From factory of the world to tech innovator

In 2015, economic reforms introduced under President Xi Jinping’s “Made in China” initiative jumpstarted China’s transition from “The Factory of the World” producing low-cost goods to a global leader in high-tech industries. China’s attempt to move up the value chain towards dominance in cutting-edge technology such as artificial intelligence (AI), electric vehicles (EVs) and humanoid robots did not go unnoticed by its rivals, particularly the US. Seeing the world’s second largest economy as a threat to Pax Americana, the US in 2022 imposed export controls that restricted China’s access to components and equipment vital to the development of advanced computing and chipmaking technology, and has been steadily tightening restrictions since then.

Homegrown champions step up to the plate

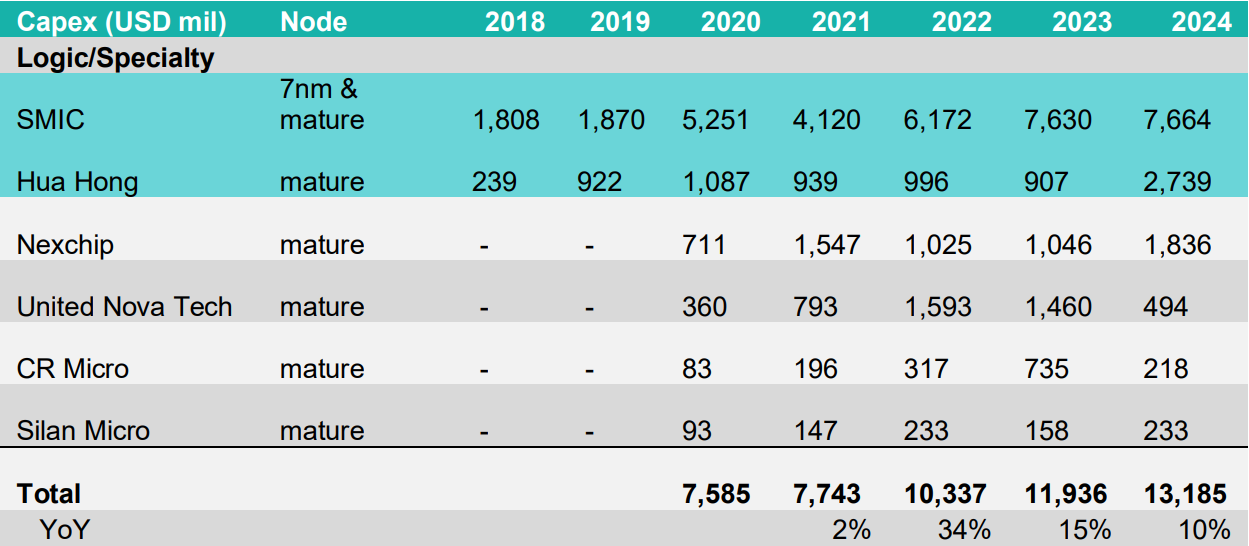

To counter those measures, Beijing accelerated the research and development of its semiconductor manufacturing capabilities, leveraging domestic champions including Semiconductor Manufacturing International Corporation (SMIC) to spearhead the endeavour. Our research indicates that Hong Kong-listed SMIC currently has the capacity to manufacture 25,000 wafers or semiconductor material monthly, with the potential to increase production to 43,000 per month once it consolidates all chipmaking equipment procured by Chinese firms over the past three years. Approximately 20 deep ultraviolet (DUV) lithography systems, which are not subject to US export controls, were imported to China, allowing the production of 7 nanometre (nm) chips.

To put things in perspective, industry leader Taiwan Semiconductor Manufacturing Company Limited’s (TSMC) 7 nm process used newer extreme ultraviolet (EUV) lithography systems to reportedly produce over 130,000 wafers monthly. The EUV systems give TSMC the capability to manufacture state-of-the art semiconductor material, the latest being the 2 nm process. After SMIC, Hua Hong Semiconductor is the second largest chip foundry in China. Following the US chip curbs, both companies are increasing their capital expenditure and manufacturing capacity to address the country’s AI and advanced computing requirements in other sectors such as EVs and humanoid robots.

Chart 1: China’s capex on semiconductor equipment

Source: Nikko AM (Company reports)

Local alternatives to AI chips and SoCs

While Huawei is also a key player in China’s push for self-sufficiency in producing advanced chips, particularly for AI, access to the privately-held firm’s business operations is limited. The media have reported that Huawei’s flagship Ascend 910C AI chip, produced with SMIC’s 7 nm process, boasts a yield rate of 40%, making it relatively profitable to manufacture at scale. This is a marked improvement compared with the previous Ascend 910B AI chip, which had a 20% yield. However, that still lags industry leader TSMC’s reported yield of over 90% for the 7 nm process.

Meanwhile, Cambricon Technologies has garnered attention as the Chinese authorities seek domestic AI chip alternatives to US-based Nvidia’s processors. However, chip shipments from the Shanghai-listed firm are currently limited, with manufacturing constraints at SMIC acting as a bottleneck. We believe this is due to a majority of wafer production capacity being reserved for Huawei.

Hong Kong-listed Xiaomi is also jumping on the advanced chip making bandwagon with its XRing 01 system on chip (SoC) in a bid to reduce dependence on US imports. Early Central Processing Unit (CPU) and Graphical Processing Unit (GPU) benchmark tests have shown Xiaomi’s mobile chipset performing nearly on par with the latest Snapdragon SoCs from Qualcomm. The smartphone maker aims to invest over US dollar (USD) 28 billion in research and development over the next five years to beef up its own mobile processors.

Don’t forget about memory modules

In addition to wafer fabrication, high bandwidth memory (HBM) modules are also essential for the production of the high-end chips required to handle the storage-intensive demands of current AI applications. We have observed that the US export curbs have limited China’s access to HBM2 chips. While the more widely available DDR5 memory modules can be used as substitutes, they do not have the same bandwidth and power efficiency as HBM2 chips. Chinese Dynamic random-access memory (DRAM) maker ChangXin Memory Technologies (CMXT) has emerged to bridge the shortfall. According to media reports, the privately-held memory chipmaker started mass production of HBM2 modules in August 2024, about two years ahead of schedule.

Chipmaking equipment replacement

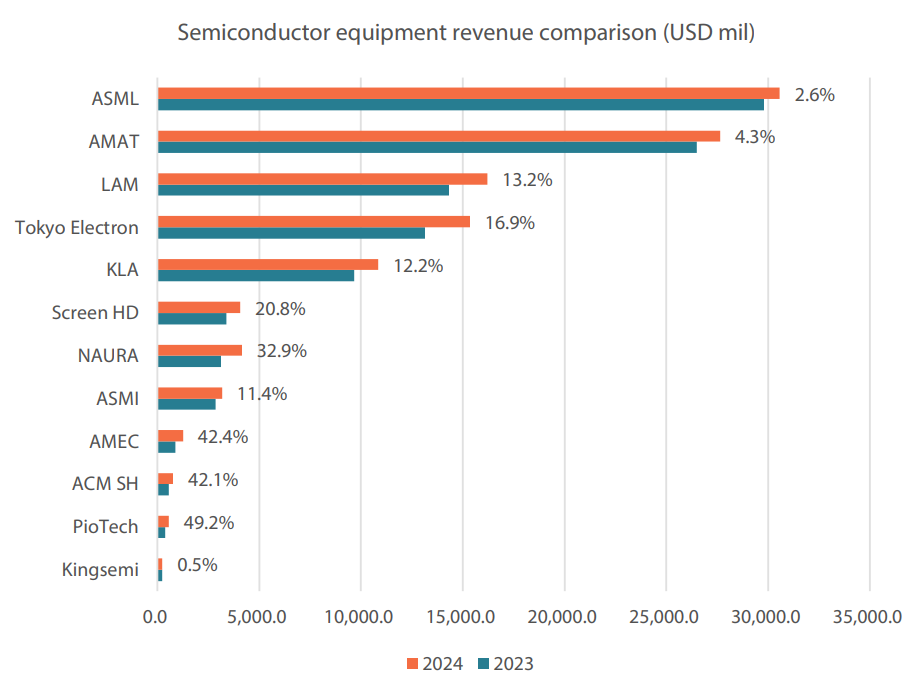

When it comes to the equipment needed to manufacture semiconductors, most of the top makers such as ASML, LAM Research and Applied Materials are prohibited from selling their latest technology to China due to the US export ban. We believe that Shanghai-listed Naura Technology, Advanced Micro-Fabrication Equipment Inc. China (AMEC) and privately-held Shanghai Micro Electronics Equipment Group (SMEE) are stepping in to plug the gap. Naura Technology and AMEC are established makers of specialised tools used in processes such as etching and chemical and vapour deposition. SMEE specialises in manufacturing lithography equipment. As the largest domestic semiconductor equipment maker, Naura Technology is also conducting research to develop lithography systems; in addition, it reportedly bought a stake in KingSemi to enhance its capabilities in this area.

Chart 2: Chinese semiconductor equipment makers are growing faster

Source: Nikko AM (Company reports)

Essential software

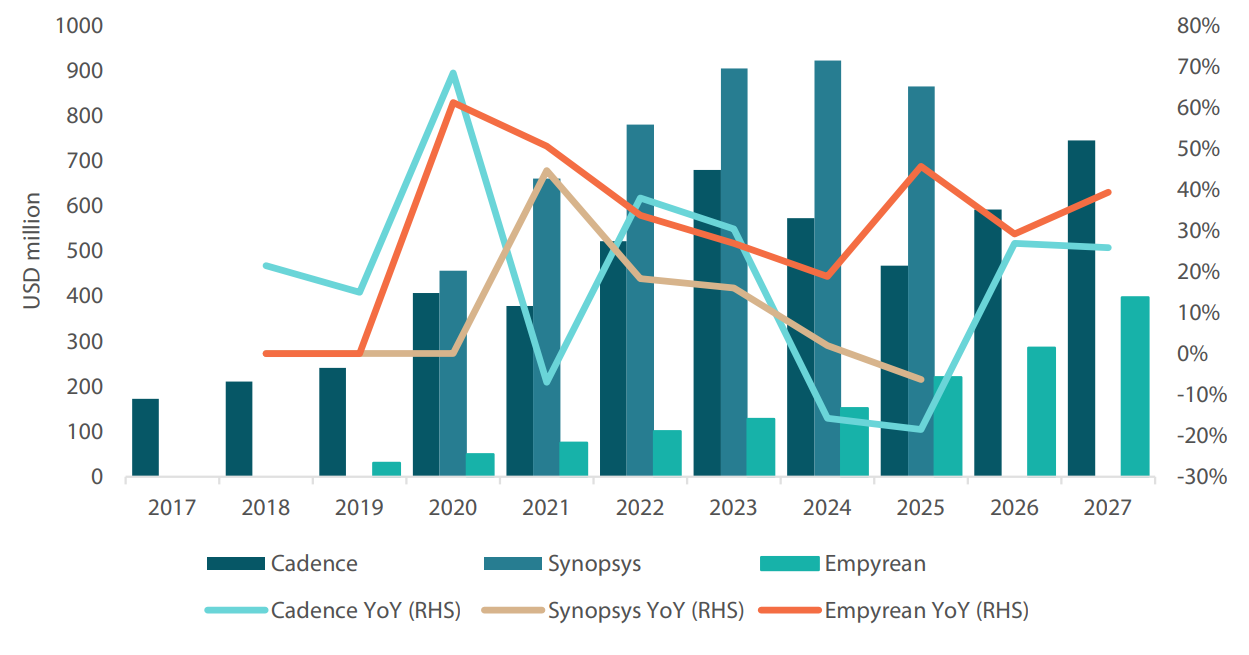

While hardware may seem like the most essential component of the industry, software also plays a major role, particularly in semiconductor design. Recently imposed US export controls on electronic design automation software (EDA) aim to limit China’s access to a vital tool in the chipmaking sector. This means that firms providing industrial design software, such as Cadence, Synopsys and Siemens EDA will need licences in order to continue supplying Chinese buyers. Empyrean Technology is emerging as a provider of homegrown software solutions for chipmakers to sidestep these measures.

Empyrean Technology, a Shenzhen-listed EDA firm controlled by the state-owned China Electronics Corporation, has shown strong growth over the past few years compared to the top players mentioned earlier, It is expected to continue growing strongly as part of the government’s drive for self-sufficiency. The firm announced plans to acquire Xpeedic Technology, another Chinese EDA company, to bolster its capabilities. We believe that the intensifying Sino-US trade tensions have accelerated China’s development timelines as it looks to fully build out its domestic semiconductor supply chain. Advanced computing and AI chips are an integral part of Beijing’s goal to redirect its economy away from low-value manufacturing. “China Plus One’ countries”, mainly in Asia, are proving to be lower-cost alternatives.

Chart 3: China EDA software revenues and growth

Source: Nikko AM (Company reports)

AI adoption and leading the (battery) pack

Chinese firms are making great strides in AI, a topic we explored in Did DeepSeek cause an AI paradigm shift? These AI applications are rapidly being integrated into the EV space, with automakers adapting AI to enhance autonomous driving systems. Hong Kong- and Shenzhen-listed BYD, the country’s largest EV automaker by market share, announced that it would integrate DeepSeek’s AI model into its latest assisted driving system for its vehicles sold locally. Moreover, Chinese firms are also industry leaders in EV batteries. Shenzhen-listed Contemporary Amperex Technology Co., Limited (CATL) and BYD took the top two spots in terms of global market share in 2024. These companies have been successful as they invested in lithium battery technology ahead of their peers, coupled with wide-ranging support from the authorities.

Ideal conditions for scaling emerging tech

AI is also making its presence felt in the field of humanoid robots, with Chinese firms such as Baidu, Huawei, Tencent, Xiaomi and BYD all making notable progress in this field. In our view, advancements in end-to-end AI computing, coupled with increased research and development funding, have widened the applications of humanoid robots in more industries including healthcare and manufacturing. This trend has sparked growing interest in humanoid robots.

We believe that Chinese firms will take the same approach for humanoid robots as they did with the fast adoption of EVs, autonomous driving and advanced industrial robots. Their approach could involve rapidly introducing a wide range of product models and potential use cases, with a vast array of diverse product models being whittled down through “natural selection”. Emerging technologies such as humanoid robotics require a period of trial and error, during which many initial users are willing to test new products. Fierce competition among multiple players also drives down unit costs quickly. The fact that the Chinese market meets these requirements is often overlooked by global investors.

With slowing growth and an ongoing trade war to handle, China appears to be in a crisis management mode. However, the Chinese characters for crisis, “危机”, representing both risk and opportunity, might be more appropriate in describing the state of the economy. The country is at an inflection point where major structural shifts are occurring as it strives to climb up the technological value chain to achieve self-sufficiency via innovation and resourcefulness. It is within these fundamental changes that we seek to identify quality names that can deliver sustainable returns in the China and Asia Ex-Japan landscape.

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way.