Global equity investment philosophy

Our philosophy is centred on the search for “Future Quality” in a company. Future Quality companies are those that we believe will attain and sustain high returns on investment. ESG considerations are integral to Future Quality investing as good companies make for good investment. The four pillars we use to assess the Future Quality characteristics of an investment are:

Franchise

- does the company have a sustainable competitive advantage?

Management

- does the company make sound strategic and capital allocation decisions?

Balance Sheet

- is growth appropriately financed?

Valuation

- are the company’s prospects under-appreciated by the market?

We believe that investing in Future Quality companies will lead to outperformance over the full market cycle. Our strategy is based on fundamental, bottom-up research therefore sector and country allocations are a function of stock selection. The Global Equity strategy is a concentrated, high conviction portfolio with a high active share ratio.

Market Outlook

The Isle of Lewis, the largest island of the Western Isles in northern Scotland, provides an ideal setting for stargazing due to its rural location—shooting stars and constellations are regularly visible in the night sky. Is it any wonder that Lewis’s ancient standing stones of Calanais, which are older than the Pyramids, are believed to be a prehistoric lunar observatory? While you sit and wonder how we got into this mess and what to do next, our ancestors would have looked to the stars above.

It is nearly a hundred years since Scottish inventor John Logie Baird made the first-ever television broadcast. He probably did not foresee television being the medium for broadcasting altercations between global leaders. The US President’s meeting at the White House with Volodymyr Zelensky was compelling in that the (perhaps?) unscripted outbursts provided an insight into how the world we live in is being run, while leaving the viewer to try to make sense of it all. History can act as a guide, though any framework you choose—from the end of the Roman Empire to former US President Richard Nixon’s “New Federalism”—is new to all professional investors. So, what should you do?

We firmly believe that markets remain inefficient, and the last few months are testament to that. Hence we face today's uncertainty level headed, attentive to where risks lie while also inquisitive about the potential opportunities. Rather than looking to the stars or world leaders for advice, we revert to our philosophy, Future Quality.

Of course, bouts of rotation and changes in style can happen—as has been the case over the last few months—but we believe that focusing on those with the ability to raise pricing and take market share should continue to drive outperformance. As ever, the four pillars of franchise quality, astute management, strong balance sheets and sensible valuations will underpin our ideas and discussions.

Over the past 12 months, we have relentlessly followed the process which has led us to de-risk the portfolio and reinvest profits into new Future Quality ideas. This continued in the first quarter with additions to more defensive names: Genpact Limited, Coca-Cola Europacific Partners plc and Kerry Group plc. These were funded out of lower conviction ideas such as Diageo plc and Coca-Cola Company but also higher US beta winners, in this case, Interactive Brokers Group, Inc. and TransUnion.

A slowdown in the US is likely, and hence we are attentive to any indicators, such as the recent fall in capex intentions evidenced by small business surveys or a slowing housing market might. While policy uncertainty reaches new highs, we are also equally alert to the opportunities the recent volatility can bring.

Finally, back to the Isle of Lewis and a lady called Mary MacLeod. She was born there in 1912, to Malcolm MacLeod, a fisherman, and his wife, who was also called Mary. Like many islanders before her, Mary left Lewis at the age of 18 for New York, where she met a local builder by the name of Trump. The rest, as they don’t say, is histrionics.

Reference to any particular securities or sectors is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way. There can be no assurance that any performance will be achieved in any given market condition or cycle. Past performance or any prediction, projection or forecast is not indicative of future performance.

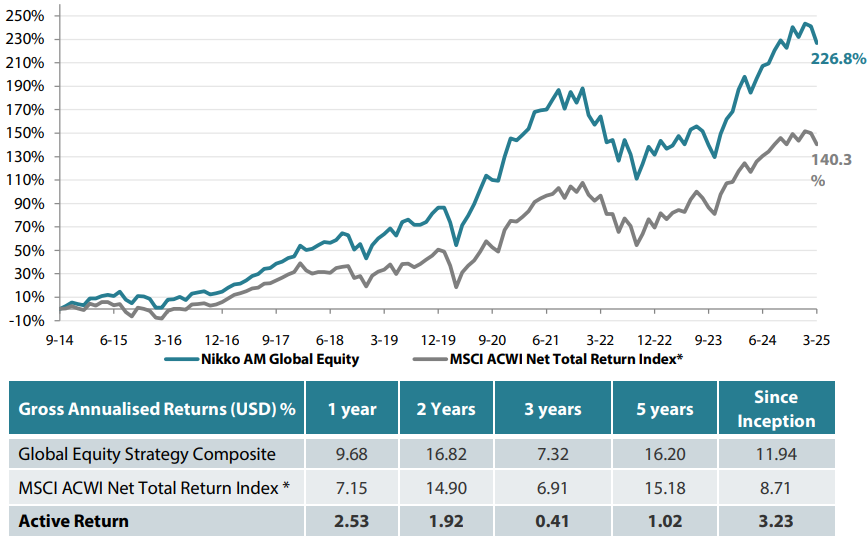

Global Equity strategy composite performance to March 2025

Past performance is not a guide to future returns. Source: Nikko AM, FactSet.

*The benchmark for this composite is MSCI ACWI Net Total Return Index. The benchmark was the MSCI ACWI ex AU since inception of the composite to 31 March 2016. Inception date for the composite is 01 October 2014. Returns are based on Nikko AM’s (hereafter referred to as the “Firm”) Global Equity Strategy Composite returns. Gross returns are presented gross of management fees, performance fees, custodial fees and withholding tax but net of all trading commissions. Returns for periods in excess of 1 year are annualised. Any comparison to a reference index or benchmark may have material inherent limitations and therefore should not be relied upon.

Data as of 30 March 2025.

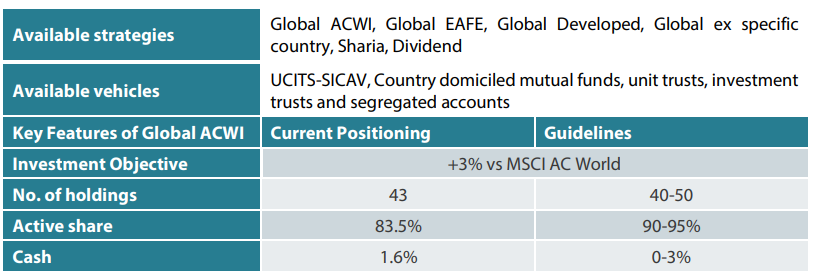

Nikko AM Global Equity: Capability profile and available vehicles (as at March 2025)

Target return is an expected level of return based on certain assumptions and/or simulations taking into account the strategy’s risk components. There can be no assurance that any stated investment objective, including target return, will be achieved and therefore should not be relied upon. Any comparison to a reference index or benchmark may have material inherent limitations and therefore should not be relied upon.

Past performance is not indicative of future performance. Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually “joining the dots” across geographies, sectors and companies, to find the opportunities that others simply don’t see.

There are four key areas that make our strategy different:

– a focus on Future Quality companies – a different and clear philosophy

– a distinctive team culture – a tight-knit team with a process built on openness and respect

– unique execution , including rigorous team challenge of every idea

– differentiated portfolios , with a strong track record in stock-picking and ESG integration

Future Quality companies

We believe that companies with superior long-term returns on investment will deliver better performance. We call these Future Quality companies, and it is only these companies that make it into client portfolios. We search for Future Quality through analysis and financial modelling of companies that we expect to deliver over the next five years, and beyond. This approach is supported by academic evidence that businesses with high and improving returns on invested capital provide superior compound performance over the long term. With this investment time horizon, the sustainability of returns is a crucial ingredient of our Future Quality approach. We have found that companies developing solutions to ESG issues and management teams providing value to all stakeholders are more likely to be successful at sustaining high returns on invested capital over the long-term.

Distinctive team structure and culture

We believe that our collective knowledge and experience are powerful tools for delivering investment performance. Since 2011, we have operated a team-based approach to uncovering Future Quality investment ideas and have fostered a strong group dynamic. Individually, each Portfolio Manager is an expert investor with a broad skillset and experience of many market cycles.

We work in a flat structure, where all our Portfolio Managers have a dual role that combines investment analysis and investment management responsibilities. With individual analytical coverage split along industry lines, each Portfolio Manager is a specialist in the stocks and sectors they cover.

We all actively challenge the ideas and analysis of colleagues throughout the investment process, in an open atmosphere of vigorous and constructive debate. Portfolio Analysts work alongside Portfolio Managers, typically researching thematic trends that could influence and uncover future investment opportunities.

We take collective responsibility for approving stocks for the portfolio, and therefore there is joint accountability for performance. As such, it is in everyone’s interest to ensure that the investment analysis is thorough and that no stone is left unturned in the search for Future Quality.

We believe that the broad experience of our Portfolio Managers and distinctive team-based approach that sees everyone contributing to the strategy, increases the probability of successfully uncovering Future Quality.

Unique execution

Our tight-knit team approach and flat structure enable us to execute in a transparent way, including a rigorous team challenge of every idea. By using our strict Future Quality standards, we can identify long-term winners from the broader universe, to narrow down a comprehensive watch list and around 100 deep dive researched ideas. This is within a unique framework of individual accountability for the underlying analysis and company research, combined with the collective challenging of assumptions at the team level. Our proprietary ranking tool creates a disciplined process to compare and rank attractive opportunities and ensures that at the portfolio construction phase, only our best-ranked ideas receive the most committed weights in client portfolios. We believe our culture is key, and the collective ownership of our research process brings the best portfolio outcomes for clients.

Differentiated portfolios

We deliver a high-conviction Global Equity strategy for clients that is not constrained by benchmarks. As such, Future Quality can be sourced from listed businesses across any geography or sector. And, in a world awash with investment prospects, our disciplined, accountable and transparent process helps us to focus solely on building portfolios from companies that best meet our specific Future Quality criteria.

In terms of balancing risk and reward, our track record shows that we consistently deliver attractive returns on a lower risk-adjusted basis compared with peers and the global reference benchmark. The high active share and concentrated number of holdings help ensure that our Future Quality stock-selection process delivers differentiated portfolios.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the strategy will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.

If you intend to invest in the UCITS Fund, please refer to the Fund Prospectus in order to identify whether the Sub-Fund will manage sustainability factors within the meaning of the SFD Regulation (EU) 2019/2088: an article 6 (limited to analysing sustainability risk as part of its risk management process), an article 8 (which also promotes certain environmental and social characteristics) or article 9 (which has sustainable investment as its primary objective).

Any investment in the Fund may only be made on the basis of the current Prospectus and the Key Information Document (KID), as well as the latest annual or interim reports.