Snapshot

The US Treasury (UST) market has been an important barometer of the reflation trade for markets this year. Most asset classes have performed in line with movements in UST yields as correlations, whether positive or negative, remain strong. After topping out at 1.74% to end the first quarter, 10-year UST yields have retraced this month, finally taking a breather after aggressively selling off from the beginning of the year. The knock-on effect was a weaker US dollar and growth equities clawing back some of their underperformance relative to value equities. Strong reported earnings for large US technology companies were also supportive of this rotation.

We consider this recent fall in yields to be more of a pause though, with yields likely to grind higher again as growth continues to improve and inflation pressures mount. A gradual rise in yields will support more favourable conditions for risk assets than the more aggressive adjustment witnessed in the first quarter. This gradual normalisation will once again favour value over growth as value stocks benefit from the re-opening that gathers pace in the rest of the world. Higher yields will also provide some support for the US dollar but stronger growth returning to the rest of the world should temper any major bout of US dollar strength that could otherwise damage the recovery story.

One challenge that awaits is navigating the often-conflicting views of central banks and economists on the true nature of inflationary pressures in the post-pandemic recovery. Annual rates of inflation are rising fast as prices rebound from severe interruptions in activity in many sectors of the economy. This bounce back effect seems to suggest price pressures will be transitory although structural changes in supply chains and global trade may suggest otherwise. We are keeping an open mind although we see the potential for elevated uncertainty as investors attempt to determine if such inflation is indeed transitory.

Our chief concern in the months ahead however is markets embracing a “taper tantrum” environment where we return to pricing a more aggressive adjustment in yields. Central bank official cash rates are still very low against a backdrop of a world returning to healthy economic growth while inflation expectations have been slowly rising. However, these expectations appear to be well-anchored as investors contemplate a return to more normal inflation conditions. While there is certainly a transitory nature to some of the inflation pressures beginning to appear, getting a more accurate read on the potential stickiness of price rises will have to wait until the volatile economic readings of 2020 begin to stabilise later this year.

Cross-asset1

We maintained our positive view on growth assets and negative view on defensive assets. Fixed income markets turned in a better month after markets had re-priced aggressively to steeper yield curves since the beginning of the year. Somehow a pause seemed warranted after central banks were unwavering in their stance of keeping policy accommodative for some time. However, with rapidly improving global growth ahead, we still see only one direction for rates which is eventually up.

As expected, US economic growth has been quite strong due to both monetary and fiscal stimulus coupled with the fast progression of the vaccine rollout. However, as vaccinations slow in the US and ramp up in other parts of the world, starting with Europe, a rotation to growth outside of the US will accelerate. The risk to this outlook is a further sell-off in the US yield curve that could return the dollar to strength and hold back growth in the rest of the world.

We marginally adjusted our relative asset class views, lifting developed market equities and lowering emerging markets (EM), given the headwinds to EM from a slow vaccine rollout. Nevertheless, we still maintain a slight preference for EM as we believe EM will benefit from stronger global growth. We marginally lifted our view on infrastructure as well with the inclusion of master limited partnership (MLPs) exposure to mid-stream energy infrastructure as an undervalued addition that benefits from increased economic activity and higher oil prices. We also marginally upgraded our view on growth currencies at the expense of defensive currencies on the view that less protection is needed against US dollar strength returning, though we are cautious if the long-end of the yield curve resumes its sell-off as quickly as it did in March.

1The Multi Asset team’s cross-asset views are expressed at three different levels: (1) growth versus defensive, (2) cross asset within growth and defensive assets, and (3) relative asset views within each asset class. These levels describe our research and intuition that asset classes behave similarly or disparately in predictable ways, such that cross-asset scoring makes sense and ultimately leads to more deliberate and robust portfolio construction.

1Asset Class Hierarchy (Team View1)")

1The asset classes or sectors mentioned herein are a reflection of the portfolio manager’s current view of the investment strategies taken on behalf of the portfolio managed. The research framework is divided into 3 levels of analysis. The scores presented reflect the team’s view of each asset relative to others in its asset class. Scores within each asset class will average to neutral, with the exception of Commodity. These comments should not be constituted as an investment research or recommendation advice. Any prediction, projection or forecast on sectors, the economy and/or the market trends is not necessarily indicative of their future state or likely performances.

Research views

Growth assets

After the worst of the COVID-19 market crash in March 2020, markets largely ignored profoundly negative economic data that followed, on hopes that large synchronised stimulus and ultimately the vaccine rollout would bring back global demand. The hopes proved warranted, but markets have been a tad more skittish of late on the concern that strong inflation data may be more than just “transitory” as the US Federal Reserve (Fed) still insists.

Based on the strong economic recovery that will continue to accelerate, the outlook for growth assets remains quite positive. However, different than the “Goldilocks” scenario where growth remains strong, but not too strong to precipitate tightening, markets are likely going to continue to question the Fed’s resolve to keep policy easy until inflationary pressures visibly retreat as predicted.

Even if the Fed does taper later this year while setting a course for rate hikes in 2022, policy will still be a long way from tight to the extent that growth would be impeded. In such an environment, growth is the safer asset than fixed income “defensives” where highly compressed yields will inevitably expand. Nevertheless, elevated uncertainty surrounding the transitory nature of inflation and the Fed’s resolve to keep policy easy will keep markets on edge and volatility elevated.

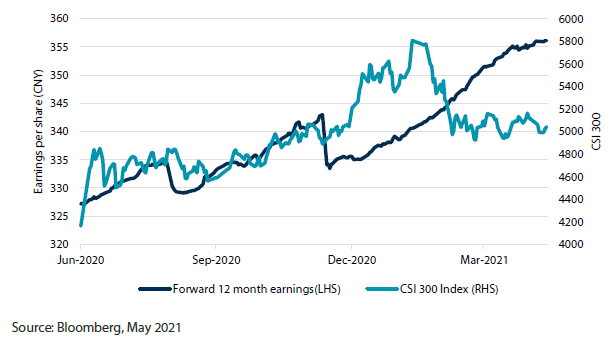

China equities looking cheaper while headwinds remain

We have been somewhat negative on China, partly for the tightening headwinds, but more for the regulatory risk hitting the tech sector. This has been exacerbated by the rotation from growth to value, while China as a whole is tech-heavy. We still think these are viable headwinds but ultimately price is guided by earnings prospects and, so far, consensus earnings forecasts are still quite sanguine relative to the much gloomier price action over the last two months. If analysts are correct in the forecasts, China equities are starting to look relatively cheap.

Chart 1: China forward earnings still robust, despite market sell-off

Markets are often correct in their forward-looking assessments, but not always. Because the China market has been historically driven by liquidity that determines retail sentiment, the knee jerk reaction is to sell on any indication that the government is tightening policy. However, China’s current focus on quality growth (avoiding bubbles and busts) means that growth momentum can continue despite targeted tightening at the margin.

However, China does use strong growth to push its reform agenda and, currently, authorities are taking aim at monopolistic portions of the tech market such as fintech. In the long run, this is probably a good thing but in the near term, uncertainty remains high and the consensus forecasts may not be adequately discounting these risks.

We have liked secular growth including tech in the US, China and North Asia, but we are cautious about the speed of the rotation from growth to value as inflation pressures are building on a global scale. Currently, markets are fixated on the transitory nature of inflationary pressures because if it proves stickier, the concern is that central banks will have to move more quickly in which case the rotation from growth to value would likely accelerate.

Conviction views on growth assets

- Reduced conviction view on EM: We reduced our conviction view on EM, once again—both equities and fixed income. While the dollar has returned to weakness, which is positive for EM, the path for the dollar remains uncertain given the unsteadiness of long-term rates. EM is also benefiting from strong commodity prices and improving global demand. However, it is becoming increasingly apparent that EM is far from exiting the COVID-19 crisis between the slow speed of the vaccine rollout and now new variants that are hitting places such as India very badly.

- Lifting Infrastructure and DM equities: Against the decrease to EM, we lifted Infrastructure by one notch to just under neutral as a relatively more defensive growth asset. We also became more positive on DM equities that stand to benefit from an accelerating vaccine rollout.

- Less conviction on relative performance within DM equities: We reduced our positive view on Japan equities given the COVID-19-related headwinds of a slow vaccine rollout and new outbreaks. We also became less positive on Singapore owing to new lockdowns connected with the India variant. We lifted the US back to neutral and reduced our negative view on Australia, overall compressing the dispersion of scores for having less conviction on relative performance within the asset class.

Defensive assets

here was no change to our negative view on defensive assets this month. Global bond yields have found support over the last few months, failing to reach new highs, but significant challenges lie ahead. The Fed continues to describe rising inflation pressures as linked to the reopening of its economy and likely to be transitory. However, this may prove to be wishful thinking as the global recovery gathers steam and businesses regain pricing power. Vaccinations are proceeding rapidly across the US and UK but have lagged elsewhere. In the meantime, fiscal and monetary support continues to fill in for any demand gaps. This combination of improving growth outlooks and growing inflation pressures will keep upward pressure on bond yields.

Credit spreads are now historically tight, reflecting market expectations for a strong global economic recovery coming out of the worst of the pandemic. Corporate credit quality should rapidly improve in this environment, but such optimism is also likely to push benchmark government yields higher. This will result in only modest corporate bond returns, although the higher running yield still makes them preferable to sovereign bonds.

We have also maintained our favourable view on inflation assets within the defensive sectors. Central banks continue to frame the approaching lift in inflation as transitory but highly accommodative monetary and fiscal policies may lead to a longer lasting inflationary environment. This shift will continue to support inflation-protected assets.

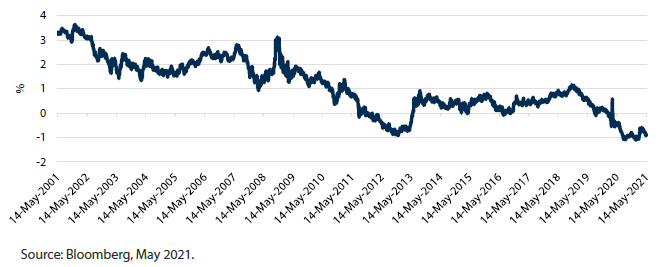

Only the Fed could love negative real yields

The US inflation debate has begun in earnest with Fed officials on one side and concerned bond investors on the other. The recent data on inflation has been unequivocally strong although it is also true that the annual figures have been flattered by base effects. The Fed cites this factor as well as others to argue that the price pressures of today, and the near future, will prove to be transitory. While many bond investors will appreciate the Fed’s efforts to calm the market’s inflation nerves, we believe there is a more fundamental issue facing potential buyers of USTs.

If we assume that the general goal of investors is to generate a return that exceeds the rate of inflation over time, then the current real yield of USTs presents a problem. Namely, it’s deeply negative. Chart 2 shows the US 10-year real yield over the last 20 years. The two periods where this rate goes negative are when the Fed is pulling out all stops to stimulate the economy and conducting large-scale asset purchases. This stands to reason as the Fed’s motivation for buying bonds is a function of monetary policy and not the expected investment return offered by their purchases. In other words, the Fed is largely agnostic about the rate of return offered by US Treasuries.

Chart 2: US 10-year TIPS real yield

Investors, on the other hand, don’t have the same luxury to accept negative real returns. When we look ahead to the Fed eventually reducing its quantitative easing programme in the face of much larger federal debt, we wonder how receptive investors will be to taking up the slack left by the Fed. At current negative real yields, we suspect it will be a bitter pill to swallow unless there is an adjustment towards more palatable levels. At a minimum, the benchmark 10-year real yield will need to be slightly positive, in our view.

If we assume that any inflation problems are manageable and the Fed gets its inflation average of 2%, then 10-year UST yields would need to rise to at least 2% to make them generate a non-negative real return for investors. Barring this, we find it difficult to see investors lining up to fund the US deficit at a negative real return. Of course, real yields could adjust through the rate of inflation falling faster than nominal bond yields, but the current climate suggests that the risks lie in the other direction.

Conviction views on defensive assets

- China government bonds are preferred safe haven: China’s government bonds offer much higher yields and lower volatility than traditional developed market sovereign bonds.

- Caution on US Treasuries: Rising inflation pressures and negative real yields are troublesome for USTs as the Fed will eventually reduce its bond buying.

Process