Snapshot

Volatility dominated risk markets in the early part of the July-September quarter. In addition to movement driven by expectations over the likely timing of the first interest rate cut by the Federal Reserve (Fed) in the US, a rate hike in Japan caused the yen carry trade to unwind, thereby triggering a global risk asset sell-off led by Japanese equities. However, stock markets recovered towards the end of the quarter amidst more positive economic news flow. In addition, the Fed started the easing cycle with a larger-than-expected 50 basis points (bps) rate cut in September.

Perceptions of the US employment environment also impacted risk markets during the quarter. Following the announcement of soft employment data in the mid part of the quarter, global equities pulled back ahead of the release of US nonfarm payroll figures due to concerns over the health of the labour market. However, risk-on sentiment returned after the data showed that US employment conditions were better than expected. Towards the end of the quarter, the race between the two front runners to lead Japan’s ruling party (and thereby become Japan’s prime minister) drove volatility in Japanese equities and the yen, reflecting the two candidates’ opposing monetary policy views. However, the yen weakened after Shigeru Ishiba, who had previously been hawkish on monetary policy reversed his stance after he became the prime minister.

In our view, the current environment is favourable for equity markets. We feel that the Japanese market looks well placed to benefit from positives such as corporate governance improvements, while renewed optimism for a soft landing in the US and the Fed’s shift to monetary easing have pushed the S&P500 higher.

Cross-asset1

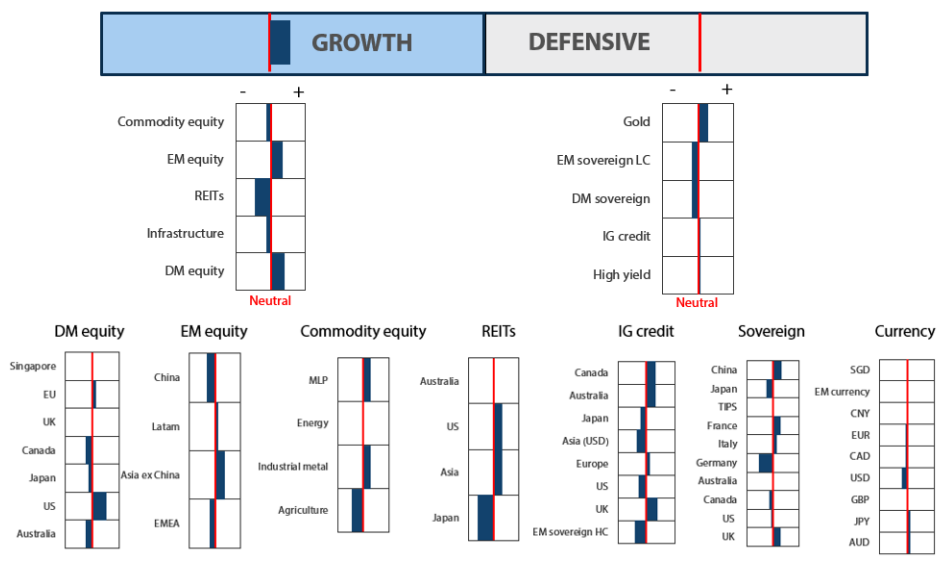

Over the July-September quarter, we kept an overweight position on growth assets and maintained a neutral position on defensive assets. Despite market volatility, several positive factors have supported growth assets, including the Fed’s interest rate cut, large fiscal spending globally and better-than-expected US economic growth. Through the quarter, we kept our overweight position in emerging market (EM) equities on a weaker US dollar, which would likely benefit EMs, and increasingly dovish monetary policies globally. The overweight position however had been reduced in August as part of our downside protection strategy. We continued to favour selective countries such as India and Indonesia, which are expected to benefit from domestically-driven economies and structural long-term growth stories. We also added weights to Taiwan, which is a beneficiary of the current global tech upcycle.

We increased our overweight position slightly in developed market (DM) equities on the back of resilient economic data and dovish monetary policies. We continue to like US for its positive earnings prospects and have added to our overweight position. During the quarter, we shifted from a slight overweight in Japan to an underweight in response to the yen’s volatility; however, we continue to favour Japan for its longer term structural story of improving corporate governance and earnings growth momentum. As such, we will look to slowly add capital on market corrections. Likewise, we reduced our overweight position in commodity equities to a slight underweight with sectors such as energy expected to face growing oversupply amid slowing demand. We instead shifted towards more defensive MLPs. We have also moved to a marginal underweight position in infrastructure as we see better risk rewards elsewhere.

Regarding defensives, we kept our high yield position unchanged at a slight overweight with the high all-in yields on offer making the asset class attractive. In addition, we increased our position in investment-grade (IG) credit to slightly above neutral with rate cuts expected to support the sector; we maintained our preference for Australia, Canada and the UK. We increased DM sovereigns to a smaller underweight.

Within DM sovereigns, we upgraded China as the currency hedging cost for the position dropped considerably. Furthermore, after being negative for a long period on US Treasuries, we upgraded our score to reflect the new reality that the Fed is entering its rate cutting cycle. Elsewhere, we upgraded gold to a larger overweight during the quarter as it typically performs strongly during rate cutting cycles and acts as a haven asset during periods of volatility. On the other hand, we reduced our exposure to EM local currency sovereigns due to currency volatility.

Asset Class Hierarchy (Team View2)

Research views

Growth assets: summary of score changes in Q3

While we maintained our overweight to growth assets throughout the quarter, score changes within the category over the period were somewhat large. EM equities were upgraded from underweight to overweight on the Fed pivot and a weaker US dollar, which should be positive for EMs. We continue to like specific countries such as India and Indonesia for their domestic demand-driven economies and long-term structural growth stories, as well as Taiwan as a beneficiary of the current global tech upcycle.

We also increased our overweight in DM equities in view of resilient economic data and increasingly dovish monetary policies globally, while rebalancing risk exposures within the category by adding to the US for a larger overweight (secular growth themes creating better visibility) and reducing Japan from overweight to underweight (more as a tactical move responding to the near-term headwinds coming from yen volatility; in the longer term we are still positive on the country’s structural story of improving corporate governance and earnings growth momentum).

On the other hand, we downgraded commodity-linked equities substantially from large overweight to slight underweight due to a worsening supply-demand balance in energy. Infrastructure was also reduced from overweight to underweight as we see better risk rewards in other asset classes. Within infrastructure, we prefer US utilities over UK infrastructure due to increasing energy demand from the secular growth in data centres in the US.

Growth assets as a whole are attractive given that economic data remains resilient against falling inflation, central banks are easing monetary policies globally and the likelihood of a hard landing continues to dissipate. Volatility could remain elevated amidst ongoing geopolitical risks, but liquidity is supportive given the USD 6.5 trillion in cash in money markets that could possibly flow into risk assets as interest rates continue to drop. The start of a rate-cutting cycle to normalise monetary policy is a powerful driver of returns—and this is a welcome departure from the impact of restrictive monetary policies implemented over the past few years. We view any current market corrections as attractive entry points from the perspective of a secular growth story.

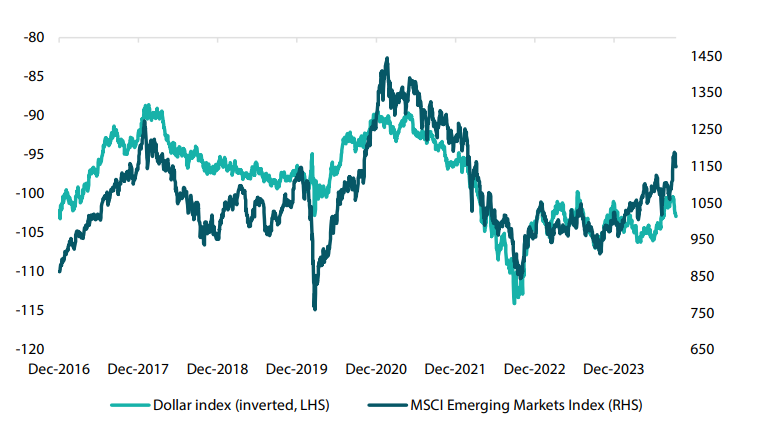

Growth assets topic: EM historically does well when the dollar weakens

With the start of the Fed’s easing cycle in September, the dollar is expected to weaken, which could provide a more supportive environment for EM. A weaker dollar is generally positive for global economic growth and emerging economies typically benefit from strong global growth. A weaker dollar also lowers the cost of borrowing, which is a further positive for EM companies. Historically, EM equities have performed well in periods of dollar weakness (Chart 1).

Chart 1: MSCI Emerging Markets Index benefits from a weaker dollar

Source: Bloomberg, October 2024

Likewise, EM central banks can now look to cut their own interest rates without having to defend their own currencies. Given the decrease in inflation and weaker economic data in these countries, the start of the rate cutting cycle is a welcome relief for reflating their economies.

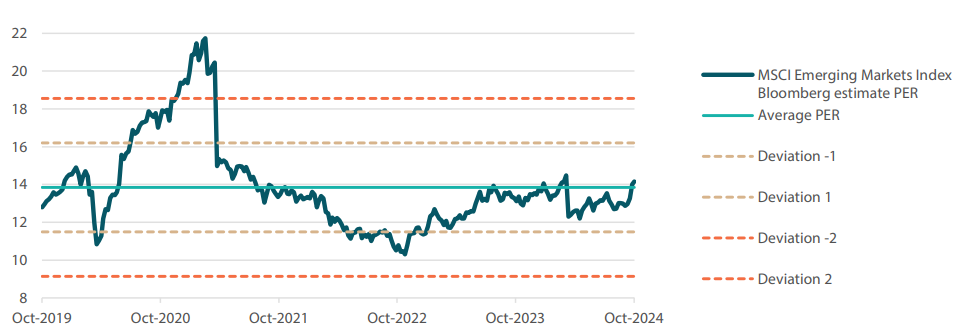

Despite the recent rally, EM valuation, in terms of PER, does not look stretched and is trading in line with its historical mean (Chart 2). Relatively, it looks attractive when compared to the rest of the world where valuations are currently at their upper band. Flows into the EM region have been increasingly positive recently and we expect them to continue on the back of further rate cuts from the Fed and a weakening dollar.

Chart 2: MSCI Emerging Markets Index valuation (PER) does not look stretched

Source: Bloomberg, ICI, October 2024

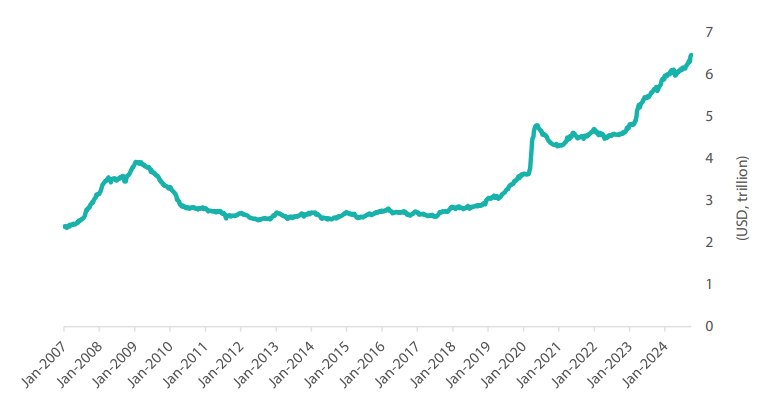

Furthermore, investors are ploughing billions into money market funds by the day (Chart 3). Since the start of the year, investors are estimated to have added another USD 557 billion to US money market funds. Retail investors currently hold close to USD 2.6 trillion of cash, with institutions making up the rest. Since 2022, the Fed embarked on the most aggressive pace of rate increases in decades which topped out at 5.5% in July 2023. The inverted yield curve also means short-end yields are yielding higher than the benchmark 10-year yield. The attractiveness of money market funds, T-bills and other short-term assets attracted the fastest pace of inflows since then.

Chart 3: Amount of liquidity in US money market funds a staggering USD 6.5 trillion

Source: Bloomberg, ICI, October 2024

With policymakers moving towards removing restrictive monetary policy and lowering interest rates, any moves away from money markets could potentially drive the valuation of risk assets higher. The timing and amount of these reductions is worth noting in the coming months.

Conviction views on growth assets

- Increased exposure to US secular growth: We continue to like US tech-related stocks despite market concerns regarding the returns expected on investments made on artificial intelligence and data centres. Corporate earnings have been resilient and the secular long-term growth story for the sector remains intact. Within the US, we are also starting to see the rally widening beyond the “Magnificent 7” which is positive for the overall market. As inflation comes under control amidst more dovish monetary policy, risk assets are expected to do well in the US.

- Maintained exposure to EMs: We maintained our overweight position in EMs based on relative valuation. With the start of the rate cut cycle in the US, a weaker dollar is typically positive for EMs. We like selective markets in India and Indonesia which benefit from domestically-driven economies and structural long-term growth stories. Likewise, we like Taiwan for its exposure to the global technology upcycle and as a beneficiary of a weaker dollar.

- Reduced Japanese equities: We moved to an underweight in Japan equities amid increasing yen volatility. We still like Japan’s structural reform story where we expect companies to increase their capital and dividend returns to shareholders. However, the volatility of the yen and a hawkish BOJ juxtaposed against dovish central banks globally also pose headwinds to sentiments. We will turn more positive on the country once we see the currency stabilising.

- Reduced commodity-linked equities and infrastructure, increased US utilities: Given the slowing economic data and energy oversupply, we have reduced our exposure in commodity-linked equities. We rebalanced the weights from MLPs (classified under commodity-linked equities) on profit taking into US utilities (classified under infrastructure) amid improving energy demand in the US from data centres. However, for infrastructure as a whole, we tactically maintained the underweight positions in the near term on better risk reward elsewhere. We remain confident that the asset class will continue to provide good diversification against inflation in the longer term as fundamentals remain compelling on both cyclical and secular factors.

Defensive assets: summary of score changes in Q3

Score changes within defensive assets were relatively small compared to those within growth assets. Having said that, one of the key changes over the quarter was the upgrading of gold to a larger overweight. The gold score, which was reduced slightly in July to allow the increase in credits, was raised substantially in September as we expect an environment in which central banks easing globally will be bullish for gold.

On the other hand, we downgraded EM sovereigns from overweight to underweight. Although we still view positively the real yields available and the macro fundamentals, the high levels of volatility in Latin American currencies due to political risks and the unwinding of yen carry trades warrant a cautious stance for the time being.

We remain underweight in DM sovereign bonds, as credit spreads are viewed more favourably and the highly inverted bond curves make it problematic to own long-dated exposures. As central banks ease, however, we look to favour a small overweight to duration, as bond curves typically steepen when the Fed cuts rates. This should bring renewed opportunities to look at sovereign bonds in the following months.

Finally, as economic growth remains buoyant in the US, and more dovish policy sets in, we still expect credit spreads to perform well. However, we are fast approaching levels where additional spread compression will be very hard to come by.

Defensive assets topic: the Fed returns

After beginning its interest rate hiking cycle in March 2022 and hiking over 500 bps, the Fed now deems that inflation is likely returning to more sustainable levels. This warranted a 50 bps rate cut in order to bring monetary policy out of restrictive territory.

While we were somewhat surprised by the Fed’s willingness to move 50 bps, clearly the inflation outlook is moving into a more normal environment whereby the Fed can reduce the cash rate towards 3.50% to bring the real rates in the economy closer to their long run average. Over the past 12 months we have been cautious on adding duration, however, more recently we have been favouring a move towards a neutral/small overweight position.

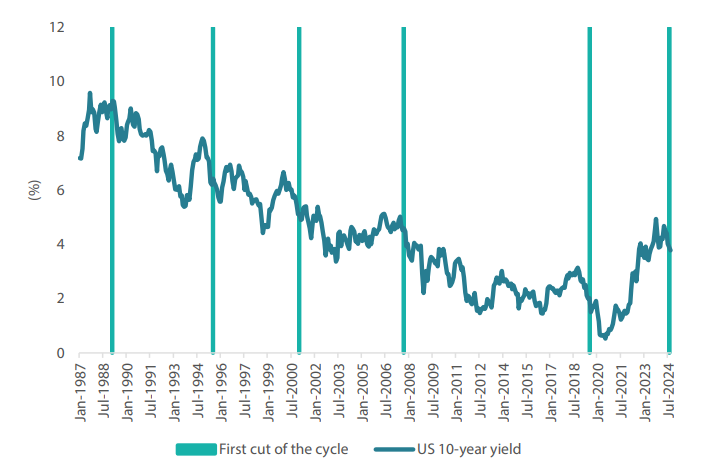

As Chart 4 below shows, once the Fed starts an easing cycle, the environment for bonds generally becomes more positive. As a simple rule while trying not to trivialise active duration decisions, we can state that when the Fed is tightening, be wary of bonds and when they are easing, re-allocate.

Chart 4: 10-year bonds and first cut of the cycle

Source: Bloomberg, October 2024

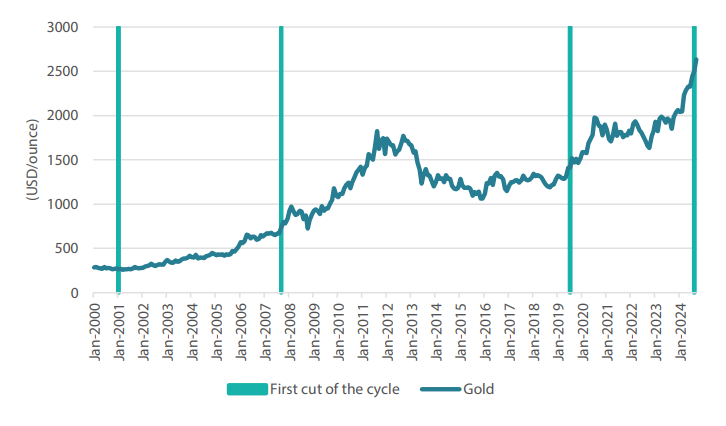

Additionally, when the Fed lowers rates, gold typically performs particularly well. While this is not true of all occasions over the past 50 years, it has been a very consistent rule to follow since the 2000s. Chart 5 below shows the performance of gold following the first cut of the cycle, with prices running 6%, 17%, and 39% over the following 12 months after the initial cut.

Over the past 12 months, gold has already posted an astonishing 43% gain in dollar terms, handily outperforming global equities. Increased central bank demand and opportunistic positioning by investors for the rate cuts mentioned above were the main factors that drove gold’s outperformance. We expect this to continue over the near term, as falling interest rates should be beneficial to the asset class; additionally, the large amounts of sovereign deficit funding is also viewed as a positive for gold.

Chart 5: Gold price and first cut of the cycle

Source: Bloomberg, September 2024

From a portfolio perspective, the dovish policy actions from the Fed are creating a number of opportunities for positioning. This is detailed not only in the EM equity positions driven by the weak dollar, but also more optimistic positioning for sovereign bonds and gold allocations. The drawback is that in Japanese yen terms, the bond market is still negative yielding, due to high hedging costs. However, as yield curves steepen, we see this becoming less of a problem over the next six months.

Conviction views on defensive assets

- Short-dated IG credit: Credit spreads remain at fair levels, but many markets still exhibit inverse yield curves, making longer-dated credit less appealing. As curves begin to steepen, we will look to shift this position. However, the current curve inversion still makes short-dated positions appealing.

- Gold remains an attractive hedge: Gold has been resilient in the face of rising real yields and a strong dollar, while proving to be an effective hedge against geopolitical risks and persistent inflation pressures. Falling real yields should benefit the asset class, and we use this allocation to supplement our long bond positioning.

- Adding duration: Central banks beginning to lower rates should be beneficial to bond markets globally. Picking the timing for rate cuts can be difficult; however, as restrictive policy comes to an end, this should be positive for bonds. Long-dated bond yields are still inverted, making large allocations expensive. However, as curves begin to steepen, continuing to add duration becomes an option.

Process

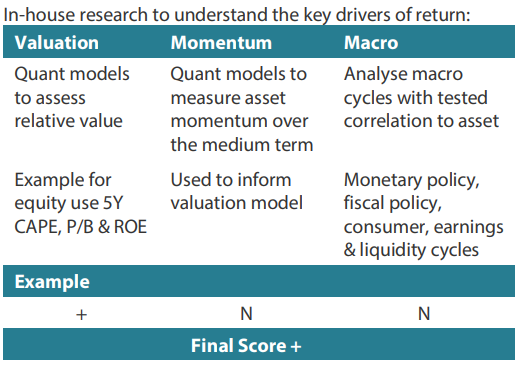

In-house research to understand the key drivers of return:

1 The Multi Asset team’s cross-asset views are expressed at three different levels: (1) growth versus defensive, (2) cross asset within growth and defensive assets, and (3) relative asset views within each asset class. These levels describe our research and intuition that asset classes behave similarly or disparately in predictable ways, such that cross-asset scoring makes sense and ultimately leads to more deliberate and robust portfolio construction.

2The asset classes or sectors mentioned herein are a reflection of the portfolio manager’s current view of the investment strategies taken on behalf of the portfolio managed. The research framework is divided into 3 levels of analysis. The scores presented reflect the team’s view of each asset relative to others in its asset class. Scores within each asset class will average to neutral, with the exception of Commodity. These comments should not be constituted as an investment research or recommendation advice. Any prediction, projection or forecast on sectors, the economy and/or the market trends is not necessarily indicative of their future state or likely performances.