spenders—have yet to fully come back. That said, signs point to a growing rebound, with Chinese travel interest in Japan picking up, particularly around major holidays such as Chinese New Year. Online travel platforms such as Trip.com have ranked Japan as one of the most popular destinations for Chinese tourists, suggesting a surge in visits in the months ahead.

One potential catalyst for further growth is Japan's expected relaxation of visa requirements for high-net-worth Chinese travellers and those in group tours. While the details are still being finalised, this policy shift would allow Chinese visitors greater flexibility to enter and stay longer in Japan, potentially boosting both arrival numbers and tourist spending. The move appears to be a reciprocal gesture following China's decision in November last year to ease visa restrictions for Japanese citizens, as part of broader efforts to strengthen diplomatic and economic ties between the two countries.

Beyond policy changes, Japan has several major events on the horizon that could further support inbound tourism, including the World Expo in Osaka, which begins in April and ends in October of this year. With international visitor numbers on track to hit new highs and China's return gathering pace, 2025 could prove another record-breaking year for Japan's tourism sector.

Three: TSE bares its teeth in improving corporate governance

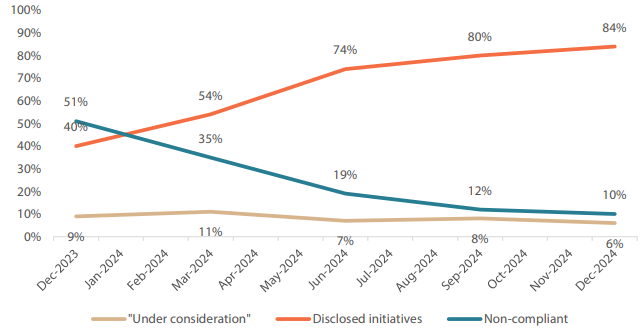

Japan's corporate governance landscape has seen a major shift over the past year, with the Tokyo Stock Exchange (TSE) applying its “carrot and stick” approach to underperforming companies to much greater effect. What started as gentle encouragement has evolved into a more forceful strategy, one that relies on naming and shaming to push companies into action.

Since January 2024, the TSE has publicly listed companies that have responded to its call for improved governance and capital efficiency. The impact has been significant: at the start of the initiative, just 40% of companies had responded, but by the end of the year, that number had jumped to 84%.

Chart 4: Compliance status to TSE's request

Source: Tokyo Stock Exchange as at 31 December 2024

Crucially, it's not just about responding to requests, companies are now taking meaningful corporate actions. Many firms have outlined clearer financial strategies and disclosed concrete steps to improve capital efficiency. The focus for 2025 will be delivering on these commitments and translating plans into measurable outcomes.

One particularly effective tactic introduced by the TSE is the publication of best practices, which was initially disclosed in February 2024. Companies that have provided strong explanations of their cost of capital and capital efficiency measures are showcased as role models. Data shows that these companies, which have been highlighted in TSE's best practice cases, have significantly outperformed their peers in terms of stock price performance.

Conversely, the TSE has also started publishing examples of poor governance practices in November 2024. While these cases remain anonymous (using placeholder names like “Company ABC” or “Company XYZ”), it's clear to those involved when they have been identified as a laggard. This public scrutiny acts as a powerful motivator, particularly in Japan, where corporate culture places a high value on reputation and peer perception.

Ultimately, the TSE's tougher approach is proving effective. Visibility and peer pressure are proving to be strong incentives for companies to improve governance standards, making Japan's corporate landscape more investor friendly. With nearly all targeted companies now engaged in the process, the next challenge will be ensuring that these commitments lead to tangible, lasting change.

Four: Japan's companies under pressure to conduct shareholder engagement

The word “hostile” often carries a negative connotation, but in the context of Japan's evolving corporate environment, it has become a sign of progress. The Ministry of Economy, Trade, and Industry (METI) has made it clear that companies can no longer ignore takeover bids, whether friendly or not. Under new guidelines, listed firms have a responsibility to consider all acquisition offers, creating an environment where collective shareholders' interests are harder to overlook. A wave of unsolicited takeover bids is forcing companies to become more responsive to investors, marking a significant step toward a more competitive corporate landscape.

This was highly evident in 2024. Over the 12 months, at least five major unsolicited takeover offers surfaced, involving both private equity firms and corporate bidders. While not all of these bids succeeded, some forced higher valuations, benefiting shareholders. In some cases, counter offers from rival buyers or management buyouts resulted in companies being acquired at significantly higher prices than the initial bids, with premiums of 30-50% have not been uncommon.

One of the most widely followed cases is Seven & i Holdings, where management is now said to be considering what could become Japan's largest-ever management buyout. Reports indicate it is seeking financial backing from a Thai conglomerate, Japanese megabanks, and US private equity firms like KKR. The fact that such a large corporation (approximately USD 40 billion in market cap) is actively engaging in takeover defence illustrates just how much outside pressure has increased.

This case and others underscore a new reality for Japanese companies: they can no longer assume they are safe from outside bids. The risk of waking up to an unexpected acquisition attempt is forcing management teams to stay disciplined, engage with shareholders and focus on value creation. With regulatory backing and a clear increase in takeover activity, Japan's corporate culture is shifting toward greater shareholder accountability. If current trends continue, 2025 could see even more companies put under pressure to justify their valuations, or risk becoming acquisition targets themselves.

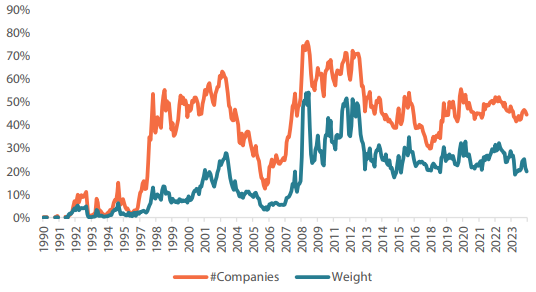

Five: Japanese value stocks still trading at a significant discount to book value

Despite Japan's improving corporate governance and rising stock prices, many value stocks continue to trade below book value, presenting a significant opportunity for investors. As of 2025, nearly half of listed companies are still valued at less than their net assets, a striking contrast to markets like the US, where such deep discounts are rare.

Chart 5: Percentage TOPIX companies trading below book value

Source: Toyo Keizai as of end-December 2024

Moreover, while 2024 was largely about improving investor disclosure, with companies laying out clearer financial strategies and setting ambitious targets, this year the focus is shifting toward tangible corporate actions aimed at unlocking value. Some of the key trends driving this shift include the following:

- Increased share buybacks: In 2024, buybacks surged by 70% year-on-year, as companies sought to return capital to shareholders and support stock prices. This momentum is expected to remain strong in 2025, signalling greater financial discipline.

- Higher dividend payouts: More companies are committing to raising dividends, making shareholder returns an even higher priority than in previous years.

- Mergers, acquisitions, and spin-offs: With pressure mounting on undervalued firms, many are turning to M&A activity and restructuring as a means of driving efficiency and improving market valuations.

Japanese companies are also using their cash reserves more strategically, not just for returning capital to shareholders but also for growth investments and acquisitions. This dual approach, enhancing shareholder returns while also actively pursuing value creation, is key to closing the valuation gap.

Final thought: Bank of Japan optimism about the economic outlook

There is also another key indicator for the direction of the Japanese economy for investors to consider, which is the optimism on display by the Bank of Japan (BOJ)'s recent interest rate hike. The decision from the BOJ in January to raise its short-term policy rate to around 0.5% has increased the cost of borrowing to its highest level in 17 years, a move that signals confidence in the country's economic outlook. While some may see rate hikes as a form of monetary tightening, the reality is more nuanced.

We would argue the BOJ's move away from ultra-loose monetary policy is a sign of economic normalisation, rather than a major tightening cycle. The BOJ's policy stance remains accommodative, and this adjustment reflects its belief that the economy, particularly wage growth, is on a solid path.

For investors who resisted increasing their allocation to Japanese equities in 2024, perhaps the confirmation of these five key trends might give them reasons to reconsider in 2025. The progress made over the last 12 months suggests Japan is still in the early stages of a longer-term economic growth cycle, with the best yet to come. Therefore, applying an active management approach, one that understands these trends, can discern winners from losers and also unlock value in a market still being overlooked by global investors, presents a compelling investment opportunity.

To learn more about unlocking hidden value in Japan, download the Nikko AM investment guide here

If you have any questions on this report, please contact:

Nikko AM team in Europe

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.