Both interest rate decisions by the Federal Reserve (Fed) on 18 December and Bank of Japan (BOJ) the day after were in line with market expectations. The Fed cut the Federal Funds rate by 25 basis points (bps) to a target range of 4.25-4.5% and the BOJ held the uncollateralized overnight call rate at 0.25%. The messaging around these seemingly predictable decisions was the main focus in both cases. The Fed's December Summary of Economic Projections showed a considerable upgrade in the Federal Open Market Committee (FOMC)'s outlook for growth and inflation and, consequently, in projections for the Fed Funds rate over the near term (a change to two 25bp rate cuts in 2025 in place of four). Perhaps more meaningfully, FOMC projections for longer-run interest rates also inched upward. The signalling sent stocks plunging in the US and pressured Japanese equity markets the next day.

The dollar also reacted to the change in the Fed Funds rate projection and surged broadly following the FOMC meeting. Although the BOJ was reluctant to acknowledge that its decision to keep rates on hold was influenced by the market reaction to the Fed's statement, the market interpreted the decision, alongside a statement by BOJ Governor Kazuo Ueda, to mean that the central bank was in no hurry to implement further hikes. This interpretation pushed dollar/yen above its prior post-US election highs.

BOJ and FOMC signal uncertainty as a hurdle to clear policy trajectories

Dollar/yen may have surged, but the US-Japan interest rate differential did modestly narrow after the Fed's rate cut. Despite seemingly divergent policy signals, there were similarities in parts of the messages delivered by Fed Chair Powell and BOJ Governor Ueda. Unfortunately, both Powell and Ueda focused on a topic that is unattractive to financial markets—uncertainties surrounding their respective policy outlooks. One prominent topic at both post-monetary decision press conferences was US trade policy, and by extension, fiscal policy in 2025. Strictly speaking, US trade and fiscal policy will remain unknown at least until president-elect Donald Trump is sworn in. However, recent headlines have made clear that tariffs will feature significantly in the incoming administration's policies. This is expected to lead to inflationary effects within the US. Additionally, the US imposing tariffs could negatively affect the growth trajectory of Washington's trade partners. Depending on the degree of retaliation, which is uncertain at this stage as both Powell and Ueda mentioned, retaliatory tariffs by trade partners could have negative repercussions for the US as well.

Fed raises growth and inflation forecast, hints of fiscal uncertainty

Despite the aforementioned uncertainties, the FOMC's summary of economic projections offered clear upgrades to the near-term US growth and inflation outlooks. The FOMC's median 2024 growth projections were revised upward by 0.5%, to 2.5% from September's projections. Projections for 2025 were upgraded more modestly to 2.1% from 2%. However, the projection for 2027 was downgraded from 2% to 1.9%. That said, the range of forecasts for 2027 widened from those of September, possibly hinting at greater uncertainty over the longer-term ramifications of US fiscal and trade policy. Meanwhile, although unemployment was revised modestly downward from September's figures for 2024 and 2025, median projections remained above the estimated longer-run rate of 4.2%, at 4.3% through 2027.

Both headline and core PCE inflation projections for end-2025 were raised significantly, to 2.5% from 2.1% and 2.2%, respectively, from September's figures. Fed Funds rate expectations for end-2025 were consequently revised to 3.9% from 3.4%; for end-2026, they were revised to 3.4% from 2.9%. It should be noted that although the median longer-run rate was only increased by 0.1% to 3%, there was a significant upgrade in the lower end of the central tendency range for the Fed Funds rate to 2.8%-3.6% from 2.5%-3.5% in September. As such, it may be said that there was an effective upgrade to the FOMC's estimates of the “terminal rate”. Moreover, one dissenter—Cleveland Fed President Beth Hammack—favoured remaining on hold rather than meeting market expectations for a 25-bp cut. These combined factors may have triggered the stock market's decline and the dollar's surge.

BOJ wants more information on wage momentum, US policy and Japan budget

On its own, the BOJ's statement cannot be classified as conclusively dovish. One reason for this is that the BOJ decision to remain on hold at 0.25% was not unanimous. BOJ Board Member Naoki Tamura judged that economic activity and prices were indeed developing in line with the BOJ's outlook. Furthermore, he believed that risks to prices had become skewed to the upside, leading him to favour a 25 bp hike to 0.5%.

On this occasion, the majority of BOJ Board members did not agree. BOJ Governor Ueda mentioned the need for further “momentum” on wages and favoured waiting for additional information about the “Shunto” spring wage round negotiations, which are due to be released in the first quarter. This, however, was not the only factor. During the post-meeting press conference, Ueda had to respond to numerous questions regarding US tariffs. Much like Powell, Ueda emphasised the uncertainty of the situation given the absence of clear data on concrete US trade measures and potential retaliation from trade partners.

Meanwhile, market speculation was less preoccupied with BOJ rhetoric than with the ongoing negotiations between Japanese Prime Minister Shigeru Ishiba's minority government and opposition parties over the coming year's annual budget. This remains a source of fiscal uncertainty for Japan and provides one plausible reason for the BOJ to remain cautious. Positively, there are few signals that inflation is accelerating to an extent requiring immediate action, which may have also influenced the BOJ's decision to stay on hold amid ongoing policy uncertainty at home and abroad.

Dollar/yen impact on “virtuous circle” remains a wild card

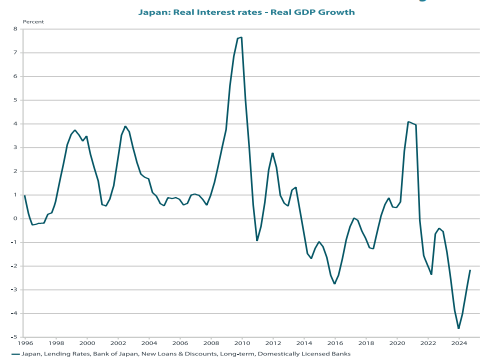

Uncertain near-term “momentum” on wages aside, Japanese data remain supportive of robust above-potential growth, therefore suggesting that the BOJ will continue withdrawing stimulus in 2025. Monetary policy remains unambiguously accommodative, thereby indicating that the BOJ has not yet hit “neutral”. Although the differential between real interest rates and real growth has rebounded since the BOJ commenced its rate hike cycle, it remains in clearly negative territory (Chart 1).

Chart 1: Differential between real interest rates and real growth remains accommodative

Source: Nikko AM, BOJ, CAO

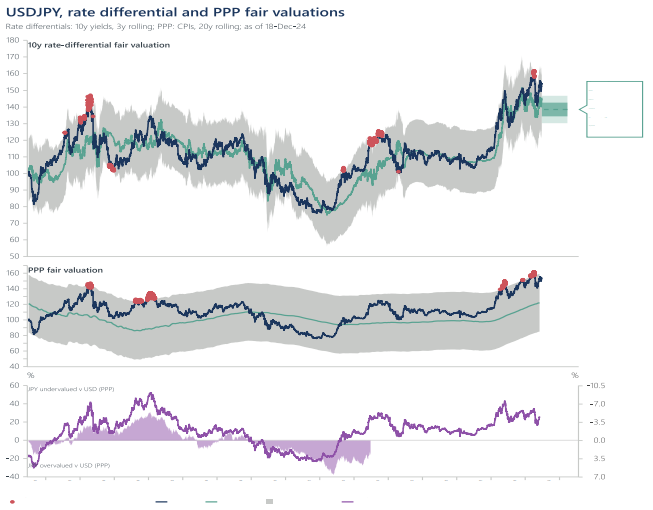

However, as dollar/yen heads higher, the central bank will also remain aware of the potential for higher imported inflation to be passed through to households, eroding the gains in real wages on which the “virtuous circle” of reflation is so dependent. We discussed the heightened lagged impact of dollar-priced import prices on core CPI in our insight “The yen: how weak is too weak?”,“ which we believe is still relevant. We highlight that by both longer-term (purchasing power parity) and short-term (relative interest rate differentials) measures, the yen remains under-valued. A continuing weakening of the yen from the current already weak levels may spur the BOJ into action, much as it may have influenced its last rate hike in July, when dollar/yen broke briefly above the 160 mark. Meanwhile, we see a high likelihood that the BOJ will hike rates even prior to the culmination of “Shunto” talks in March 2025.

Chart 2: the yen is undervalued against the dollar by several measures

Source: Macrobond, US Treasury, BLS, SBJ