In the last few weeks, we have had a spell of rather stormy weather in the UK, and between the rain and wind it has been good to escape for some fresh air. Even my local beach in Scotland has become a surf destination for a while. For some reason surfing has always had a particular appeal for me personally, with the combination of exercise, outdoors and the complete distraction of battling the elements being a particularly attractive combination. Sadly, my skills and flexibility have made my attempts at actually standing up on a board best described as disappointing, or once relayed by my children as downright embarrassing!

Source: author

Source: author

Surfing is a pretty good analogy also for the evolution in markets we have been seeing. From 2009 onwards we have been in an environment where central banks have done everything possible to smooth out volatility and this has conditioned many investors to assume that markets are relatively predictable.

The regularity at which quantitative easing (QE) was used to smooth out the unexpected such as the Euro crisis—or more lately COVID lockdowns—has become locked into data series, asset owner allocations and general investor psychology. In surfing parlance, the markets had become an easy beach break suitable for beginners.

Source: Shutterstock

Source: Shutterstock

Suffice to say, that particular game is over. The conducive swell has gone from the beach we all enjoyed for so long. The emergence of notable inflation has changed the game, as recovering lost credibility is now the paramount goal of central banks. As a reminder, US 10-year Treasuries yielded 0.508% in August 2020 and are yielding 4.6% as of this writing. In the UK a similar punishing shift in the cost of borrowing has taken place with 10-year gilts over the same period rising from a low of 0.077% to 4.29%. Borrowing costs in the US dollar, the world’s reserve currency, have risen 400 basis points. Translation costs for offshore borrowers have risen as a result of the higher dollar and credit lines may no longer even exist on renewal.

So, in reality we are heading to a new beach we have not surfed before and the situation is less predictable and a lot more gnarly. With the experimentation of QE and now quantitative tightening (QT) ongoing, this is new ground for both policy makers and investors. We don’t know the final level of policy tightening needed from central banks, the timing (though recent market actions suggest it is nearing) or the duration of tight policy before a reversal may commence.

Hence investors continue to adjust portfolios for “higher for longer” and the challenges of slowing growth. To return to the surfing analogy, 2023 has been all about picking the right board and finding the best and most consistent breaks on this newly discovered beach.

Picking the right spots in the market

Source: Shutterstock

Source: Shutterstock

The one thing we have been confident about throughout this year is that we have a trusted surfboard, our Future Quality philosophy. In our view, companies that can grow, attain and sustain superior returns on invested capital and have all the key quality pillars in place (Franchise, Management, Balance sheet and Valuation) are the best candidates for longer term alpha today as much as they have ever been.

However, picking the right spot on the beach to surf has proven to be a more erratic exercise than we expected. Given the lower growth and higher cost of capital regime we expected, the spots we particularly preferred at the beginning of the year were the following:

Enablers of the required spending on energy transition: This has been correct overall with Chart Industries (sold in Q3), Schneider and Linde all proving to be winners for portfolios.

Normalisation and structural growth in global travel to surprise: Booking Holdings, Amadeus and Samsonite have been positive contributors.

Providers and enablers of Healthcare Efficiency: incorrect so far with the majority of holdings lagging the benchmark.

However, by far the best “breaks” have been at spots we didn’t expect. These have presented the biggest challenges, and they are as follows:

Technology leaders have become the defensive havens of choice: we had technology marked as an area of the market likely to face headwinds resulting from an end to the cheap capital era and a more challenging environment for customer spending. This element may still prove to be a correct concern over time, but other positive attributes have completely swamped this thesis and hence we were downright wrong from an allocation perspective.

The catalysts for the leading performance of larger tech names, particularly in the first half of 2023, are more obvious with hindsight—emergence of artificial intelligence (AI) as a dominant force, high cash flow generation, proactive cost cutting to support profitability and strong balance sheets. In particular, AI is in a period of rapid growth that is generally independent of the broader economic cycle. Moreover, the larger technology firms have the starting ingredients of large data sets, existing AI engineers and the ability to spend large amounts of capital, and as a result are making the moats around their franchises deeper and wider. A degree of rerating from the depressed levels of late 2022 has hence been well deserved.

We had some exposure with holdings such as Microsoft and TSMC, but in short, we didn’t have enough of the affectionately named “Magnificent 7”. This has been a rather harsh reminder that like many successful managers we are not, and never will be right all the time. We have very much done some navel gazing on why we didn’t pick up on this trend quicker, whilst also making sure that we stick with rational type 2 thinking. Being wrong in timing is one thing, but being stubborn and relying on hope of market reversal is an enduring problem.

Hence, we have updated our research, forecast models and valuation analysis, and as a result there are some names on reappraisal that do now meet our Future Quality criteria. Over recent months we have added Synopsys, Nvidia and more recently Meta, with all of these market leaders benefitting from the rapid adoption of AI. Whilst AI has an element of hype it also has a high probability of being the game changing technology for the next generation, and the picks and shovels of the adoption phase will be leaders. The successful new business models or use cases of AI are an exciting area for our research. But it is too early to define the winners, with the Internet bubble of the 2000s being a possible parallel.

Obesity-management drugs go mainstream….for the few

AI is not the only new kid on the block. GLP-1 obesity-management drugs have also been in focus recently, as their successful regulatory approvals[1] have boosted the growth potential of leading providers Eli Lilly and Novo Nordisk, and, given the hype over the drugs, their valuations as well. Novo Nordisk’s P/E, which was in line with the healthcare sector globally in 2019, today trades at a 72% premium2.

The mirror image has been a notable de-rating of healthcare/consumer companies who have been identified as GLP-1 losers. Whilst the direction of thinking could be correct, it does remind us of the period when EV adoption was at peak frenzy back in 2020 and we saw auto parts-related companies being shorted by some investors on the basis that we would run out of cars needing repair rather quickly. We bought O’Reilly Automotive when the market made that particular misjudgment and it has notably rewarded portfolio returns since. We wonder if a similar scenario will be played out in the coming years with those identified as GLP-1 losers, and hence we continue to be happy holders of companies such as Abbott, Danaher and Bio-Techne.

Tough environment favours unique business models

We have shared our experience and how we are learning where the leaders are more likely to be in this new higher-cost-of-capital regime. We describe them through the lens of common themes as this provides an easier understanding for many investors. But each and every company we own must meet the test of attaining and sustaining high returns on invested capital. Even better, we look for companies on a journey of sustainable improvement over the next five years, a tough journey at most times, and one made more difficult by the current economic headwinds.

These Future Quality paths are often rather unique to individual companies. Growing market share is one common characteristic of such companies, and we have already highlighted Meta as an addition, where the scale of ongoing share of the global pool of advertising being a key positive for that company. Ryan Specialty is another example and an addition to the portfolio in recent months, where rising share in the wholesale insurance brokerage market in the US is a key driver for above-average growth in this high return business. Our other insurance holdings, Palomar and Progressive, have similar above market growth due to their more unique business models.

Undercurrents in the current environment

Returning again to the surfing analogy, this new beach we are on has some notable undercurrents that are likely to be a persistent factor to consider. We would summarise them as follows:

Capital needs: many investors are still conditioned by the last decade, when capital has always been available, and for the most part way too cheap. In public markets the game has changed, and we would make the guess that a similar outcome will more fully develop in the private markets as the pipeline of dry powder eventually becomes exhausted. Within listed equity markets we observe that the risk premium between capital providers (large excess free cash being returned to investors today) and capital takers (profitability is insufficient to self-finance growth or is needed to service or payback debt providers) is widening. This widening of risk premiums due to operating risks and refinancing risks may have further to run, particularly where both risks are evident.

Pricing of low-volatility dividend yields

One of the features of the QE era was the search for low volatility yields in assets other than fixed interest, as the real yields were manipulated lower. There is a relationship therefore between the relative performance of these lower vol, higher dividend havens in the equity market, with consumer staples and utilities being suitable examples (Chart 1).

Chart 1: Consumer staples, utilities and 10-year US bond yields

Source: Bloomberg, November 2023

Whilst they will no doubt have some degree of haven status during periods of shorter-term crisis, higher real bond yields are encouraging investors to reappraise prior allocations to these companies. In addition, higher term premiums are impacting valuations, as longer duration debt on refinancing will also need more cash flow allocation that will no longer be available for equity holders. In short, they are becoming less of the defensive haven of choice and relatively cheaper valuations will likely persist or widen further until either real rates reverse or the asset owner reallocation dissipates as a driver.

Adapt to the conditions

The last few quarters have been a good reminder that we are in a changing world. Interest rates have gone up a lot more than most investors, including ourselves, expected. Geopolitics similarly are signalling an end to the peace dividend that has prevailed for the careers of most financial players, with ongoing developments in the tinder box of the Middle East being the current addition to ongoing uncertainty. Finally, we need to remind ourselves that QT has no notable precedent in the modern and highly leveraged financial world.

As a result, we need to focus always on investing in enduring franchises and we would suggest that our Future Quality approach is soundly placed in that regard. But valuation is also one of our pillars and still a key variable over shorter time horizons. Being the wrong side of these widening valuation dispersions is painful, whilst also being a comfortable momentum tailwind for the areas of the market attracting investor attention. It is difficult to know when these rotational forces will become exhausted or be altered by subsequent events, but it is probably fair to assume we are good way down that journey already. Hence, we think that a significant amount of caution and discipline is needed when building positions in prior winners, being diligent about the risks of “better value”. We also need to approach monetary policy with an open mind; sometime soon central banks could change the game again by reversing rate hikes, ending of QT or even going straight to an era of financial repression. In short, be ready with your trusted surfboard and make the most of the conditions.

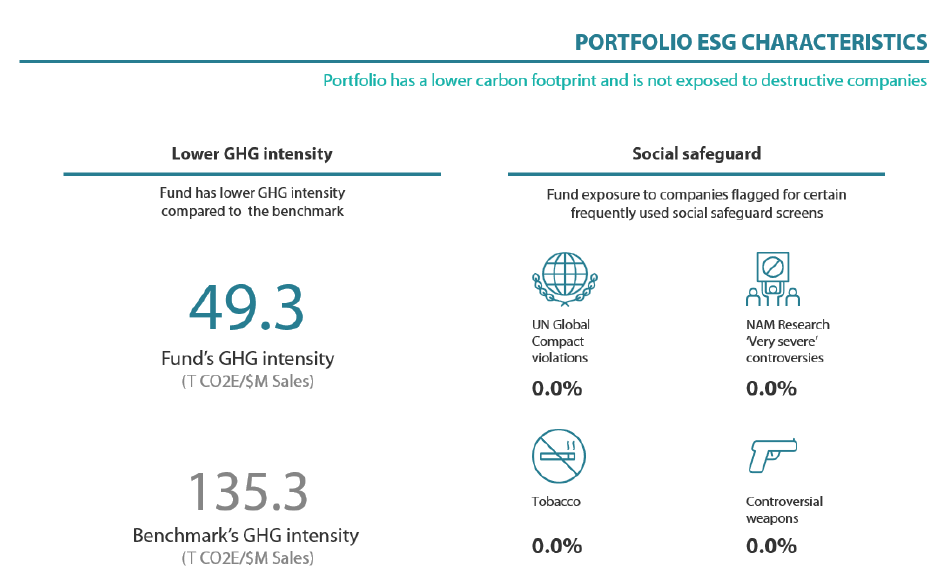

Source: MSCI ESG Research, NAM Research October 2023. Underlying score is the MSCI ESG Quality Score. Carbon Footprint is Weighted Average Carbon Intensity Fund is a representative account of the Nikko AM Global Equity Strategy. Benchmark is the MSCI ACWI. Any comparison to reference index or benchmark may have material inherent limitations and therefore should not be relied upon.

Global Equity strategy composite performance to October 2023

Past performance is not a guide to future returns.

*The benchmark for this composite is MSCI ACWI Net Total Return Index. The benchmark was the MSCI ACWI ex AU since inception of the composite to 31 March 2016. Inception date for the composite is 01 October 2014.

Returns are based on Nikko AM’s (hereafter referred to as the “Firm”) Global Equity Strategy Composite returns. Returns for periods in excess of 1 year are annualised. The Firm claims compliance with the Global Investment Performance Standards (GIPS ®) and has prepared and presented this report in compliance with the GIPS. GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Returns are US Dollar based and are calculated gross of advisory and management fees, custodial fees and withholding taxes, but are net of transaction costs and include reinvestment of dividends and interest. Copyright © MSCI Inc. The copyright and intellectual rights to the index displayed above are the sole property of the index provider. Any comparison to a reference index or benchmark may have material inherent limitations and therefore should not be relied upon. To obtain a GIPS Composite Report, please contact This email address is being protected from spambots. You need JavaScript enabled to view it.. Data as of 31 October2023.

Nikko AM Global Equity: Capability profile and available vehicles

(as at October 2023)

")

Target return is an expected level of return based on certain assumptions and/or simulations taking into account the strategy’s risk components. There can be no assurance that any stated investment objective, including target return, will be achieved and therefore should not be relied upon. Any comparison to a reference index or benchmark may have material inherent limitations and therefore should not be relied upon.

Past performance is not indicative of future performance. This is provided as supplementary information to the performance reports prepared and presented in compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually “joining the dots” across geographies, sectors and companies, to find the opportunities that others simply don’t see.

There are four key areas that make our strategy different:

- a focus on Future Quality companies – a different and clear philosophy

- a distinctive team culture – a tight-knit team with a process built on openness and respect

- unique execution, including rigorous team challenge of every idea

- differentiated portfolios, with a strong track record in stock-picking and ESG integration

Future Quality companies

We believe that companies with superior long-term returns on investment will deliver better performance. We call these Future Quality companies, and it is only these companies that make it into client portfolios. We search for Future Quality through analysis and financial modelling of companies that we expect to deliver over the next five years, and beyond. This approach is supported by academic evidence that businesses with high and improving returns on invested capital provide superior compound performance over the long term. With this investment time horizon, the sustainability of returns is a crucial ingredient of our Future Quality approach. We have found that companies developing solutions to ESG issues and management teams providing value to all stakeholders are more likely to be successful at sustaining high returns on invested capital over the long-term.

Distinctive team structure and culture

We believe that our collective knowledge and experience are powerful tools for delivering investment performance. Since 2011, we have operated a team-based approach to uncovering Future Quality investment ideas and have fostered a strong group dynamic. Individually, each Portfolio Manager is an expert investor with a broad skillset and experience of many market cycles.

We work in a flat structure, where all our Portfolio Managers have a dual role that combines investment analysis and investment management responsibilities. With individual analytical coverage split along industry lines, each Portfolio Manager is a specialist in the stocks and sectors they cover.

We all actively challenge the ideas and analysis of colleagues throughout the investment process, in an open atmosphere of vigorous and constructive debate. Portfolio Analysts work alongside Portfolio Managers, typically researching thematic trends that could influence and uncover future investment opportunities.

We take collective responsibility for approving stocks for the portfolio, and therefore there is joint accountability for performance. As such, it is in everyone’s interest to ensure that the investment analysis is thorough and that no stone is left unturned in the search for Future Quality.

We believe that the broad experience of our Portfolio Managers and distinctive team-based approach that sees everyone contributing to the strategy, increases the probability of successfully uncovering Future Quality.

Unique execution

Our tight-knit team approach and flat structure enable us to execute in a transparent way, including a rigorous team challenge of every idea. By using our strict Future Quality standards, we can identify long-term winners from the broader universe, to narrow down a comprehensive watch list and around 100 deep dive researched ideas. This is within a unique framework of individual accountability for the underlying analysis and company research, combined with the collective challenging of assumptions at the team level. Our proprietary ranking tool creates a disciplined process to compare and rank attractive opportunities and ensures that at the portfolio construction phase, only our best-ranked ideas receive the most committed weights in client portfolios. We believe our culture is key, and the collective ownership of our research process brings the best portfolio outcomes for clients.

Differentiated portfolios

We deliver a high-conviction Global Equity strategy for clients that is not constrained by benchmarks. As such, Future Quality can be sourced from listed businesses across any geography or sector. And, in a world awash with investment prospects, our disciplined, accountable and transparent process helps us to focus solely on building portfolios from companies that best meet our specific Future Quality criteria.

In terms of balancing risk and reward, our track record shows that we consistently deliver attractive returns on a lower risk-adjusted basis compared with peers and the global reference benchmark. The high active share and concentrated number of holdings help ensure that our Future Quality stock-selection process delivers differentiated portfolios.

About Nikko Asset Management

With USD 211.0 billion* under management, Nikko Asset Management is one of Asia’s largest asset managers,

providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In addition, its complementary range of passive strategies covers more than 20 indices and includes some of Asia’s largest exchange-traded funds (ETFs).

*Consolidated assets under management and sub-advisory of Nikko Asset Management and its subsidiaries as of 30 September 2023.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the strategy will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.

If you intend to invest in the UCITS Fund, please refer to the Fund Prospectus in order to identify whether the Sub-Fund will manage sustainability factors within the meaning of the SFD Regulation (EU) 2019/2088: an article 6 (limited to analysing sustainability risk as part of its risk management process), an article 8 (which also promotes certain environmental and social characteristics) or article 9 (which has sustainable investment as its primary objective).

For Professional Investors only. This is a marketing communication. Please refer to the UCITS prospectus and to the KIID before making any final investment decisions

1US and UK regulators approved Eli Lilly’s obesity-management drug in November 2023; they approved Novo Nordisk’s drug in 2021

2Bloomberg, November 2023

There can be no assurance that any performance will be achieved in any given market condition or cycle. Past performance or any prediction, projection or forecast is not indicative of future performance.

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way. Past performance or any prediction, projection or forecast is not indicative of future performance.

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way. There can be no assurance that any performance will be achieved in any given market condition or cycle. Past performance or any prediction, projection or forecast is not indicative of future performance.

Any comparison to a reference index or benchmark may have material inherent limitations and therefore should not be relied upon. There can be no assurance that any performance will be achieved in any given market condition or cycle. Past performance or any prediction, projection or forecast is not indicative of future performance.