Key Takeaways

- With AI transforming the technology landscape, how do investors wade through the noise to identify genuine investment opportunities?

- We use our Future Quality framework to find the high-quality companies that are already moving the AI dial.

- Right now, we see those opportunities within the AI infrastructure-building space, where good companies intrinsic to the roll out of AI are already delivering high cash returns.

Change is one of few constants throughout history. The technology sector is a good example of how history never repeats, but it does rhyme. Looking back, there has been a clear evolution in computer platforms. Since the 1950s, new computing platforms that innovate and progress how humans interact with computers have emerged, dramatically expanding use cases. Bill Gates' vision of “a computer on every desk and in every home” was ridiculed at the time, yet now there is a computer in every pocket.

It started in the 1950s and 60s with the introduction of mainframe computers; in the 70s we had microcomputers (not so micro by today’s standard); while the 80s and 90s ushered the era of personal computers; and then this century we have lived through the ubiquity of smartphones. Each computing platform built on the shoulders of the previous generation and saw a 10x adoption increase. Now we appear to be on the precipice of another computing platform: artificial intelligence (AI).

Sifting through the AI noise

Since the launch of ChatGPT in November 2022, stock markets have been driven by the disruptive potential of this new computing platform. Like each previous computing platform, there is the promise to revolutionise many industries. As Future Quality investors, we look through the noise to focus on where the cashflows will accrue, on an enduring basis. Either by reinforcing existing business models to build higher moats or allow disruptors to unseat incumbents or create new markets.

Is there a bubble? History is full of cautionary tales. There are two key points of difference when analogies are drawn to the dot com bubble. Firstly, there are cornered resources in the technology and secondly the customers and funders of AI are the largest and most profitable companies. Neither of these factors were true for the internet bubble of the late 90’s. The development of the Internet era from the mid-1990s saw a significant infrastructure build-out that lasted for around 5-10 years.

One of the key enabling technologies for the internet was the shift of digital communication through copper to glass. The glass in our fibre optical fibre today is a marvel and key innovations were developed through the 1970s. These innovations included production of the purest glass, alongside optical amplifiers and wavelength division multiplexing that enabled vastly increased latency, volume and reliability of the data infrastructure. These crucial technologies were contributed to by a broad range of research institutions and private companies. So, companies were unable to establish a technological edge as the technologies were open and accessible to all. In fact, homogeneity was important to ensure a common network and adherence to industry standards was enforced by new regulations such as the Telecommunications Act of 1996 in the US, which ensured there was little to differentiate the infrastructure. With the benefit of hindsight, we know few profits accrued to those infrastructure builders. In fact, it was the applications that were built on top of the commoditised infrastructure that emerged to take advantage of the internet era.

Today, the AI ecosystem is very different to that of the internet era. Technological innovation is driving adoption and the regulatory environment is not as prescriptive or involved. Companies such as Nvidia are highly differentiated with incredible technological and strategic barriers built over many years. The vertical integration cutting across software, networking and GPUs has created incredible sticking points for customers by creating incredibly compelling solutions for customers, which few competitors can match.

Secondly, during the internet build out, as there were no technological barriers, companies viewed scale as the primary competitive vector. Whoever had the biggest network would win, was the thinking. In order to reach scale, huge sums of capital were required, and debt investors were more than happy to oblige. It is estimated over US dollar (USD) 500 billion was invested into internet infrastructure in the 5 years following the Telecommunications Act of 1996. This was just in the US and translates to just shy of USD 1 trillion inflation adjusted. Debt investors were more than happy to oblige. Leverage is an amplifier. In the downturn it was risk that was amplified, and many bankruptcies ensued. Compared to today, we have a very different set of funders. The majority of spend with AI today comes from rational cash-rich, highly profitable companies which are already enjoying a return on their investment spend.

In our view, we are at that very initial infrastructure-building stage of AI platforms. So, for us, we are not trying to identify the next generation of dominant AI players of a future unproven use case, or new product category. Instead, we are focused on finding those businesses that will be intrinsic to the development of AI’s infrastructure where we can have higher confidence of the company’s earnings power from today. We review these companies through our Future Quality framework to find the high-quality companies that are enablers of AI that offer sustainable and growing cash returns on investment. Today, we are drawn to the key infrastructure providers.

Case study: Synopsys

Synopsys—a supplier of Electronic Design Automation (EDA) software tools to the semiconductor industry—is an example of a business that meets our Future Quality criteria. Its EDA tools are crucial to the design of semiconductors. The most advanced chips today such as GPUs used for AI workloads, contain over 100bn transistors. Without EDA tools like Synopsys’, these semiconductors would be impossible to design or manufacture. And it is this constant march of progress which continuously demands more complex semiconductor designs and therefore more sophisticated EDA software. So as AI semiconductors drive this next wave of complexity, Synopsis revenues will be a significant beneficiary of this AI demand tailwind.

Further, our research has found that not only the product offering, but Synopsys’s business itself is also changing by adopting AI. From the product side, their first AI tool was released in 2020, the Design Space Optimisation AI, which optimises surface layout. Area optimisation is a key consideration in chip design, when considering the billions of transistors and the immense challenge their placement and design presents. Currently, one in five customers have adopted this tool which has a 20% uplift to pricing for Synopsys. Synopsys has also begun utilising AI to improve the efficiency of its own operations, having already identified more than 20 use cases.

In short, we have found that this is a business franchise that looks set to fully embrace and benefit from the AI trend, its management is clearly innovative and forward-thinking, while its return profile looks set to remain robust and sustainable over the long term.

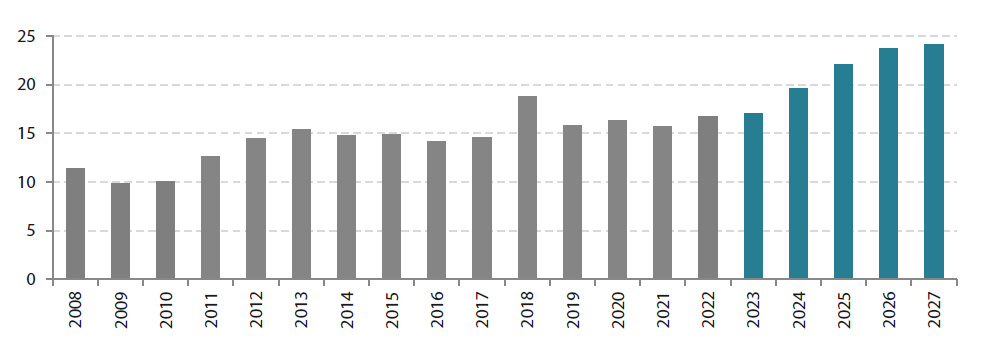

Chart 1: Synopsys current and projected cash return on investment

Source: Nikko AM, data as of 30 September 2023. Forecasts are not guaranteed.

Is technology becoming quasi-defensive?

But change within an industry doesn’t all have to be about disruptive trends; some changes relate to how investors view a particular sector or stocks within that sector. For obvious reasons, technology has traditionally always been considered a growth sector. Investors are generally happy to pay a premium for such stocks due to the potential for above-average earnings growth. Yet, the dynamics of some areas of the sector are changing.

Firstly, two of the leading technology giants—Meta and Alphabet—have recently announced their first-ever dividend payments. This is a significant milestone as technology companies have a history of hoarding their outsized profits to use for investment or acquisitions, with money usually only being returned to investors via share buybacks. Secondly, certain areas of the sector are experiencing more dependable earnings patterns, with earnings being less driven by cyclical economic drivers. For example, in order to compete with rapid digitisation and remain competitive, companies have little choice but to spend on software updates and invest in the latest technology developments. The roll-out of AI could be an additional spur here, with governments already investing heavily in AI applications in a modern-day equivalent of defence spending in the past. Rather than being growth attributes, stocks that provide regular dividends and consistent earnings regardless of the state of the underlying economy have traditionally been categorised as defensive by investors. So, while the technology sector can’t be entirely considered a defensive play just yet, certain areas are demonstrating more defensive qualities.

Envisioning tomorrow’s investment opportunities

Part of our Future Quality ethos is to look at the big picture and identify themes or structural shifts to determine which companies could benefit profitably over time. Our philosophy is adaptable and recognises that pathways can shift in response to new or altered inputs. This awareness and pragmatic approach to change has been particularly valuable in our response to the ongoing and rapid evolution of technology. With a disciplined process that is centred on seeing further and envisioning tomorrow’s investment opportunities, we strive to keep ahead of the pack with investments that will do well in both good times and bad.

For more information on our global equity investment process, please download Nikko AM’s new investment guide:

Seeing Further in Changing Times.

If you have any questions on this report, please contact:

Nikko AM team in Europe

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way.