Global equity investment philosophy

Our philosophy is centred on the search for “Future Quality” in a company. Future Quality companies are those that we believe will attain and sustain high returns on investment. ESG considerations are integral to Future Quality investing as good companies make for good investment. The four pillars we use to assess the Future Quality characteristics of an investment are:

Franchise—does the company have a sustainable competitive advantage?

Management—does the company make sound strategic and capital allocation decisions?

Balance Sheet—is growth appropriately financed?

Valuation—are the company’s prospects under-appreciated by the market?

We believe that investing in Future Quality companies will lead to outperformance over the full market cycle. Our strategy is based on fundamental, bottom-up research therefore sector and country allocations are a function of stock selection. The Global Equity strategy is a concentrated, high conviction portfolio with a high active share ratio.

Market outlook

Equity market leadership continues to be driven by rising confidence in the positive impact of abundant liquidity and ongoing / increasing government support. This is manifesting itself in rising inflation expectations and bond yields and provides something of a headwind for long duration growth stocks.

Inflation expectations are rising for understandable reasons. Too many resources are visibly in the wrong place at the wrong time and this is leading to a pronounced squeeze up in prices. The blocking of the Suez Canal by the container ship Ever Given in March provided further short-term dislocation, by closing a meaningful route for global trade for six days. It looks likely, however, that this picture will improve significantly over the next 12 months, and enduring shortages of capacity look difficult to see at this stage. Importantly, labour markets still retain significant capacity and this is before we see what the new normal (with some measure of social distancing) means for employment levels in many service industries.

Hope and expectations are often inextricably linked. Many investors now expect (hope?) that policy makers will not rain on their parades by tightening interest rates any time soon. Who is leading who though? Is the Federal Reserve (Fed) ahead of the curve or willingly behind it and led by capital markets? Ironically, the more people that expect the Fed to stay supportive, the higher that asset prices will go and the more the imperative to act will grow. We all hope that policy makers will learn the lessons of the past in terms of avoiding unexpected moves, but, if you are a Fed policy maker, how do you avoid surprising the market with every single utterance poured over and even the tone of the message analysed to death?

Might other actors (rather than the Fed) be the first to gradually remove the punchbowl? Other countries (including China) have emerged from the pandemic more quickly and are starting to normalise monetary policy already. Other, private actors will have a role too and we will be monitoring bank lending standards and margin requirements for signs of increasing conservatism. The recent collapse of Archegos Capital Management and the resultant “firesale” of USD 30 billion of assets served as a reminder that liquidity isn’t always there when you need it, even if macroeconomic numbers suggest that it should be.

Coming back to inflation, one of the ways in which rising price expectations could pose a challenge for sustainable growth businesses is via their upward pressure on the discount rate used to arrive at today’s value of future cashflow (with this rate heavily influenced by reference government bond yields). We have been wary of using a market-derived discount rate for some time and have increased the rate that we use, to build in a measure of conservatism. Time will tell if we have built in enough of a buffer but our discipline on valuation will remain and we will continue to reduce our exposure to companies where we believe that we are being asked to reflect unrealistically low rates, even if we continue to like the franchise, management team and balance sheet.

Interestingly, although cyclical stocks have continued to lead the market, some of their defensive peers have started to improve somewhat. This could be a quarter end-inspired development rather than anything more substantial but Consumer Staples outperformed Consumer Discretionary in March and Real Estate and Healthcare both beat Information Technology.

Part of the reason for Tech’s underperformance is the unwinding of excessive positioning but another contributor is likely the flipside of the government largesse on the infrastructure spending that is propelling Basic Material and Industrial stocks higher. These bills will need to be paid for at some stage and increased taxation of the corporate sector seems to be a big part of this. No-one doubts the contribution of the US technology sector to the country’s long-term future and no US government would want to jeopardise the innovation that it brings, but the sector is a low tax area and has benefitted from a number of tax breaks that will likely be less generous in the future. This will act as a drag on profit growth relative to other parts of the economy.

The portfolio continues to have a barbell of attractively valued growth and more cyclical businesses. We have tended to find greater valuation support in the cyclical parts of the market in recent months, but we will only own businesses where we believe in the sustainability of their returns over the longer-term, even if economic growth slows.

In conclusion, the current environment continues to pose a modest headwind to performance relative to benchmark indices with greater exposure to lower quality cyclical stocks. That said, our ability to find Future Quality companies across a wide variety of sectors, whilst underweighting growth at any price is allowing us to stay in touch. Over the longer-term, we are confident that this approach will generate strong risk-adjusted returns for our clients.

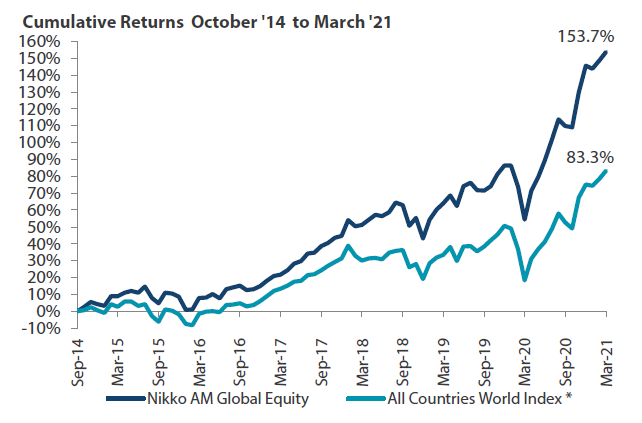

Comparative returns are against the MSCI All Countries World (ex Australia) Index

Global Equity Strategy Composite Performance to Q1 2021

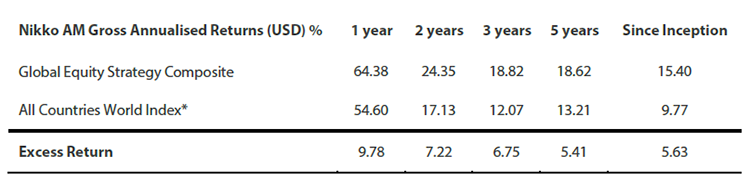

*The benchmark for this composite is MSCI All Countries World Index. The benchmark was the MSCI All Countries World Index ex AU since inception of the composite to 31 March 2016. Inception date for the composite is 01 October 2014. Returns are based on Nikko AM’s (hereafter referred to as the “Firm”) Global Equity Strategy Composite returns. Returns for periods in excess of 1 year are annualised. The Firm claims compliance with the Global Investment Performance Standards (GIPS ®) and has prepared and presented this report in compliance with the GIPS. Returns are US Dollar based and are calculated gross of advisory and management fees, custodial fees and withholding taxes, but are net of transaction costs and include reinvestment of dividends and interest. Copyright © MSCI Inc. The copyright and intellectual rights to the index displayed above are the sole property of the index provider. For more details, please refer to the performance disclosures found at the end of this document. Data as of 31 March 2021.

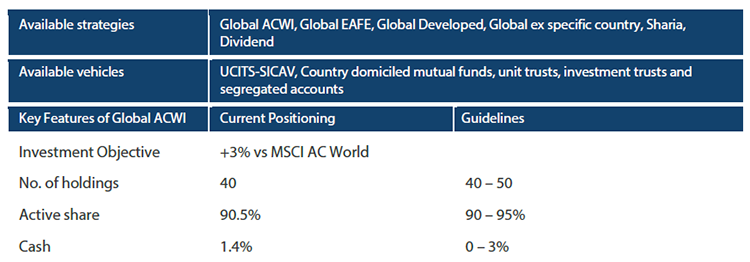

Nikko AM Global Equity: Capability profile and available funds (as at 31 March 2021)

Past performance is not indicative of future performance. This is provided as supplementary information to the performance reports prepared and presented in compliance with the Global Investment Performance Standards (GIPS®). Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually “joining the dots” across geographies, sectors and companies, to find the opportunities that others simply don’t see.

Experience

Our five portfolio managers have an average of 24 years’ industry experience and have worked together as a Global Equity team for eight years. Two portfolio analysts, Michael Chen and Ellie Stephenson joined in 2019 and are the first in a new generation of talent on the path to becoming portfolio managers. The team’s deliberate flat structure fosters individual accountability and collective responsibility. It is designed to take advantage of the diversity of backgrounds and areas of specialisation to ensure the team can find the investment opportunities others don’t.

Future Quality

The team’s philosophy is based on the belief that investing in a portfolio of Future Quality companies will lead to outperformance over the long term. They define Future Quality as a business that can attain and sustain high return on investment. We believe that ESG considerations and Future Quality investments are not independent of each other and as such the team evaluate the materiality of ESG factors when assessing the Future Quality potential of each stock.

Execution

Effective execution is essential to fully harness Future Quality ideas in portfolios. We combine a differentiated process with a highly collaborative culture to achieve our goal: high conviction portfolios delivering the best outcome for clients. It is this combination of extensive experience, Future Quality style and effective execution that offers a compelling and differentiated outcome for our clients.

About Nikko Asset Management

With USD 282.3 billion* under management, Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income and Multi-Asset strategies. In addition, our complementary range of passive strategies covers more than 20 indices and includes some of Asia’s largest exchange-traded funds (ETFs).

*Consolidated assets under management and sub-advisory of Nikko Asset Management and its subsidiaries as of 31 March 2021.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the Sub-Fund will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.