A changing landscape

After years of widespread investor enthusiasm, ESG (Environmental, Social, and Governance) investing is now encountering growing negative sentiment. This scepticism stems from several factors: the overuse and politicisation of the ESG acronym, lack of understanding of sustainability, widespread greenwashing, short-term underperformance and concerns that it has become a marketing and greenwashing tool designed to simply attract capital. These issues are not entirely unfounded and recent scandals, like the one involving a large German asset manager, have only fuelled further scepticism.

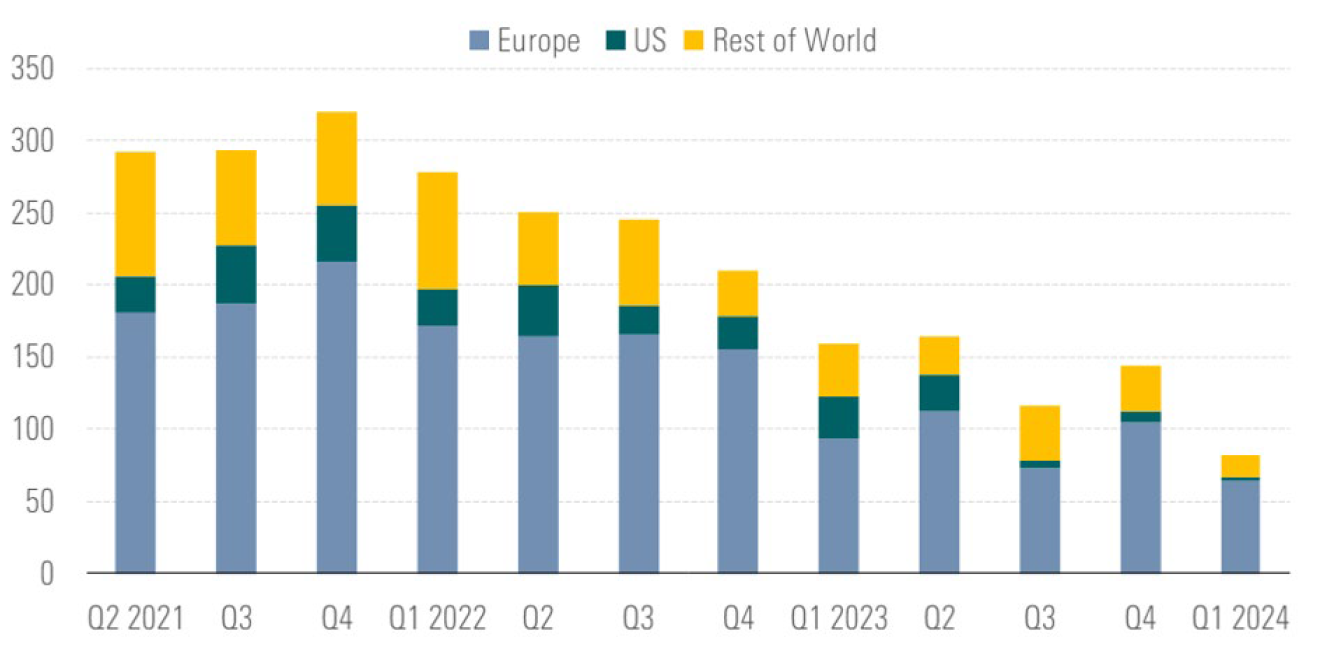

As the ESG label is becoming heavily scrutinised, we are observing an increase of funds removing references to ESG in their names and a steady drop in new launches of ESG or sustainability-named funds. Morningstar’s Global Sustainable Fund Flows Review1 shows that the first quarter of 2024 registered the lowest number of new sustainable fund launches in recent years. In fact, the trend has been declining steadily since 2021 and it’s now at its lowest point.

While this may look grim on the surface, we think the picture for sustainability-focused investors might be brighter than expected. The hype around ESG and the overuse of this term is in large part responsible for the growing backlash we have recently witnessed. This was expected and, in a way, can be seen almost as a positive development. Regulators have now been closely monitoring potential greenwashing risks and regulatory pressure keeps mounting—look no further than the upcoming European Securities and Markets Authority (ESMA) regulation on fund labelling for example. In the meantime, investors are developing a better understanding for the hidden nuances behind the various ESG or sustainability-related labels and claims used to promote funds. As a result, asset managers are now increasingly accountable and scrutinised for their claims and financial market participants are increasingly better educated on the topic—good news in our view.

Chart 1: Global sustainable fund launches per quarter

Source: Morningstar Direct Data as at March 2024

Looking further into ESG fund flows, we are seeing an increase in flows allocated towards ESG-labelled bond funds since the start of the year2. Like more conventional fixed income, high interest rates have led to increasing demand for sustainable debt. According to the Climate Bonds Initiative (CBI) quarterly market update, green bond issuance has reached record levels. A significant volume of US dollar (USD) 272.7 billion was added in the first quarter of 2024, which is 15% more than recorded in Q1 2023, and 41% more than Q4 20233. This data supports and aligns with S&P Global Ratings’ forecast that sustainable labelled bond issuance is on track to reach the USD 1 trillion milestone this year4.

Taking North America as an example, despite the worst-ever ESG outflows in the US in Q1 2024, the issuance of labelled bonds in North America saw a 68% increase year-on-year in Q1 2024. This surge is a clear indicator of the growing appetite to finance the green transition which we believe will maintain its momentum, regardless of election results in the US this year.

The appeal of green bonds

Green bonds have emerged as an increasingly attractive investment, offering a unique blend of financial returns and measurable environmental impact. These bonds are issued by entities that are generally committed to environmental sustainability, a commitment that is reflected not just in words but often in demonstrable actions. The funds raised through these bonds are specifically allocated for green projects, enhancing their credibility in the eyes of investors.

One of the standout features of green bonds is their transparency. The use of proceeds is clearly outlined, and issuers often provide regular updates on how the funds are being utilised. The money raised from these bonds is used to finance projects that promote environmental sustainability, including initiatives in renewable energy and pollution prevention. This level of transparency enhances the credibility of the sustainability claims of the bonds in the eyes of investors.

Further enhancing their appeal is the escalating support for green bonds from governments and regulatory bodies globally. Sovereigns, supranationals and agencies (SSAs) are increasingly endorsing sustainable initiatives, often providing incentives that amplify the attractiveness of green bonds. In fact, in the same CBI Q1 2024 report, lifetime volume of sovereign green, social, sustainable and other labelled (GSS+) bonds crossed the USD 0.5 trillion mark, reaching USD 538.3 billion, and sustainable finance passed a milestone of 50 sovereign issuers5.

We believe green bonds are made attractive as they address a lot of the concerns about mainstream ESG investments. Green bonds reduce risks of greenwashing through clear transparency and ringfenced allocation of proceeds towards sustainable projects. In many cases, investors can enjoy the benefits of positive environmental contributions without sacrificing yield. This makes green bonds a win-win for investors, offering the potential for attractive yields along with environmental benefits.

A rigorous review process to address greenwashing risks

While the transparency and impact of green bonds can help alleviate scepticism around ESG and sustainability claims, green bonds are not immune from greenwashing risks. A recent study published in the International Review of Financial Analysis highlights for example that companies can use the funds raised by issuing green bonds to misrepresent their investment in green activities6.

To address this concern, we believe it is imperative that managers implement a rigorous review process at both issuer- and use of proceeds-level. Our sustainable review process is a stringent two-step pre-investment procedure designed to ensure that we invest in green bonds making tangible environmental impact, issued by entities also committed to sustainability.

Assessing the bond’s structure and impact

The first step in our process involves a thorough examination of the bond’s structure and impact. We assess and measure how the proceeds from the bond are being used. This involves a detailed analysis of the projects that the bond is intended to fund. This includes thorough review of source data, as opposed to simply relying on third-party data, such as the issuer’s green bond framework and associated second-party opinion, as well as the issuer’s allocation and impact reports.

We look for evidence of tangible contribution to environmental objectives, by making sure proceeds are clearly allocated towards meaningful and impactful projects, such as solar or wind farms for a utility company, green and energy efficient buildings in the real estate sector, clean transportation solutions for a delivery company and so on.

We also do our best to assess the concrete impact of the projects financed. A common metric often reported by issuers is greenhouse gas (GHG) emissions avoided through use of proceeds. However, this may not be always appropriate. For example, impact can be a real challenge to measure, and even more so to compare, when it comes to projects relating to biodiversity and nature preservation. These are important limitations to acknowledge when it comes to the impact of green bonds, making an active bottom-up assessment a critical element of our research process.

Evaluating the issuer’s sustainability strategy

The second and equally important step in our process involves an evaluation of the issuer’s overall sustainability credentials. We believe the issuer’s broader strategy needs to be consistent with the purpose and issuance of the green bond.

We assess the issuer’s commitment to sustainability, looking at factors such as their corporate governance practices, their environmental policies, and their track record on sustainability issues. We also consider the issuer’s sustainability targets and how the green bond fits into these plans. Using the utility sector as an example, having proceeds earmarked towards renewable energy projects is not sufficient, we also expect ambitious climate commitments, such as the full phase-out of coal production, measurable short- and medium-term targets to reduce GHG emissions and tangible evidence of shift towards renewable energy in the energy mix.

The green bond market is in constant evolution and we do not expect the momentum behind green bond issuances to subside anytime soon. The need to finance the transition will continue rising. The introduction of European Green Bond standards will raise the bar further when it comes to transparency and credibility of use of proceeds. We expect growth in issuance to also be supported by a diversification of the types of projects financed as global reporting standards are introduced. The recent introduction of the framework for nature-related financial disclosures by the TNFD (Task Force on Nature Related Financial Disclosures) is expected to support the continued growth of biodiversity-related bonds, for example.

In a world where the need for sustainable investing is becoming increasingly apparent, green bonds offer an appealing option. Due to their design, they inherently help address important risks around greenwashing. When complemented with an active bottom-up review process, we believe green bonds can offer tangible and credible environmental impact combined with attractive returns.

Nikko AM team in Europe

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.

1https://www.morningstar.com/lp/global-esg-flows

2 Barclays: ESG fund flow update: May 2024.

3 https://www.climatebonds.net/files/reports/cbi_mr_q1_2024_01e_1.pdf

4 https://www.spglobal.com/_assets/documents/ratings/research/101593071.pdf

5 https://www.climatebonds.net/files/reports/cbi_mr_q1_2024_01e_1.pdf

6 https://www.sciencedirect.com/science/article/abs/pii/S1057521923003666