Rate hike highlights apparent improvement in BOJ's communication

In a widely expected move, on 24 January the Bank of Japan (BOJ) hiked interest rates by 25 basis points (bps) to 0.5%, their highest level since 2008. The last time the BOJ hiked rates in July 2024, market conditions were notably different. Back then, Japan's equity market sank in the wake of the central bank's monetary tightening. Many attributed this equity market slump, dubbed the “BOJ shock” by some, to the rate hike. However, a more plausible explanation is that the BOJ's tightening roughly coincided with the release of weak US employment data. This not only damaged global equity sentiment but also triggered a rapid appreciation of the yen, leading to a sharp reversal in the Japanese market. This time, however, the market took the BOJ's move in stride. The market had time to price in a possible rate hike after BOJ Governor Kazuo Ueda and Deputy Governor Ryozo Himino hinted at possible tightening. In this regard, the BOJ's improved communication with the market was evident.

While its market messaging may have improved, the BOJ remains cautious in its approach. Taking the central bank's caution into account, market participants expect only one more rate hike in 2025. Their focus has already shifted to the timing of the next rate hike and how the BOJ intends to communicate its intentions. The BOJ's cautious approach reflects its fear of prematurely stifling inflation by hiking rates. Inflation appears firmly entrenched and the BOJ's concerns may appear overblown. However, we are likely to see the central bank continuing to act with prudence rather than haste.

In addition to inflationary trends, the BOJ will also have to keep an eye on the impact of the US administration's policies on the markets. The long-term impact US policies could have on the markets and the economy remains uncertain. However, statements from Washington have caused market volatility and their short-term impact cannot be ignored. From the BOJ's perspective, the central bank is likely hoping that any declarations from the White House will not result in a sustained rise in dollar/yen during its ongoing rate-hiking cycle. Thus, when contemplating future monetary policy, the BOJ may have to consider dollar/yen volatility during the current US presidential term.

Japanese economic resilience in focus amid flurry of trade-related news

Actions and statements by US President Donald Trump are dominating news headlines and the markets are feeling the impact as well. However, when viewed from a longer term perspective, the impact of these headlines on Japan's market is likely to be more psychological than tangible. It is worth focusing on what is happening on the ground domestically. Wages in Japan have been rising and are set to surpass inflation, which is more significant than tariff-related developments from an economic perspective.

The tariffs the US may impose on trade partners such as Japan should not be downplayed, particularly considering the potential impact on exporters. Japanese exporters could also come under pressure should the yen begin to appreciate on Japanese and US monetary policy developments. However, if the steady rise in wages can be maintained—ideally at about 3% for the next two years— it will stimulate domestic demand and help offset slower growth by exporters. Wage growth surpassing inflation will further increase consumption, providing a particular boost to small and medium-sized enterprises, as well as consumption and construction-related sectors. If the BOJ raises interest rates, the banking sector will receive a further lift as well. These are the areas that the market may focus on, potentially giving broader equities the lift they need for 2025.

Regarding exporters, the rise in wages and the labour shortages Japan is currently experiencing are changing the country's profit sources. Compared to the Abenomics era, Japan is no longer as dependent on its exporters, who were in turn reliant on US demand. This shift is due to the fact that rising wages and labour shortages have broadened and deepened the scope of activity and diversified the profit sources of Japanese companies across a broad array of sectors.

Japanese equities mixed in January on trade uncertainty, stronger yen

The Japanese equity market was mixed in January, with the TOPIX (w/dividends) rising 0.14% on-month and the Nikkei 225 (w/dividends) falling 0.80%. Stocks were weighed down by uncertainty surrounding the protectionist policies of the new US administration as well as the appreciation of the yen against the US dollar amid the outlook for the BOJ to continue hiking rates based on remarks made by Governor Ueda. On the other hand, positive factors included the International Monetary Fund raising its 2025 global economic growth forecast in light of the strength of the US economy. Japanese equities were also supported by the gains from semiconductor-related and other high-tech stocks after the US president announced a large-scale investment plan to boost the country's AI development.

Of the 33 Tokyo Stock Exchange sectors, 17 sectors rose, including Securities & Commodity Futures, Other Products, and Banks, while 16 sectors declined, including Marine Transportation, Electric Power & Gas, and Wholesale Trade.

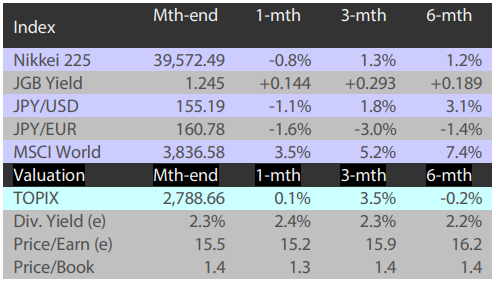

Exhibit 1: Major indices

Source: Bloomberg, 31 January 2025

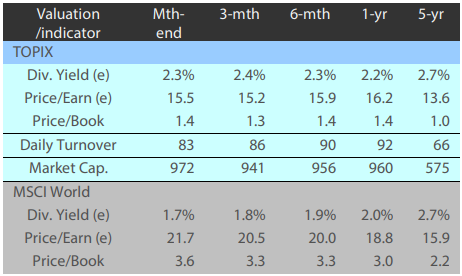

Exhibit 2: Valuation and indicators

Source: Bloomberg, 31 January 2025