Japan’s corporate reforms are now reaching small and mid-cap firms

Japan’s steady programme of market reform initiatives, including the realignment of the Tokyo Stock Exchange (TSE) and more recently, its guidance to call for companies to focus on cost of capital and share price, has driven improvements in corporate governance and unlocked previously overlooked value opportunities. While Japan’s corporate reforms targeted larger, global businesses first, we are starting to see smaller firms adopting reforms that will further unlock shareholder value. We believe Japan’s programme of ongoing reforms will further benefit “cash-rich” firms, many of which are small and mid-cap companies.

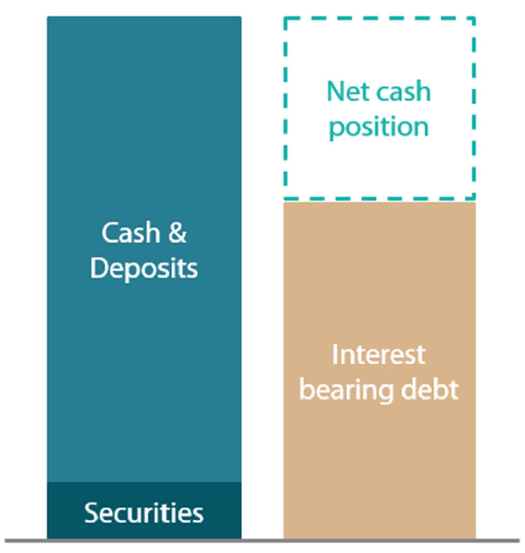

Japan is a nation of cash-rich companies, and it has been for decades. While cash-rich companies may not be a purely Japanese phenomena, there are many companies in Japan today that through their long-term corporate behaviour have accumulated large cash reserves. These businesses have significantly higher amounts of cash (and securities) relative to their operating needs, even after taking total debt into consideration.

Chart 1: Cash-rich companies

Source: Nikko AM (for illustrative purposes only)

The pros and cons of being cash-rich

There are, of course, two sides to cash-rich companies. Having significant liquid assets means strong balance sheets, offering companies invaluable downside protection during periods of uncertainty (as witnessed during the Great Financial Crisis). On the other hand, cash-rich companies face criticism from shareholders for hoarding cash and not investing enough in their businesses or returning it to shareholders, in other words, not putting their money to good use.

In our experience, there are cash-rich companies that are competitive globally, operating in profitable niche sectors. And a surprising number are to be found in the small and mid-cap space. This presents an investment opportunity, as we believe that many of these companies trade at a discount because they are “under the radar” of most equity analysts. Small and mid-cap companies have less analyst coverage than larger companies, which means there is less information available and greater opportunities for active managers to earn returns.

Why invest in cash-rich companies?

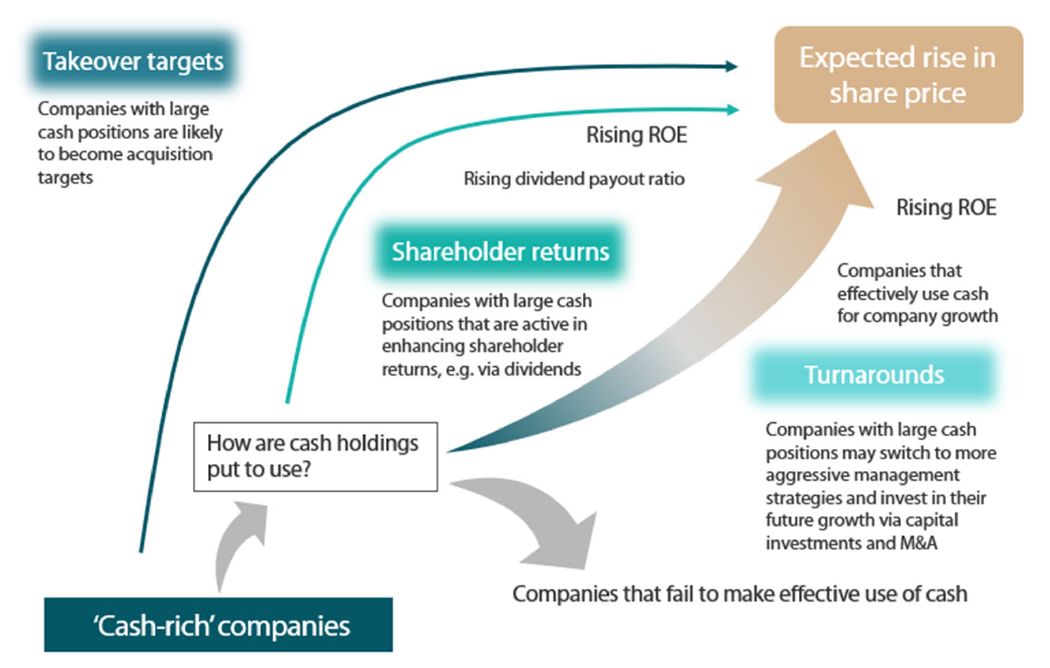

A cash-rich investment strategy involves investing in cash-rich companies whose share price is undervalued but is expected to benefit from an improved valuation in the future. The aim is to find companies with excess cash but are not capital-efficient, and then help these companies improve their capital efficiency by making better use of that cash, ultimately leading to better returns for investors. Specifically, there are three pathways to improving capital efficiency and increase the return on equity, which in turn leads to higher returns for investors:

-

Increase shareholder returns: This involves returning profits to shareholders either through increased dividends or share buybacks.

Investing in future growth: This involves more aggressive investment in new businesses (M&A) and projects to promote the company’s growth.

Become a potential takeover target: Being acquired by another company tends to increase the company’s value.

Chart 2: Three different scenarios for effective use of cash holdings

Source: Nikko AM (for illustrative purposes only). The diagram does not guarantee future performance.

Cash-rich companies have outperformed

In our research we have found that the accumulated total return of Japanese cash-rich companies has outperformed the broader TOPIX over both the medium to long-term (15 years), both in weighted average and equal-weighted terms. In other words, investing in cash-rich companies is effective, and furthermore, by selecting the right companies from within the cash-rich segment, higher returns can be achieved. Nikko AM has been following this investment approach since 2005 and has delivered outperformance since inception. The Japan Cash Rich Company Strategy is well-positioned to exploit investment opportunities unique to Japan, as well as benefitting from the structural tailwind of policy-driven corporate governance reform.

To learn more about unlocking hidden value in Japan, download the Nikko AM investment guide here.

Nikko AM team in Europe

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.