Japan, a nation of “cash-rich” companies, is undergoing corporate reforms aimed at raising valuation of companies by improving their capital efficiency. This includes leveraging existing corporate savings for shareholder distribution and investing for future growth. The reforms, along with cash-rich companies' historical outperformance and strategic options due to their ample cash holdings, make these firms well worth exploring.

A country of cash-rich companies

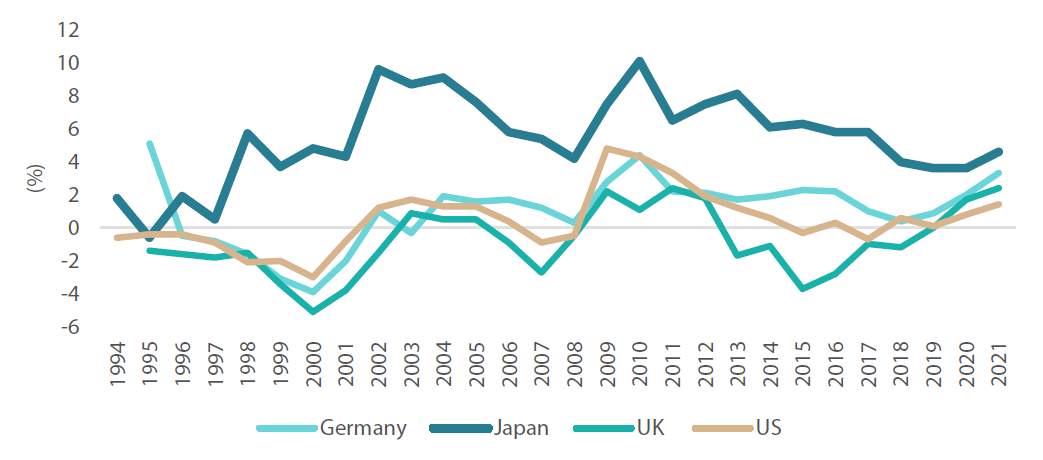

With its firms having held a higher amount of savings than those in other developed economies over the past three decades (Chart 1), Japan can be described as a country of “cash-rich” companies. As with many aspects of Japan’s economy, the bursting of the asset bubble in the 1990s played a significant role in shaping corporate behaviour. After the bubble burst, Japan entered a long period of economic stagnation during which corporate investment slowed. Company profits were instead channelled into savings, turning many of them into net holders of cash.

Chart 1: Corporate net savings (% of GDP, 1994-2021)

Source: OECD

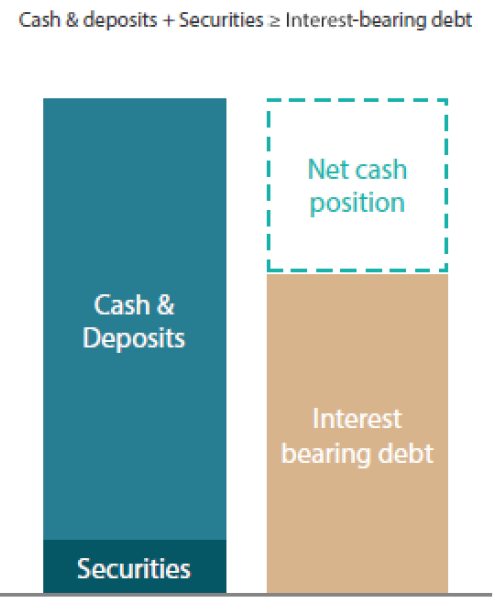

Japan went on to experience many years of deleveraging with corporate cash diverted to interest payments. This resulted in the proliferation of cash-rich companies, often defined as firms whose holdings of cash & deposits and Securities are greater than their interest-bearing debt (Exhibit 1).

Exhibit 1: Cash-rich companies

Source: Nikko AM

There are two sides to cash-rich companies. Having significant liquid assets means strong balance sheets for companies during market turbulence; it also enables them to be generous with dividend payments and share buybacks. On the other hand, shareholders can criticize cash-rich companies for hoarding and not investing enough in their businesses—in other words, not putting their money to good use. However, Japan is undergoing significant corporate governance reforms. Thanks to these policy tailwinds, potential changes in behaviour, such as more actively using cash, are expected to unlock shareholders value and enhance the attractiveness of cash-rich companies.

How governance reforms were initiated

With the bursting of the bubble, the influence in the Japanese equity market of financial institutions, saddled by mountains of bad loans, waned, while the presence of activists and foreign investors increased in the recent years. This led to increased scrutiny of corporate practices which had plagued Japan. These included “parent-subsidiary” listings (when a parent company and its subsidiary are listed on the same exchange, often creating conflicts of interests between the parent companies and the minority shareholders), cross-shareholdings, use of takeover defence measures and neglect of minority shareholders.

Against such a backdrop, the administration of then-Prime Minister Shinzo Abe declared in 2013 that corporate governance reform would be one of the main agendas of its Abenomics policies intended to revive the economy after two decades of stagnation. Japan followed through with the introduction of the Stewardship Code in 2014 and the Corporate Governance Code in 2015.

The purpose of the Corporate Governance Code is to encourage engagement between companies and shareholders to promote sustainable growth and increase corporate value, with changes in investor expectations now being expressed via proxy voting. As a result, companies must become more efficient to maximize shareholder returns.

In March 2023, the TSE requested that listed companies improve their capital efficiency as return on equity (ROE) in Japan has been historically low by international standards. This move successfully encouraged companies to set targets (or projections) of dividends or share buybacks, especially in April and May 2024 to coincide with their full-year earnings. This positive trend will likely continue to raise investment opportunities over the medium term. More importantly, some listed companies announced projections to grow earnings through better use of capital, i.e., increase in capex to pursue earnings growth. The revival of the Japanese economy is expected to support these growth opportunities over the medium term.

We believe that the ongoing reforms could further result in many cash-rich firms engaging in the following measures:

-

Utilising excess cash: effectively improving companies’ earnings and/or shareholder distribution

Addressing parent-subsidiary listings: unlocking value by divesting or by making it into a fully consolidated subsidiary

Reduction in cross-shareholdings: unlocking value as it involves firms with numerous cross-shareholdings buying back their own shares

Other features that make cash-rich companies attractive

In addition to the policy tailwinds mentioned above, there are three other characteristics that make Japan’s cash-rich companies attractive.

-

Strong track record of outperformance

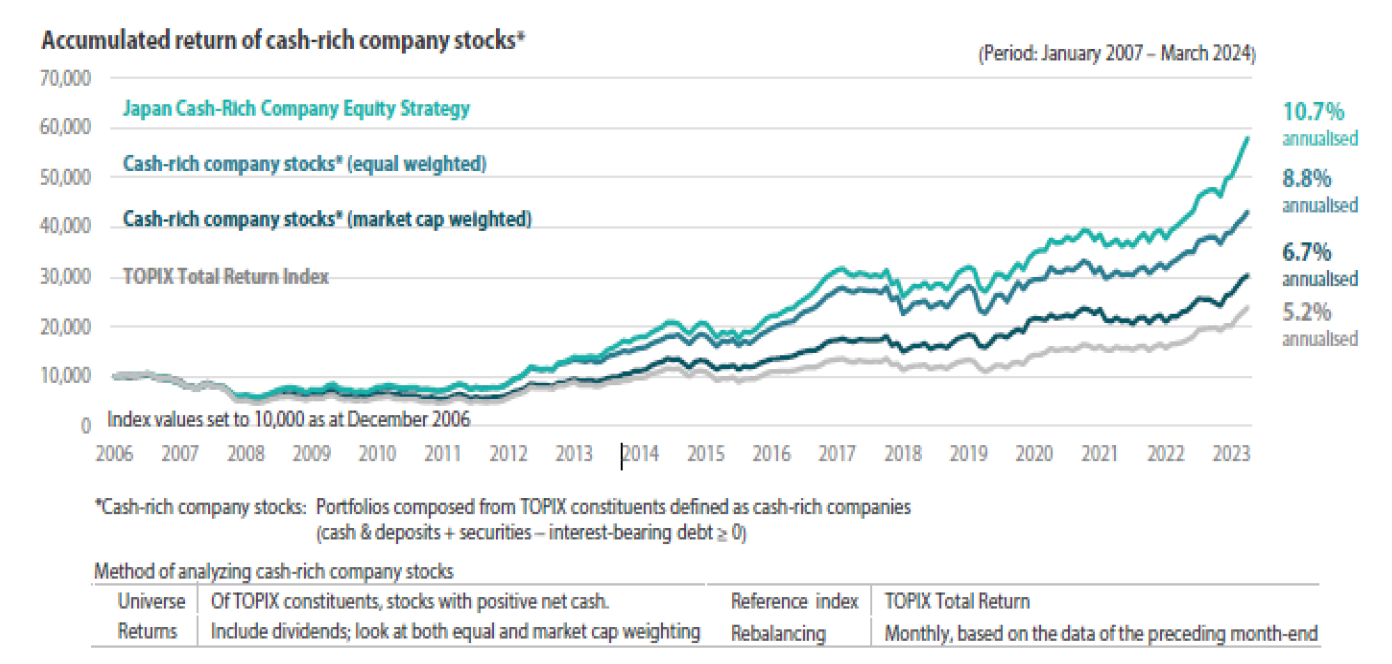

Cash-rich companies have outperformed the market over the last 17 years, offering attractive returns even during challenging market conditions (Chart 2).

Chart 2: Cash-rich companies have outperformed

*Cash-rich company stocks: Portfolios composed from TOPIX constituents defined as cash-rich companies (cash & deposits + securities – interest-bearing debt ≥ 0)

The data shown represents past performance and is not a guarantee of future returns. Returns are Japanese yen based and are calculated gross of advisory and management fees and custodial fees, but are net of transaction costs and include reinvestment of dividends and interest.

Source: Nikko AM based on data deemed reliable; TOPIX Total Return Index data from JPX Market Innovation & Research, Inc.

-

Strategic options thanks to cash-rich companies’ ample cash

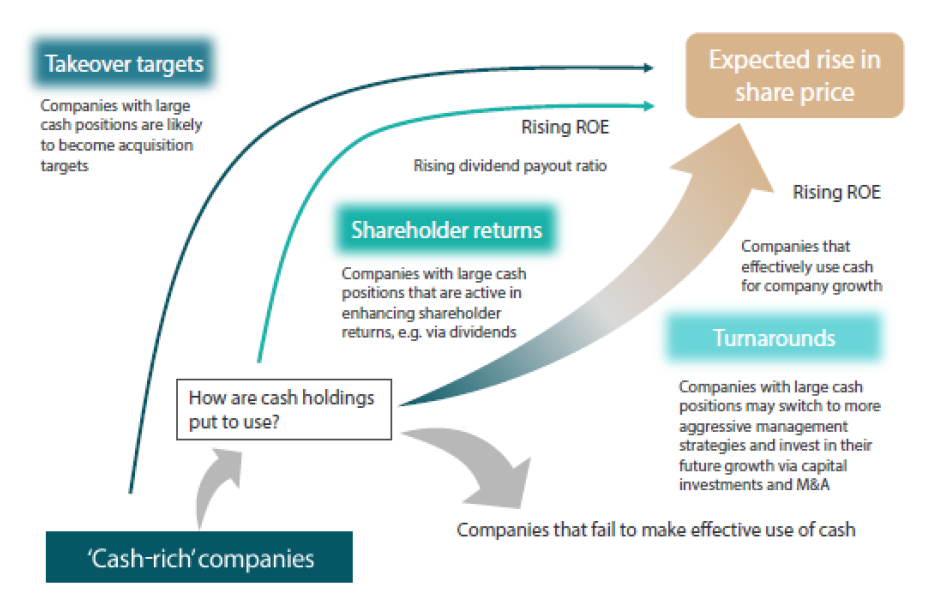

Cash-rich companies offer at least three investment scenario options: (1) “takeover targets”, (2) “shareholder returns” and (3) “turnarounds”. In our view, any of these scenarios can potentially lead to investment returns.

Exhibit 2: Three investment scenario options cash-rich companies offer

Source: Nikko AM

-

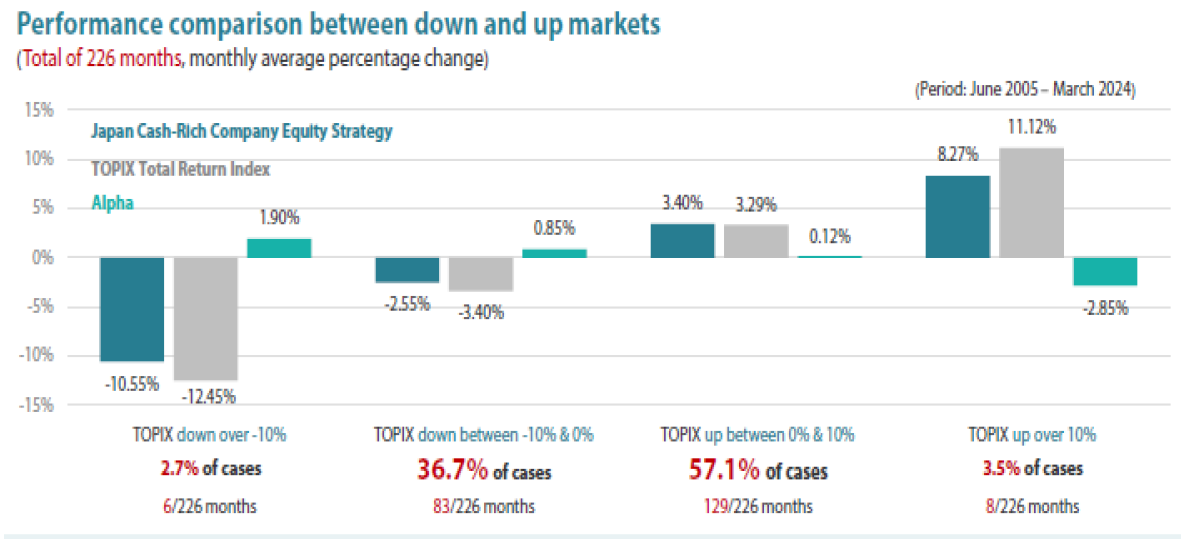

Downside protection

An investment strategy focused on cash-rich companies can not only keep pace during market upturns, but it can also offer protection during downturns, offering a concave investment return profile.

Chart 3: Cash-rich strategy keeps pace with market upturns, offers protection in downturns

The data shown represents past performance and is not a guarantee of future returns. Returns are Japanese yen based and are calculated gross of advisory and management fees and custodial fees, but are net of transaction costs and include reinvestment of dividends and interest.

Source: Nikko AM; TOPIX Total Return Index data from JPX Market Innovation & Research, Inc.

Strategy focused on undervalued cash-rich companies

While the Japanese equity market has rallied since early 2023, with the Nikkei Stock Average rising to a record high in July this year, the recovery in share prices has not been even. For example, smaller cap stocks have been underperforming larger caps since April 2023. Furthermore, some sectors have been lagging external demand-oriented sectors.

Nikko AM’s Japan Cash-Rich Company Equity strategy focuses on return opportunities where undervalued stocks, notably small to mid-caps and beneficiaries of Japan’s improving inflation outlook, support earnings growth over the medium term.

More specifically, the strategy is focused on undervalued cash-rich companies that are expected to improve their ROEs. This investment focus captures rising beneficiaries of Japan’s revival with more companies starting to improve their capital efficiency amid ongoing corporate governance reforms. The strategy’s expected holding period of portfolio stocks is three years, which helps to capitalise on the structural reform of corporate governance through ROE improvements. This approach gives the strategy the opportunity to leverage corporate actions to improve shareholder returns.

It is estimated that nearly half of TOPIX companies are not covered by sell-side analysts. This presents the strategy, through its own proprietary research, with the opportunity to uncover undervalued smaller cap stocks that have gone unnoticed. The strategy gains first-hand information through one-on-one meetings with firms’ management teams and key individuals. This process has succeeded in delivering attractive performance in the past. We believe that actively managed funds are now in a better position than passive funds to capitalise on opportunities to be found in Japan.

Case study 1: Union Tool Co.

A manufacturer of precision machinery with a large market share in printed circuit board drills.

The company is highly evaluated for the following factors:

- Demand is expected to increase for drills needed to support the growth of generative AI. Such drills require a high level of precision and are thereby products high in added value.

- The company produces its own manufacturing machinery in-house, differentiating it from its peers.

Case study 2: ASKA Pharmaceutical Holdings Co.

A pharmaceutical manufacturer with strength in gynaecology.

The company is highly evaluated for the following factors:

- The company’s products are highly growth-oriented, designed to address social issues in Japan by contributing to the advancement of women and tackling declining birthrates.

- The company is actively making an effort to increase shareholder returns and reduce cross-shareholdings.

Summary

A significant number of Japanese companies became cash-rich after the bursting of the asset bubble in the 1990s as many channelled profits into savings. Despite criticisms, these cash-rich companies have come to possess strong balance sheets and have potential for generous dividend payments and share buybacks. Japan’s recent corporate governance reforms have encouraged companies to increase their shareholders value by utilising their excess cash and idle assets more proactively. These reforms, in addition to other factors, have enhanced the attractiveness of Japan’s cash-rich companies, making it an opportune time to focus on these undervalued and oft under-researched entities.

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way. There can be no assurance that any performance will be achieved in any given market condition or cycle. Past performance or any prediction, projection or forecast is not indicative of future performance.