Sharia-compliant bonds, or to give them their official name, “sukuk”, are often dismissed as faith-based instruments with limited appeal outside of Muslim-majority markets. However, this misses the opportunity they present for global fixed income investors seeking diversification, resilience, and sustainability.

During a recent visit to Dubai, I had the privilege of speaking at a conference on the expanding opportunities in the sukuk market and its natural alignment with sustainable fixed income investing. To appreciate sukuk's appeal, we must first understand its foundation in Islamic legal and ethical principles.

How does sukuk comply with Islamic law?

In Islamic finance transactions that involve paying interest, known as “riba” are avoided, as they are inconsistent with ethical and equitable practices. However, sukuk structures address this by placing the borrower's asset into an independent trust. This trust then pays investors a pre-determined income rather than a fixed coupon. From the investor's perspective, the result is much the same as standard fixed income investments: periodic distributions and principal repayment, often with comparable risk and return profiles to traditional investment grade credit.

Issuance remains solid

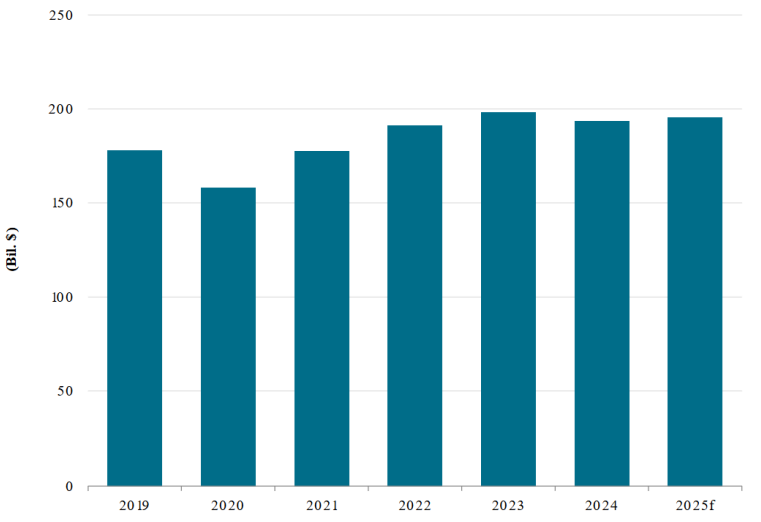

According to S&P Global, global sukuk issuance held steady in 2024, ending the year at USD 193.4 billion, slightly down from USD 197.8 billion in 2023 1 . This stability was driven by a sharp rise in foreign currency issuance, which offset a decline in local currency sukuk. Demand was supported by strong financing needs in key Islamic finance markets, efforts to attract foreign investment, and improving global liquidity as major central banks began to ease monetary policy. All things considered, S&P expects issuance to get close to USD 200 billion again this year.

What is most overlooked, however, is the enviable performance of sukuk compared to conventional fixed income in recent years. Since January 2019 to May 2025, the Bloomberg Global Aggregate Bond Index has returned 0.29% annually, weighed down by rising interest rates and stubborn inflation. In contrast, the Bloomberg Emerging Markets GCC USD Sukuk Total Return Index has delivered a positive annualised return of 4.47% over the same period 2 . This performance gap demonstrates sukuk's relative resilience, driven by factors such as lower duration risk, strong sovereign support from Gulf Cooperation Council (GCC) states, and less exposure to heightened developed market rate volatility.

Chart 1: (USD Dollar) Global sukuk issuance stabilised in 2024 (2025 forecast)

Source: Eikon, S&P Global Ratings 2024

Sukuk's green credentials

Additionally, a growing share of sukuk issuance qualifies as green bonds, a testament to the natural alignment between Islamic finance and ESG principles. In 1Q 2025, ESG sukuk issuance represented over half of all ESG dollar debt in emerging markets (excluding China; US dollars only), according to Fitch Ratings. Sharia law's emphasis on responsible investing, social welfare, and avoidance of harm mirrors the objectives of sustainable finance. For investors seeking values-based alignment without sacrificing yield or credit quality, sukuk therefore present a well-suited alternative.

The United Nations Development Programme's report on green sukuk 3 published in May 2025 highlights this convergence between Islamic finance and sustainable investing, noting that its principles of social justice, risk-sharing, and environmental stewardship offer an ethical way to mobilise long-term capital for climate-focused investments and the green transition. Green and sustainability sukuk issuers had already raised over USD 11 billion during the first three quarters of 2024, with projections suggesting USD 30–50 billion could be mobilised by 2025 to help close the Sustainable Development Goals funding gap.

To accelerate growth in the green sukuk market, the UN recommends that governments issue benchmark sovereign green sukuk and establish unified taxonomies that define what qualifies as “green” under Shariah principles. Aligning these frameworks with global standards—such as the EU Green Bond Standard and ICMA's Green Bond Principles—would reduce ambiguity, enhance credibility and attract sustainability-focused investors, including SFDR Article 9 funds.

Regulatory crossroads for the sukuk market

Despite its advantages, liquidity remains a challenge. A key obstacle is the lack of interbank dealer support and active market-making in the sukuk space, particularly outside core Islamic finance jurisdictions. This underdeveloped secondary market infrastructure limits institutional participation and keeps bid-ask spreads wider than they should be. With more robust dealer engagement, liquidity would improve significantly, allowing sukuk to integrate more fully into global bond portfolios.

There is a potential cloud on the horizon, however, in the form of a proposed shift to asset backed sukuk, requiring full legal ownership to be transferred to investors. This proposal, known as Shariah Standard 62, is being considered by the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI). Core markets for sukuk issuance, including Saudi Arabia, the United Arab Emirates and Indonesia, have different legal rules and limits on asset transfer. Changing the nature of sukuk would create a number of legal and political challenges. From an investor perspective, changing the ownership structure of sukuk could make them more expensive and less appealing as fixed income equivalents, while Fitch Ratings has warned that new sukuk structures may not be able to meet existing standard credit rating models. This would effectively shut out institutional investors, such as pension funds and sovereign wealth funds, that are required to hold credit-rated assets and have only recently entered the sukuk market.

AAOIFI has said it is currently taking industry feedback on board, with the final standard due this year. There is still hope that new rules remain both true to Shariah principles and are practical enough for sovereign and corporate sukuk issuers to implement without stifling market appetite.

Summary

Rather than being dismissed as religious outliers, sukuk deserve to be thought of as sound financial instruments with increasing global relevance. At a time when fixed income investors have grown used to their returns being hampered by developed world uncertainty, sukuk deserve serious consideration from those seeking durable yield, true portfolio diversification and sustainability alignment.

If you have any questions on this report, please contact:

Nikko AM team in Europe

Email:

This email address is being protected from spambots. You need JavaScript enabled to view it.