Summary

- Asian stocks brushed aside uncertainties posed by new COVID-19 variants and climbed higher in January. The MSCI AC Asia ex Japan Index rose 4.1% in US dollar (USD) terms over the month.

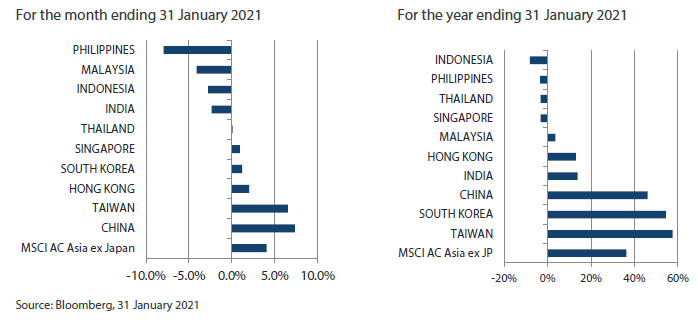

- China and Taiwan were the best performers in January. China was buoyed by better-than-expected fourth quarter GDP growth, while Taiwan was aided by the strong performance of index heavyweight Taiwan Semiconductor Manufacturing Company.

- Conversely, the ASEAN region lagged. In the Philippines, extended travel curbs and weak export data raised concerns about the country's fragile economic recovery. Meanwhile, the Malaysian government re-imposed the Movement Control Order in several states and subsequently declared a state of emergency to rein in rising COVID-19 infections.

- Most Asian countries have plenty of fiscal and/or monetary stimulus headroom, and their superior growth and better national finances are available at a significant discount to developed markets. A languid USD should enhance local currency returns in Asian markets.

Market review

Regional stocks climb higher in January

While developed-market equities experienced a downturn in January, Asian stocks brushed aside uncertainties posed by new COVID-19 variants and climbed higher. Regional equities were supported by China’s better-than-expected fourth quarter (4Q20) economic growth and the continued optimism about a vaccine-led regional economic recovery as more Asian countries began rolling out mass COVID-19 vaccination programmes.

For the month, the MSCI AC Asia ex Japan Index rose 4.1% in US dollar (USD) terms, outperforming the MSCI AC World Index, which fell 1.0%. Within the region, China, Taiwan and Hong Kong were the best performers in USD terms (as measured by the MSCI indices), while the Philippines, Malaysia and Indonesia were the worst performers.

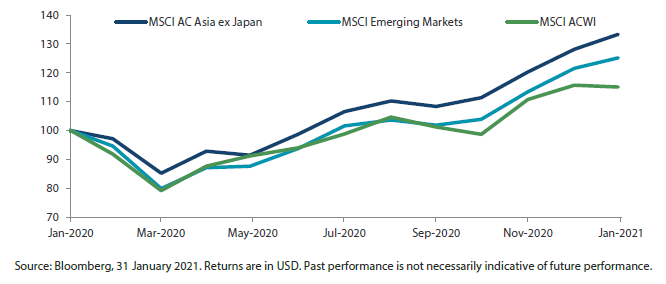

Chart 1: 1-year market performance of MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index

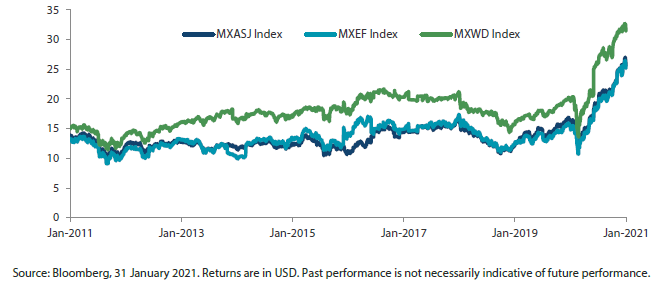

Chart 2: MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index price-to-earnings

China and Taiwan outperform

In China, stocks jumped 7.4% in USD terms in January, buoyed by rising hope of a sustainable recovery in the world’s second largest economy, which grew 6.5% year-on-year (YoY) in 4Q20. For the whole of 2020, China’s GDP grew 2.3%, making it the only major economy in the world to avoid a contraction last year as many nations struggled to contain the COVID-19 pandemic.

Similarly, Taiwanese stocks rose 6.5% in USD terms, driven by the strong performance of index heavyweight Taiwan Semiconductor Manufacturing Company, following the announcement of a larger-than-expected USD 28 billion capital expenditure plan for 2021.

Hong Kong tracks the regional upswing, South Korea sees muted gains

Elsewhere, Hong Kong and South Korean stocks turned in USD gains of 2.0% and 1.2%, respectively, for the month. Hong Kong equities were boosted by strong buying from mainland Chinese investors through the Shanghai-Hong Kong Stock Connect.

In South Korea, stocks turned in muted gains, weighed down by a rise in COVID-19 cases in the country and a correction in Samsung Electronics shares after the company’s vice chairman Jay Y. Lee was sentenced to two and a half years in prison over a bribery case.

India and ASEAN underperform

In India, stocks returned -2.3% in USD terms, as sentiment was dampened by the new coronavirus strains and news of fresh border tensions with China. The country is set to announce its annual budget in early February with spending measures to boost the pandemic-hit economy.

In the ASEAN region, stocks lagged their regional peers and turned in mixed performance in January. Singapore and Thailand were the best performing ASEAN markets, with respective USD returns of 1.0% and 0.1%, while the Philippines, Malaysia and Indonesia incurred respective USD losses of 8.0%, 4.1% and 2.8%. In the Philippines, extended travel curbs and weak export data raised concerns about the country's fragile economic recovery. Meanwhile, the Malaysian government re-imposed the Movement Control Order in several states in mid-January and subsequently declared a state of emergency to rein in rising COVID-19 infections.

Chart 3: MSCI AC Asia ex Japan Index1

1Note: Equity returns refer to MSCI indices quoted in USD. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

Market outlook

Asian countries have ample fiscal and monetary stimulus headroom

Asian countries have, by and large, handled the COVID-19 pandemic better than their western counterparts and are now emerging from their post-outbreak nadirs. Most of these countries also have plenty of fiscal and/or monetary stimulus headroom. And this superior growth and better national finances are available at a significant discount to developed markets. A languid USD should enhance local currency returns in these "risk assets".

China could see a broadening and deepening of innovation

China aims to remain open to the world (international circulation), while engineering a shift from infrastructure-led growth to innovation- and consumption-led growth (domestic circulation). Announcements or targets in the areas of fiscal sustainability, stabilising supply chains (especially as it pertains to technology) and addressing climate change via the national emissions trading scheme show a commitment to "walk the talk". The government's no-nonsense approach towards corruption and abuse of power, even if the perpetrators are the giants of China's digital economy, ought to lead to a broadening and deepening of innovation. Meanwhile, Hong Kong continues to come to terms with the reality that the "one country, two systems" is only possible if the "one country" doesn't feel threatened by the "second system". Accordingly, we favour areas of improving domestic demand, localisation and strategic industry development.

Focusing on private sector banks, digital services and logistics in India

India's government has pushed through labour and agriculture reforms that could be transformative if executed well. Labour reforms have also relaxed onerous restrictions on lay-offs, fixed-term employment and unions, thereby boosting efficiency. The new laws significantly reduce the compliance burden, which has been a major deterrent for investments in labour-intensive sectors in much need of productivity improvements, such as agriculture. This sector will also benefit from the recent passage of reforms announced in May via much-needed investment in the supply chain, which makes it more efficient. We continue to focus on sub-sectors benefiting from trends such as market consolidation, formalisation, and companies that reduce the friction of doing business, namely private sector banks, digital services and logistics.

Selective in South Korea, Taiwan and ASEAN

Increased digitisation—of work, health, manufacturing, social media, clean energy, or commerce—relies heavily on the semiconductor industry and the technology supply chain. In this regard, South Korea and Taiwan remain well positioned, notwithstanding the rising tensions between China and the US. However, a cautious and selective approach is warranted.

In the ASEAN region, COVID-19 has catalysed a massive acceleration in digitisation, notably in Indonesia. And Indonesia and Vietnam, in particular, are benefiting from the redesign of supply chains currently heavily reliant on China. Thailand's lacklustre economy needs a sizeable fiscal impulse, one that is unlikely given ongoing political developments. Singapore's stock market remains a proxy for the region, albeit with a better governance framework. Besides continued capital inflows from Hong Kong, there is little fundamentally that excites us here in Singapore. The Philippines is showing early signs of a cyclical recovery, and we are content to stay watchful for now. Malaysia remains uninteresting except in niche segments.

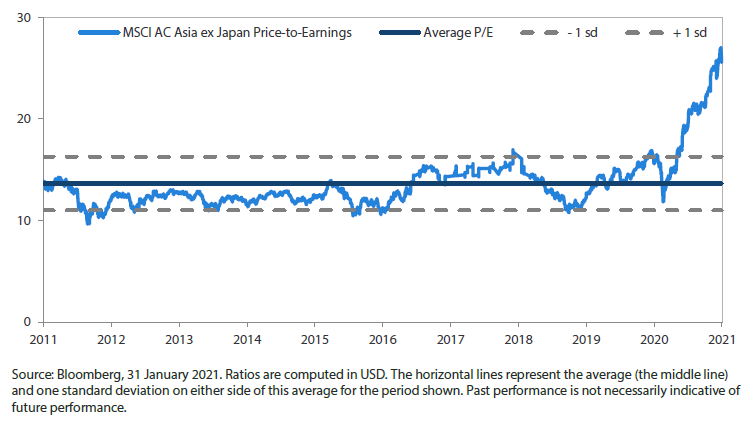

Chart 4: MSCI AC Asia ex Japan price-to-earnings

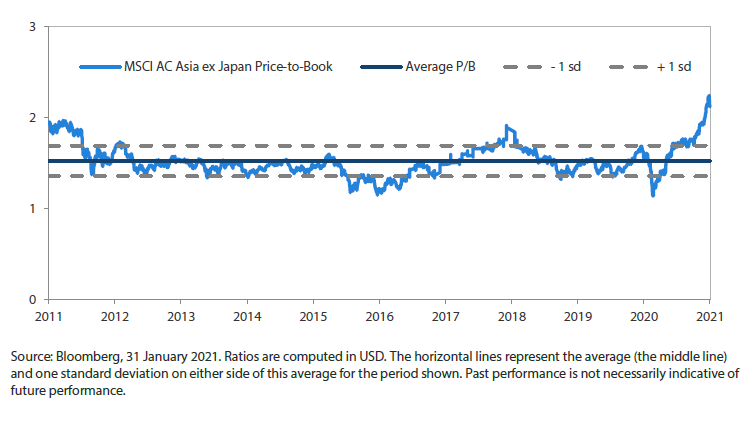

Chart 5: MSCI AC Asia ex Japan price-to-book