Summary

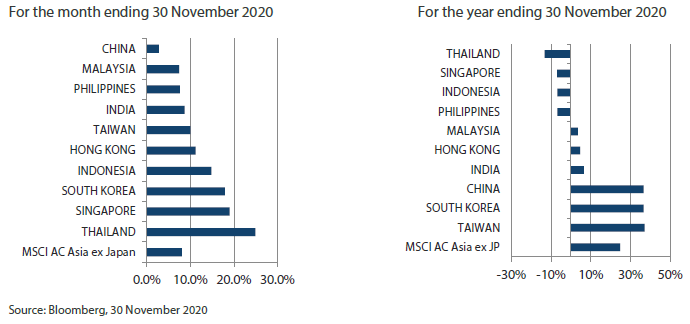

- Asian stocks turned in strong gains in November, boosted by positive COVID-19 vaccine developments, rising hopes for better US-Asia ties under the leadership of US President-elect Joe Biden and stronger-than-expected economic data from several Asian countries. The MSCI AC Asia ex Japan Index rose 8.0% in US dollar (USD) terms over the month.

- Thailand, Singapore and South Korea were the best performers in November. Thailand and Singapore were buoyed by improving economic outlooks, while the rally in Korea was led by index heavyweight Samsung Electronics, which surged during the month on higher demand prospects in 2021.

- China lagged the region over the month, due to a rise in US-China tensions. The Trump administration stated it was poised to add China's top chipmaker SMIC and national offshore oil and gas producer CNOOC to a blacklist of Chinese companies with ties to China's military.

- Despite the continued rise in COVID-19 cases in the West and several lockdowns that ensued, markets have preferred to focus on the positives of more assured outcomes from vaccines, US presidential elections and economic recovery. Our preference continues to be for domestic-focused stocks in structural growth areas of software, automation, healthcare and insurance.

Market review

Regional stocks surge on positive COVID-19 vaccine developments

Asian stocks turned in strong gains in November, boosted by positive COVID-19 vaccine developments, rising hopes for better US-Asia ties under the leadership of US President-elect Joe Biden and stronger-than-expected economic data from several Asian countries.

For the month, the MSCI AC Asia ex Japan Index surged 8.0% in US dollar (USD) terms. Within the region, Thailand, Singapore and South Korea were the best performers in USD terms (as measured by the MSCI indices), while China, Malaysia and the Philippines were the laggards.

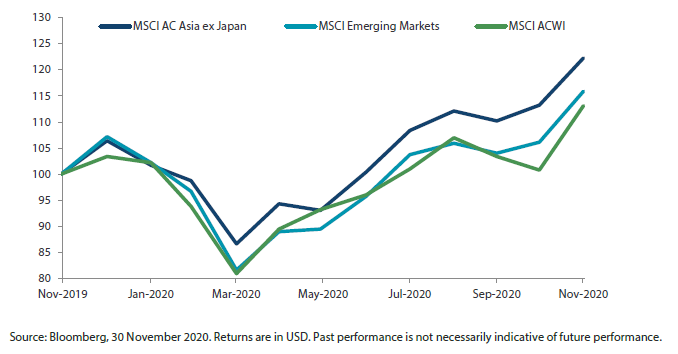

Chart 1: 1-year market performance of MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index

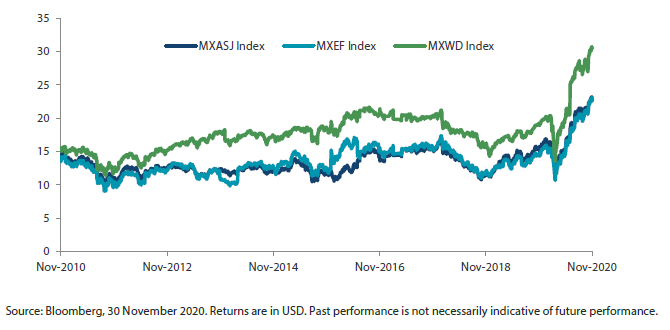

Chart 2: MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index price-to-earnings

Thailand and Singapore outperform, Malaysia and the Philippines lag

In Thailand and Singapore, stocks jumped 24.9% and 19.0%, respectively, in USD terms in November, buoyed by an improvement in economic outlook. Thailand's GDP contraction moderated to -6.4% year-on-year (YoY) in the third quarter of 2020 (3Q20), as exports and domestic tourism started picking up from the coronavirus-induced slump. Likewise, Singapore's economy shrank at a slower rate of 5.8% YoY in 3Q20; on a quarter-on-quarter (QoQ) basis, it grew by 9.2%, exceeding the Singapore government's estimates of a 7.9% QoQ expansion.

Indonesian stocks also did well, climbing 14.8% in USD terms. Comfortable with its inflation outlook, Bank Indonesia cut its benchmark 7-day reverse repurchase rate by 25 basis points to 3.75% in an attempt to pull its economy out of recession. Stocks in the Philippines and Malaysia, however, lagged their ASEAN peers, turning in USD gains of 7.6% and 7.4% respectively. Sentiment for Malaysian equities was dampened after the country extended movement curbs across most states and banned inter-state travel in an attempt to contain a surge in COVID-19 cases.

India tracks the regional upswing

In India, stocks tracked the regional upswing and climbed 8.6% in USD terms for the month, as COVID-19 restrictions largely eased in the country. India's economy contracted by 7.5% YoY in 3Q20, beating market expectations of a deeper contraction. In November, global index provider MSCI added 12 stocks, including those of Kotak Mahindra Bank and Yes Bank, to the MSCI India Index, potentially attracting fund flows to these new index components.

South Korean stocks jump while China equities underperform

Elsewhere, South Korean shares jumped 17.9% in USD in November, buoyed by vaccine-led recovery hopes. The rally was led by index heavyweight Samsung Electronics, which surged during the month on higher demand prospects and better earnings outlook for 2021. In Taiwan, stocks returned 10.0% in USD terms, supported by the country's better-than-expected 3Q20 GDP, which expanded 3.92% YoY; while Hong Kong stocks returned 11.2% in USD terms for the month.

The region's biggest laggards in November were China stocks, which posted modest USD gains of 2.8% due to a rise in US-China tensions. The Trump administration stated it was poised to add China's top chipmaker SMIC and national offshore oil and gas producer CNOOC to a blacklist of Chinese companies with ties to China's military. On the economic data front, China's factory activity expanded at the fastest pace in more than three years in November, while growth in the services sector also hit a multi-year high.

Chart 3: MSCI AC Asia ex Japan Index1

1Note: Equity returns refer to MSCI indices quoted in USD. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

Market outlook

Markets have preferred to focus on the positives

Despite the continued rise in COVID-19 cases in the West and several lockdowns that ensued, markets have preferred to focus on the positives of more assured outcomes from vaccines, US presidential elections and economic recovery. Some of the trends that were accelerated by the virus will likely remain. But for the near future, we see a migration towards the worst affected areas and countries, which should see greater incremental improvement in earnings. Caution is still warranted, however, as geopolitical confrontations, liquidity tightening and increasing regulation threaten some specific areas of the market. Hence, our preference continues to be for domestic-focused stocks in structural growth areas of software, automation, healthcare and insurance.

Views on China reflect new risks

The Chinese authorities sent some clear messages to the private sector in November and these will have significant implications for future sustainable returns. The decision to change regulatory requirements which led to the pulling of Ant Group IPO was significant. This was due to be the largest IPO allocation ever and one that would have valued the company at or above Chinese state-owned financial heavyweights ICBC and CCB. The new regulations favour banks, whilst they are more punitive for some fintech companies, including Ant. In addition to this, we also saw a raft of policy suggestions for anti-competitive behaviour on the part of platforms. This will impact the whole industry but perhaps disproportionately the largest players. Our views on China reflect these risks; we now have a particular focus in areas of improving domestic demand, localisation and strategic industry development.

Focusing on digital services and logistics in India

We continue to witness improvements in underlying economic data in India, which coupled with positive structural reform in both the labour and agriculture sectors, should result in improving sustainable returns over the longer term. We continue to focus on sub-sectors and companies benefiting from trends such as market consolidation and formalisation. We are also focused on companies that reduce the friction of doing business—digital services and logistics.

On the lookout for opportunities in South Korea and Taiwan; selective in ASEAN

In addition to good containment and limited economic disruption, South Korea and Taiwan have both enjoyed booming demand for technology, healthcare and clean energy exports, which have further boosted their domestic economies. We continue to be mindful of the sensitive geopolitical spot both countries are in and hence remain on the lookout for opportunities in esoteric sectors such as clean tech, content and industrial automation.

Despite significant rallies from deeply oversold levels, we remain relatively selective in the ASEAN region. The political environment in several countries remains a headwind to positive reforms, while there is fierce competition for manufacturing re-shoring opportunities. Vietnam has been the standard bearer in terms of handling COVID-19 and the recovery in economic activity, particularly as supply chains undergo reconfiguration in the new normal. As such, we maintain our focus in electric vehicle (EV) materials and high-quality banks, both of which are in Indonesia.

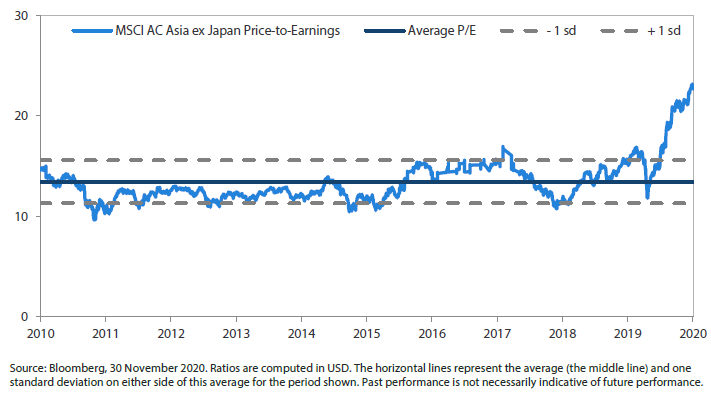

Chart 4: MSCI AC Asia ex Japan price-to-earnings

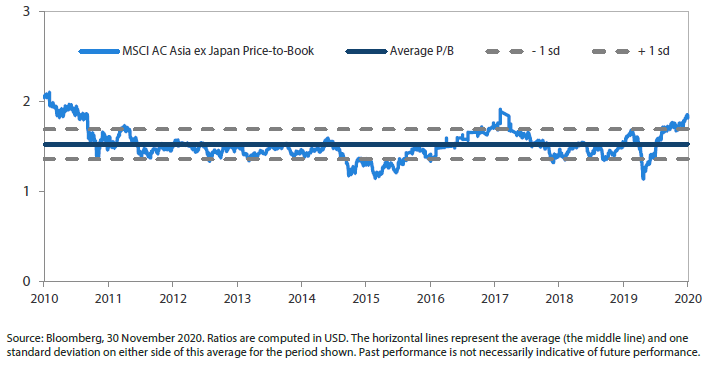

Chart 5: MSCI AC Asia ex Japan price-to-book