Outlook for 2025

With 2024 mostly behind us, we are again reminded of how difficult it is to forecast asset market performance over the medium term. Coming into 2024, many pundits believed that a bond markets-supportive US recession was still on its way. However, the widely predicted recession never showed up. Instead, the MSCI World Global Equity index has risen about 19% year to date, while the Bloomberg Aggregate Bond Index has gained a modest 1.50%. Despite the difficulty in forecasting, we examine where markets could be headed in 2025. We are currently focused on a “no-landing” scenario, in which the US economy continues to grow at trend as the effects of a less restrictive monetary policy and a business-friendly Republican Party powers the economy forward.

A second Trump term: tax cuts, tariffs and central bank easing

With the Republicans taking control of both the House and the Senate, the economic outlook for US risk assets in 2025 has turned increasingly positive. While it is still too early to fully see all the party’s policy objectives, president-elect Donald Trump ran on a platform that included tax cuts, tariff implementation and immigration reform. During Trump’s first presidency, these policies were positive for US equities and credit spreads, while they had a negative impact on bonds.

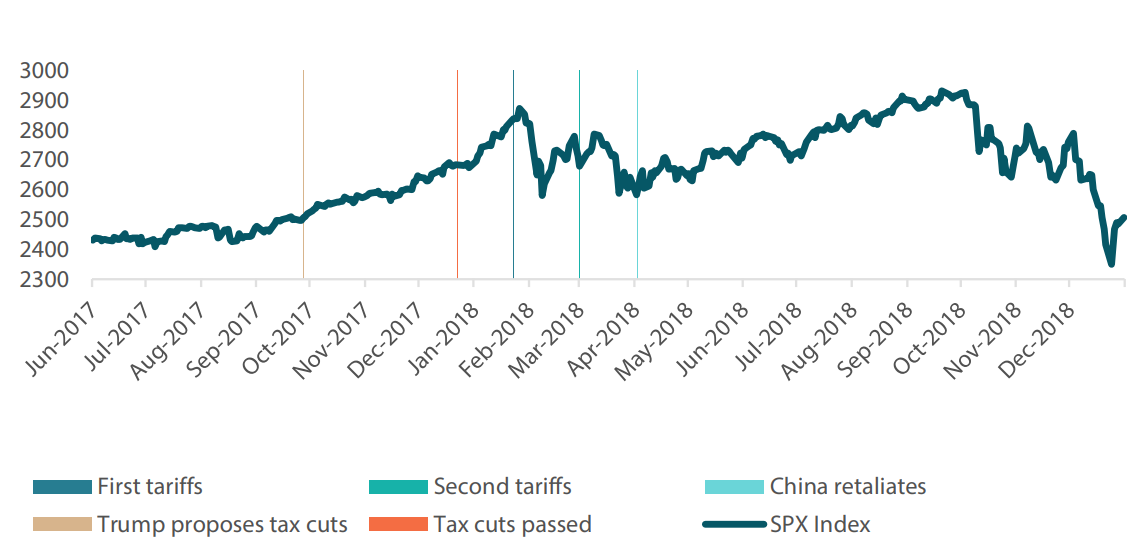

Chart 1 shows the performance of the US equity market as Trump’s key policies evolved during his first term. The market received the introduction of the tax cut plan very positively, while the introduction of tariffs led to poor market performance. However, the market rallied once the outlook became more established following China’s retaliatory measures.

Chart 1: Performance of S&P 500 following the introduction of tax cuts and tariffs

Source: Bloomberg, Nikko AM, November 2024

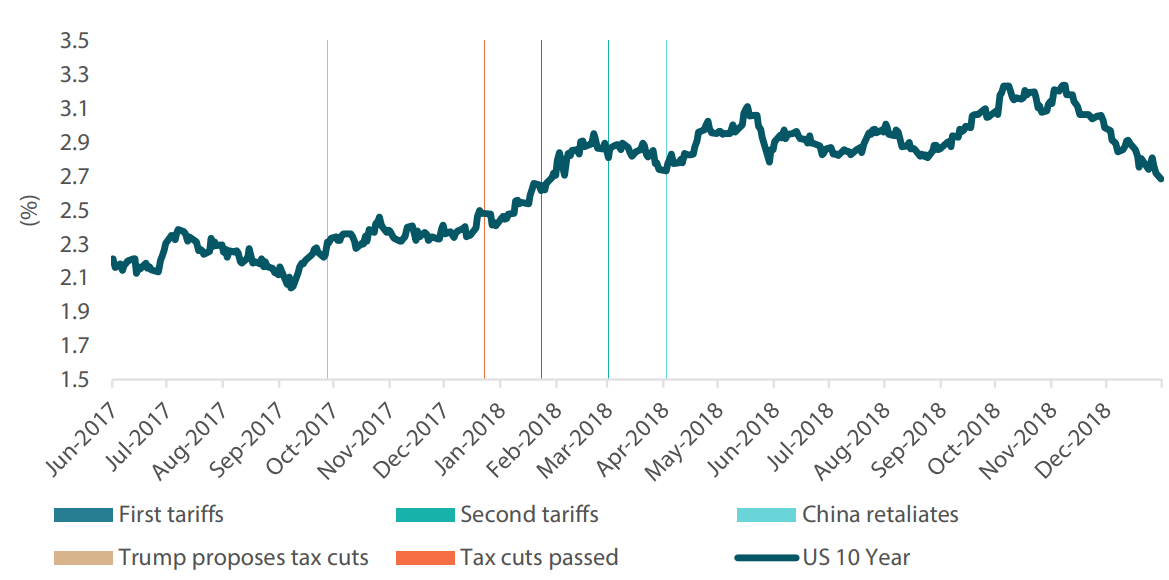

Within the bond market, Trump’s policies were viewed less favourably. Nominal bond yields and inflation breakeven pricing rose during the policy changes, as both tariffs and tax cuts were seen as inflationary by the market (Chart 2).

Chart 2: US 10-year Treasury yield following the introduction of tax cuts and tariffs

Source: Bloomberg, Nikko AM, November 2024

Looking ahead to 2025, we consider how the Republicans’ agenda could affect risk markets. We also gauge how far the US Federal Reserve (Fed), and other central banks could lower interest rates. We see monetary easing as positive for US equity markets; however, we expect a more nuanced view to emerge for bond markets amid the contrasting effects of expansionary fiscal policy and the impact of a falling Fed funds rate on yields.

Equity outlook: US, Japan and others

In terms of regions, we view the elections “Red Sweep” positively for US equities given the Trump administration’s inclination towards less regulation and corporate tax cuts. Certain sectors such as technology and banking may benefit from decreased scrutiny from government regulators. Likewise, the energy sector could see an increase in activities as more oil and gas exploration licenses are granted. The likelihood of increased fiscal spending points to stronger economic growth, while higher import tariffs should benefit domestic companies. Such a scenario may result in a stronger US dollar and a prolonged period of higher interest rates.

Higher import tariffs, especially on Europe and China, mean that corporates in those areas with revenue exposure to the US may struggle. In addition, economic data from Europe and China remain weak, and corporate earnings continue to underperform. Emerging markets (EM), which have a negative correlation with the dollar, are also likely to underperform. This is because EM central banks may not be able to lower interest rates when defending their domestic currencies against higher US interest rates. Given these prospects, we take a cautious view towards EM regions in 2025.

In contrast, Japan could be the only country to benefit from a stronger dollar. As many large Japanese corporates are exporters, a weak yen is positive for corporate earnings. However, the current volatility of the yen poses challenges for global investors, and we would look to deploy capital only after the yen stabilises at a lower level. Valuation is not the only attractive story in Japan. The country’s improving corporate governance and capital returns also present strong structural narratives in the medium term.

Global rates: US versus Europe

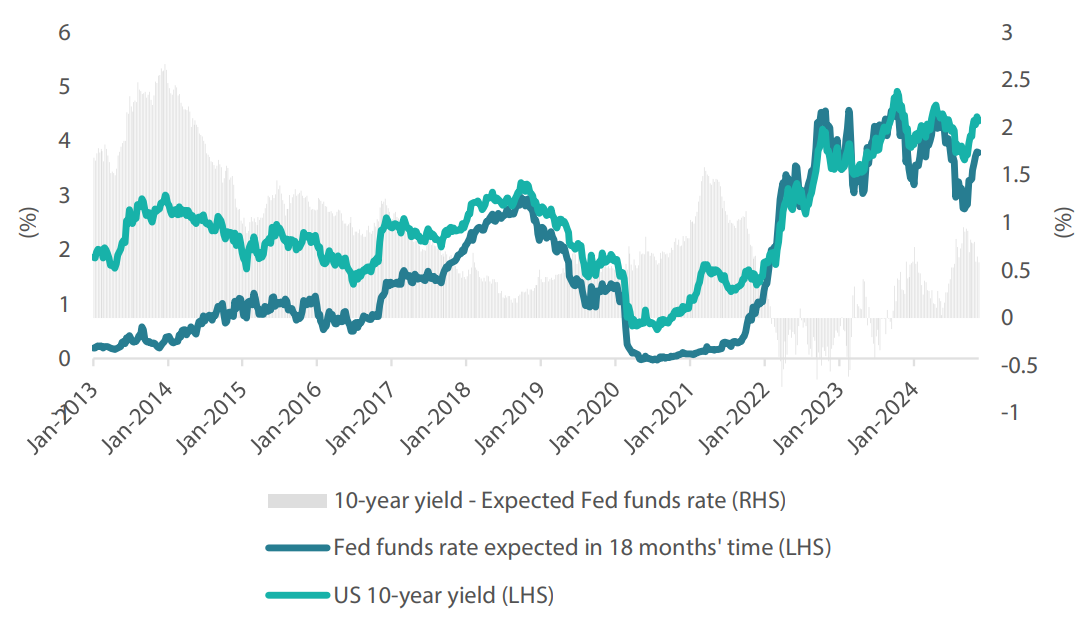

While the market experienced a rapid sell-off following the Republicans’ election sweep, bonds now appear to be approaching levels which we believe are relatively fair. One key measure to determine expected yields in the short term is how they trade relative to the market’s expectations for cash in 18 months’ time. Over the past 10 years, longer-dated US bond yields have traded on average at 60 basis points (bp) over the market’s expectations for the Fed funds rate in 18 months’ time (Chart 3). Therefore, when determining the “fair value” for the bond market, an understanding of where the Fed funds rate may land should serve as a guide.

Chart 3: US 10-year Treasury yield vs. Fed funds rate expectations

Source: Bloomberg, Nikko AM, November 2024

For 2025, we see the market trying to navigate an expansionary Republican policy agenda at a time when the Fed sees a diminished need for restrictive monetary policy. We expect the second Trump presidency to be marginally more inflationary, with inflation seen in the mid 2% range and slightly above the Fed’s target. For the Fed, this should necessitate a positive real rate of around 1–1.5% to control inflation and achieve the 2% goal. Putting these numbers together, we expect a Fed funds rate of 3.5–4.0%, which in turn means an anticipated range of 4.5–5.0% for US 10-year bond yields.

Outside of the US, we like European and French government bonds, as inflation in the eurozone has dropped back to 2% and gross domestic product (GDP) growth remains below 1%. Trump, who is focused particularly on China, could make global trade more challenging and cause the dollar to appreciate. A stronger dollar could prompt the European Central Bank (ECB) to cut rates more aggressively than the US in order to stimulate the euro zone’s sluggish economy. Such action by the ECB could be supportive of European bond markets.

Dollar/yen in a higher-for-longer environment

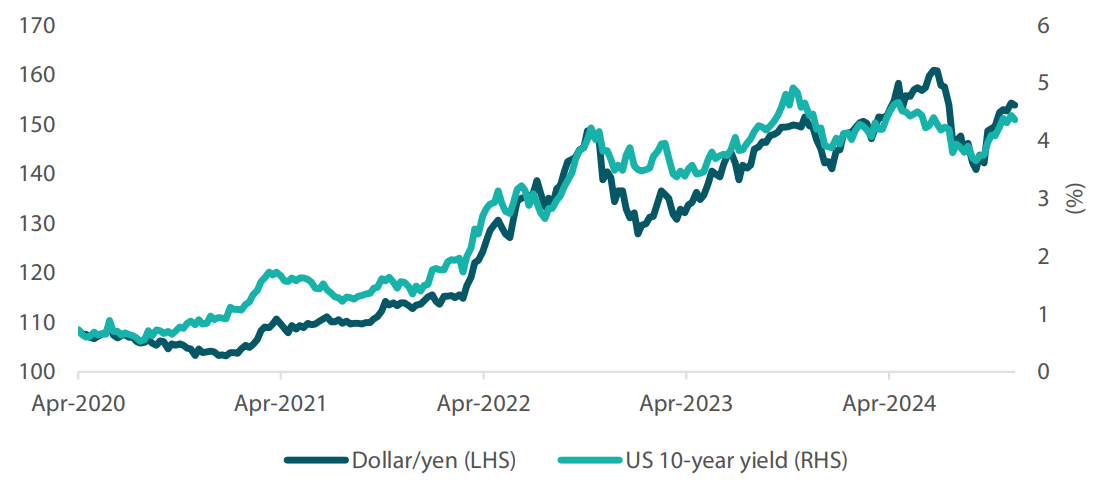

This higher-for-longer interest rate environment should continue to support the dollar against the Japanese yen. Although the Bank of Japan is on track to continue hiking rates, it is doing so at a far slower tempo relative to the pace at which the markets expect the Fed to cut rates. Since 2020, dollar/yen has shared a strong correlation with the US 10-year yield (Chart 4). The yen could be kept mostly rangebound at levels similar to those of 2023 if the US 10-year yield stabilises in a 4.25–4.75% range.

Chart 4: Dollar/yen and the US 10-year Treasury yield

Source: Bloomberg, Nikko AM, November 2024

If the yen stabilises at its current level, going long on the dollar against the Japanese currency would provide strong levels of carry and benefit portfolios in turn. Such positions also provide diversification against both US Treasuries and the S&P 500. As shown in Table 1, the correlation between bonds and equities is positive, while the US dollar is negatively correlated to risk assets and bonds. Therefore, for multi asset portfolios, a high US interest rate structure provides the benefits of both additional yield and diversification from an asset allocation perspective.

Table 1: Correlation between asset classes

Source: Bloomberg, Nikko AM, November 2024

Bond-equity correlation: the regime switch

The outlook is always a crucial factor when we construct multi asset portfolios. However, the correlation structure plays a large role in the final asset allocation. Since 2022, the bond-equity correlation has become positive; this has resulted in duration amplifying equity risk rather than diversifying it. As we head into 2025, our covariance matrix shows that this new regime is still at play, with most bond markets having a positive correlation to equities.

This means that forecasting bond yields and trying to time the performance of the US Treasury market can always be an interesting exercise. From an asset allocation perspective, our quantitative-driven portfolio construction process favours short-dated credit markets (such as Australia and Canada), China bonds, gold, and the dollar to reduce volatility in portfolios. These market segments exhibit lower volatility and correlations than traditional risk-free assets such as US Treasuries.

Summary

Generally, our outlook for 2025 is relatively positive. We expect the business-friendly stance of the Republican Party, coupled with easier monetary policy, will be supportive for risk assets, particularly in the US market. We are less bullish about US Treasuries, as a Fed funds rate of 3.50% would make long-dated bonds a marginally attractive proposition. Outside of the US, we have a more positive outlook on bond markets, but we are less positive about risk assets given the uncertainty of Trump’s trade policies.

While we hold various views, we rely on our strategic asset allocation to guide our long-term outlook—with healthy equities, short-dated credit, the US dollar and gold forming our backbone for the medium term.