It's perhaps an understatement to say things have been eventful since the return of Donald Trump to the White House. Along with the implementation of “Trump Tariffs” that has threatened to upend the global order, the new administration has spearheaded a resetting of sustainability initiatives which has been playing out both at the government and corporate level. Earlier this year, under pressure from shareholders, BlackRock became one of the latest large fund management house to remove itself from the voluntary Net Zero Asset Managers (NZAM) initiative. This followed six of the largest US banks (including Goldman Sachs, Morgan Stanley and JPMorgan) quitting the Net Zero Banking Alliance.

With sustainability seemingly out of favour in the US for at least the next four years, it would be tempting to see the tide turning against sustainable bonds and other forms of sustainable investment. Despite the shift of direction from the US, we believe the fundamentals underpinning sustainable bonds, particularly green bonds, will remain strong due to the global momentum in favour of this asset class.

A once-in-a-generation opportunity?

First, there's the investment case for fixed income itself. From a purely financial perspective, bond yields are at levels not seen in nearly 20 years. This matters because a bond's yield largely determines its expected return over a three-to-five-year horizon, offering investors a level of predictability that is often hard to find in equity markets. Compared to where bonds have been historically, this makes them an attractive option in today's uncertain environment.

Moreover, the global sustainable bond market shows no signs of slowing down, with total issuance now surpassing US dollar (USD) 5 trillion. This figure includes a broad range of issuers, from governments and supranational organisations to mortgage-backed securities and municipal bonds. Such depth means that investors can now construct well-diversified portfolios that closely track global bond indices, reducing concerns about limited investment options or liquidity constraints.

The US dollar has strengthened in recent years due to interest rate differentials and the Federal Reserve's aggressive tightening, but shifting macroeconomic conditions suggest an impending reversal. With inflation easing and potential rate cuts on the horizon, historically high US asset valuations could prompt capital outflows, weakening the dollar. Growing fiscal deficits, increased Treasury issuance, and political uncertainty further threaten dollar stability, mirroring its decline in 2017 during Trump's first term. Sustainability-focused indices, which are predominantly Eurocentric in composition, could outperform traditional indices if prolonged dollar weakness persists, benefiting from their structural preference for euro over dollar assets.

And of course, as the sustainable bond market has grown and matured, concerns over the “greenium”, the premium investors should expect to pay for choosing sustainable bonds over other fixed income assets, has died down. Any yield differences observed have been marginal—we're talking a handful of basis points—with other factors such as currency risk and duration exposure having a far greater impact on performance. In fact, green bonds are now behaving much like their conventional counterparts in terms of returns. The iBoxx Green, Social, and Sustainability Bond Index is performing in line with broader benchmarks such as the Bloomberg Global Aggregate Bond Index. This is a crucial shift, demonstrating that investors no longer have to choose between sustainability and competitive financial returns—you can have a positive impact while earning financial returns.

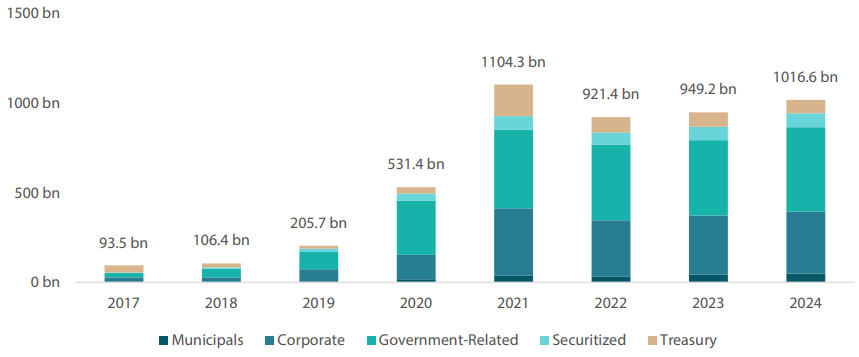

Chart 1: Over USD 1 trillion in sustainable bond issuance in 2024 (by issuer type)

Source: Nikko AM, Bloomberg (as of December-end 2024)

As the US retreats on sustainability, other countries step up

Despite the rhetoric surrounding the new US administration and its decision to, once again, withdraw from the Paris Climate Agreement while rolling back Biden-era green initiatives, we view this shift as unlikely to have a significant impact on the global sustainable bond market. After all, historically, US domestic issuers have played a minimal role in issuance. For example, corporate issuance of labelled green bonds or ICMA-aligned instruments has been virtually non-existent relative to the broader market. The main sources of green bond issuance linked to the US come from Fannie Mae's green mortgage-backed securities and LEED-certified commercial mortgage-backed securities. Beyond that, multilateral institutions like the World Bank and the Inter-American Development Bank, both of which are headquartered in Washington but backed by multiple countries, remain the dominant issuers. Since these institutions are not under direct US government control, they are unlikely to be affected by US domestic policy changes.

More broadly, concerns that a change in US leadership would disrupt the sustainable bond market appear unfounded, as the vast majority of issuance takes place outside the US. Green bond issuance in 2025 has already reached USD 128 billion as of mid-February, putting it on track to exceed USD 1.1 trillion by the end of the year, which would see it matching or even surpassing last year's levels. While greater US participation could further expand this market, its absence is not hindering overall growth.

European countries evolving their views on regulation

Interestingly, the political shifts in the US look to be having an unexpected effect by sparking debate within the European Union (EU) about the complexity and cost of compliance with sustainability regulations. Concerns have been raised by countries like France, Germany and Denmark that extensive environmental, social, and governance (ESG) reporting requirements are making the EU less competitive. This push for simplification is largely stemming from The Draghi report on EU competitiveness published in September 2024, which called for the simplification of regulations to keep the EU competitive. This report led to the idea of Omnibus regulation, aimed at reducing and merging regulatory requirements. Countries such as France and Germany have publicly voiced their support for this initiative, citing concerns about the burden on businesses. If the EU can strike a balance between preventing greenwashing and maintaining a workable framework for companies, it could help sustain market growth rather than stifling it with too-rigid compliance demands.

Meanwhile, while some asset managers have been stepping back from formal net-zero initiatives, commitments and collaborative engagements on climate change due to legal and compliance concerns, primarily in the litigious US market, this has not led to a similar retreat from green investments. In fact, fund-specific adoption of green bonds continues to rise, with Bank of America reporting that over USD 40 billion has been absorbed into green bond funds, double the pace of the previous year. Investors continue to see value in sustainable fixed-income products, and demand from fund managers for green bonds is only growing.

Japan's increasing participation in the green bond market

Finally, there's a strong argument to suggest Japan's increasing participation in the green bond market could be a game changer. The Japanese government started issuing transition bonds in February 2024, for its Green Transformation (GX) programme, which aims to mobilise Japanese yen (JPY) 150 trillion (USD 1 trillion) for advancing sustainable technologies over the coming decade.

Historically, Japanese pension funds were slower to adopt ESG investment strategies, but that has been shifting in a positive direction. In the past year, seven major Japanese pension funds signed onto the UN-backed Principles for Responsible Investment (PRI), signalling a stronger commitment to sustainable investing. Since June 2024, three funds overseeing retirement savings for police officers and public school employees have joined the initiative, further reinforcing Japan's commitment to sustainable finance. This change has been driven in part by unwavering government support. Former Prime Minister Fumio Kishida actively encouraged Japan's public pension funds to align with ESG principles, and his successor, Shigeru Ishiba, has continued in a similar vein.

The sheer size of Japan's pension market, currently valued at over JPY 90 trillion (USD 566 billion) makes this shift particularly significant. With Japan's pension funds now more engaged and potentially mandated to allocate capital toward sustainable investments, this shift could accelerate adoption and add significant depth to the market. Japan's growing involvement comes at a time when other major economies, including China, are also expanding their green bond programmes.

Summary

For investors currently considering asset allocation decisions, we suggest there is a short window of opportunity before global yields begin to fall and given the inverse relationship between bond prices and yields, a higher fixed income allocation will work in their favour over the coming years. At the same time, the positive outlook for fixed income presents an opportunity to increase green bond exposure. We would argue that the transparency and diversification of green bonds should make them an essential and mainstream part of institutional investors' global fixed income portfolio, especially as investors can now build sustainable portfolios that match the long-term returns of conventional bond markets.

While greater involvement from US issuers would be welcome, the sustainable bond market has proven resilient and growth has been driven by demand from investors globally. The trajectory of the market therefore remains unchanged, with or without US participation. We do not foresee any significant shifts derailing this long-term trend toward a more sustainable future.

If you have any questions on this report, please contact:

Nikko AM team in Europe

Email:

This email address is being protected from spambots. You need JavaScript enabled to view it.